Coronavirus and the Health of the U.S. Economy

The Fletcher School, Tufts University and EconoFact

The Issue:

The coronavirus has, in a matter of weeks, had a profound impact on the world economy. The economic impacts stem both from the direct effect of those who fall ill and from the measures taken to contain or slow the progression of the pandemic. These effects, operating through both domestic and global channels, affect supply and demand, both through direct effects and through people’s expectations of the future. The ultimate consequences of this pandemic will depend upon the depth and duration of the shock, as well as the effectiveness of measures to counter it. At this time, it is difficult to gauge the magnitude of the effect because of our current lack of understanding of the coronavirus as well as uncertainty about the scope and efficacy of policy responses. Nonetheless, it is possible to provide frameworks for understanding some of the different channels through which it is likely to impact the economy.

The Facts:

- Because this is a new virus many important factors that would help model the progression of the pandemic and its economic impact are unknown. The novel coronavirus that causes COVID-19 first emerged in Wuhan, Hubei Province, China and is thought to have spread from animals to humans. The disease spread rapidly in China, from none to over 80,000 cases with over 3,000 deaths between the beginning of the year and early March (see Johns Hopkins coronavirus site for world wide updates). The course of the epidemic is defined by several key factors, which are not yet well understood for COVID-19. In order to determine the overall number of people who are likely to be infected, scientists look for the basic reproduction number — the average number of secondary cases each new case generates in a population. This is a poorly understood number in the initial stages of the current epidemic, when scientists are uncertain about aspects such as transmission in children. Importantly, scientists also have a high degree of uncertainty regarding the case fatality rate for the disease. The case fatality rate is calculated using the number of people who have the virus and the number of deaths caused by the virus; but the number of people with the virus is not known at this time. The actual fatality rate could be lower than current numbers indicate if infections are being undercounted because many in the population have a mild version of the disease and are not tested for it. Alternatively, the number could be higher if people who are currently counted as sick eventually die of the disease (see here).

- Initial estimates expect the economic disruption stemming from the coronavirus pandemic to bring down global growth in the first quarter of 2020, but there is wide uncertainty about the magnitude as well as the range of expected effects further out. To cite one example, expectations for global growth for 2020 fell by 0.5 percentage points in the forecasts issued by the Organization for Economic Co-operation and Development (OECD) between the forecast issued November, 2019 and the one issued on March 2, 2020. This change illustrates how quickly conditions changed as a result of the new virus. However, there is a high degree of uncertainty regarding even the latest forecasts. The March base-case scenario from the OECD, in which world growth slows to 2.4 percent and rebounds by 2021, is based on the assumption that the epidemic peaks in China in the first quarter of 2020 with gradual recovery in the second quarter and that new cases of the virus in other countries prove sporadic and contained. A more pessimistic OECD scenario estimates a reduction of World GDP by 1.5 percentage points in 2020. McKibbin and Fernando estimate a wide range of values for the effect of coronavirus on GDP growth (relative to baseline), depending upon the severity of the disease and its spread. They estimate a reduction in United States 2020 GDP growth rate of 0.1 percent to 0.2 percent if the epidemic is confined to China. If the disease spreads widely across the world, as is now more likely, of 2.0 percent (if 10 percent of the Chinese population becomes infected and 2 percent of those people die) to 8.4 percent (if 30 percent of the Chinese population becomes infected and 3 percent of those people die). This range reflects the uncertainty associated with both the coronavirus itself and the scope and efficacy of policy responses.

- The initial impact to the U.S. economy stems from the effect of the outbreak on China and to the rising importance of China to the world economy and U.S. supply chains. In addition to the rising infection and mortality being caused by the virus and affecting workers, the Chinese government instituted quarantines and widespread restrictions on mobility and travel, which have delayed restarting factories and production after the Lunar New Year holiday. China plays a key role in global supply chains for computers, electronics, pharmaceuticals and transport equipment. Many companies with integrated global supply chains that depend on Chinese components to manufacture their end products already began facing delays and disruptions to their production, according to a March 11 survey by the Institute of Supply Management. These disruptions are likely to be more severe than those from past events that were more localized such as the 2011 Fukushima disaster. Reduced production constitutes a supply shock, with businesses located far from China facing rising costs, diminished productivity and reduced economic activity and with consumers eventually facing the potential of product shortages. In addition, China's rapid economic rise over the past decades mean that an economic slowdown in China has global repercussions as the country now accounts for 17 percent of global GDP, 11 percent of global trade, 9 percent of global tourism and over 40 percent of global demand for some commodities, according to the OECD. Due to the decline in economic activity for instance, demand for oil from China had dropped by 20 percent in February pushing down the global price for the commodity.

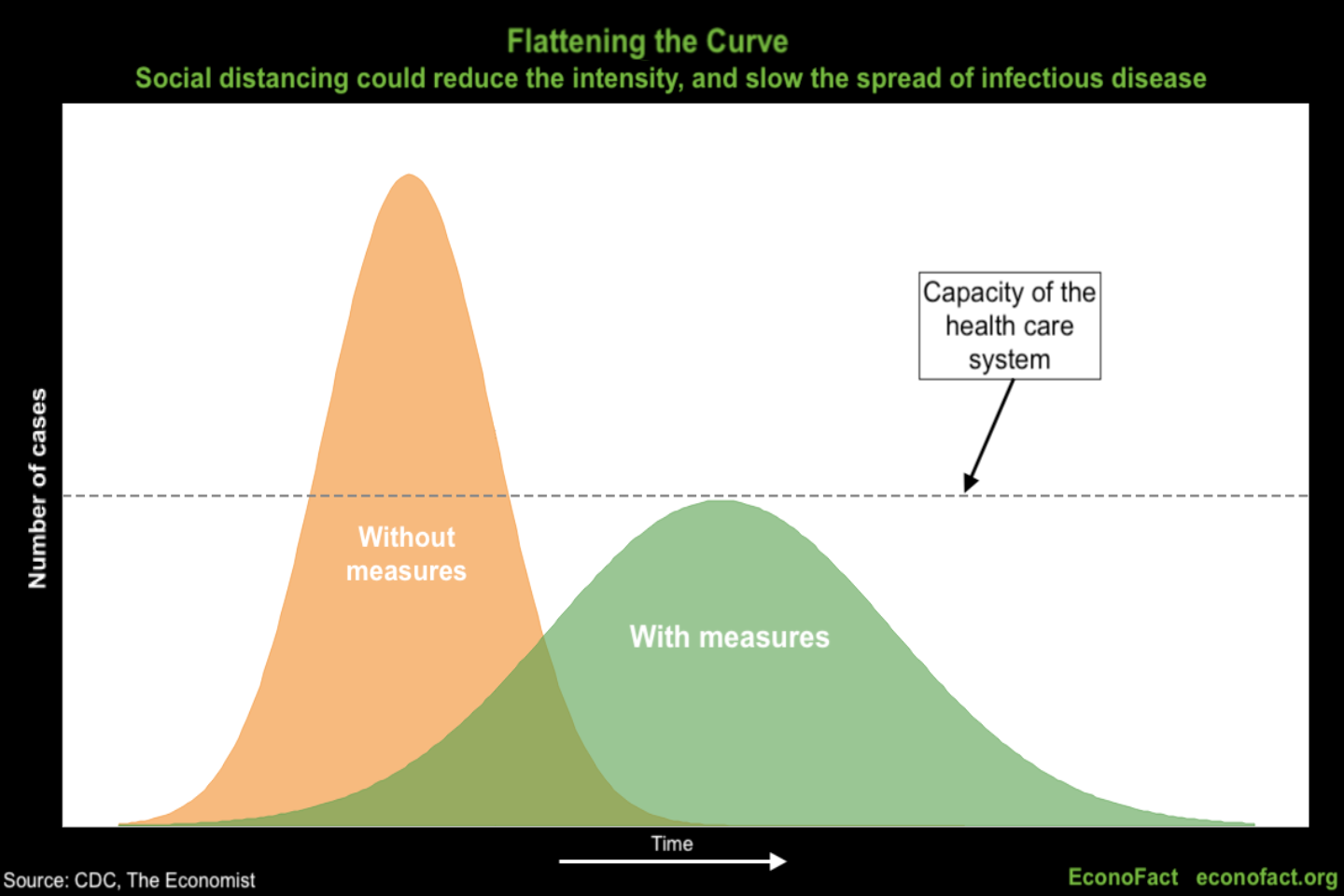

- As the outbreak spread beyond China, measures that attempt to slow the spread of the disease have raised its economic costs domestically. An important public health goal is to slow the incidence of the disease in order to both lower the total number of cases and to keep the number of new cases from spiking so as to not overwhelm the healthcare system. An important way to achieve this “flattening of the curve” (see graph) is through social distancing. This will have the effect of lowering demand for some products and services through actions like canceling large-scale events (like SXSW (South by Southwest) which was estimated to have boosted the Austin, Texas economy by $356 million last year), running sports events without spectators (as is already being done with two Division I basketball tournaments), suspending sports leagues’ games (as the NBA did on March 11, followed by the NHL and Major League Baseball which delayed the opening of its season), and having students remain home and take classes online after Spring Break (which is being done at a wide range of colleges and universities). And the impact of lowered demand is not limited to big-ticket items and organized events. The person running a coffee stand in Manhattan stands to lose business as people work from home and so does the Uber driver losing rides from people not going out for dinner or drinks. Social distancing will have a supply-side effect as some employees are required to work remotely, and this is likely less efficient than working in an office. But while some jobs lend themselves to remote work, others do not. For example, manufacturing and service jobs in hospitality, travel, tourism, and in-person retailing demand workers show up at their place of business. A reduction in demand, along with concerns about contagion, could hit workers in these industries particularly hard.

- The very uncertainty associated with this epidemic also has adverse economic effects. People are less likely to purchase big-ticket items if they are uncertain about their incomes in the future. Companies too are more likely to hold off on hiring, or investing in plant and equipment. The deep uncertainty about the economic effects of the coronavirus has already affected the stock market, with indices falling by about 20 percent between mid-February and mid-March. And there is a risk that these effects could feed into each other triggering a response that is greater than the circumstances warrant. A decline in stock prices means that people will reevaluate their wealth, which could also cut consumption. Fear raised by this uncertainty can contribute to panic buying, shortages, and disruptions.

- The adverse economic effects of the pandemic could be exacerbated through financial channels. Banks, facing a range of challenges, have seen their stock prices fall by more than 30 percent between mid-February and mid-March. The net interest income of banks falls with lower interest rates. The specter of a slowdown in economic growth has reduced demand for bank lending by both businesses and consumers. There is also a concern that, as the economy slows down, loans, especially higher-risk loans, may not be repaid, which could have cascading effects. For instance, oil companies that borrowed to take advantage of low interest rates but are now facing low oil prices could default on loans. As banks begin to suspect that customers will be unable to repay loans on a timely basis this could cause banks to raise borrowing costs and to tighter financial conditions (see here) which could cause a spiral of slower growth leading to yet tighter financial conditions which slows growth even further.

What this Means:

The coronavirus pandemic is first and foremost a health crisis. The full impact on the U.S. economy will depend on many important and related factors such as the spread of the disease, the severity with which it strikes different locations, the effectiveness of measures local and national authorities take to curtail it, and how long it lasts. These factors will play a large role in determining whether this is a temporary setback with a relatively fast recovery or whether it is a more pronounced slump. The longer the crisis persists, the more likely that businesses would have to start laying off workers, which would reduce family incomes and spending, and contribute to a downward spiral. The typical measures aimed at stimulating demand to counter a slowing economy are not likely to be effective in the short term — when reductions in supply are due to workers being sick and supply chains being disrupted and while demand is depressed due to people hunkering down in order to increase social distancing.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.