What Problems (If Any) Arise From Stock Buybacks?

Brandeis University

The Issue:

Stock buybacks by the firms included in the S&P 500 index have increased recently, rising from an average of about $135 billion per quarter over the previous three years to over $200 billion per quarter: $800 billion in the first eleven months of 2018 with announced buybacks bringing the figure to $1,100 billion for the year. This is an acceleration of a trend that started during the recovery from the 2007-2009 financial crisis. The increase in buybacks has raised concerns about whether they disproportionately apportion company earnings to increasing the wealth of stockholders and happen at the expense of greater capital investment that would raise future firm profitability, worker productivity and economic growth. Senators Charles Schumer (D-NY) and Bernie Sanders (I-VT) propose limiting corporations’ ability to repurchase shares until they pay a minimum of $15 per hour to workers and also offer a mandated range of benefits. Senator Marco Rubio (R-FL) wants to change tax laws in order to reduce the attractiveness of share buybacks to corporations. Each of these proposals is framed by its sponsors as a tool for encouraging businesses to invest – presumably for the benefit of the larger economy – rather than returning capital to their investors. But is the increase in stock buybacks cause for concern?

Share repurchases and a thriving market for equity issuance are consistent with a healthy redeployment of capital toward the firms that have the most attractive investment opportunities.

The Facts:

- Stock buybacks are a channel that corporations use to return value to their owners. And, they can also serve to free up capital for potentially productive investments by other firms. The fiduciary responsibility of a corporation is to return value to its owners, that is, those who own the shares of the corporation. A corporation can use retained earnings to finance new investments that increase the value of the firm, taking into account the riskiness of those investments. In the absence of profitable investment opportunities, a corporation can maximize value for investors by paying them dividends or, alternatively, by repurchasing shares of the firm from investors. Investors who receive dividends, or the proceeds from selling shares back to the corporation, can then reinvest this money in other firms with better prospects. This is an important engine of growth in a dynamic, market-based economy and helps liberate capital from declining businesses to have it redirected to higher-growth firms. Share repurchases and a thriving market for equity issuance are consistent with a healthy redeployment of capital toward the firms that have the most attractive investment opportunities.

- Looking only at the value of stock buyback activity provides an incomplete view of the capital flows into and out of corporations and, by extension, of their ability to invest in their business. Corporations buy back shares, but they also issue new shares that raise additional capital, by either selling them directly to public investors in exchange for cash or indirectly, such as when a company issues shares as part of an acquisition of another firm or to compensate its employees. Repurchases and issuances can offset each other, so the value of gross repurchases gives a misleading picture of the net flow of capital into or out of the corporate sector (see here). Taking into account equity issuance, the recent net payout to shareholders has been more modest than the gross figure would indicate. The Federal Reserve Board has recently worked to enhance the publicly-available data on net equity flows in its benchmark financial accounts of the United States. Their data, which include repurchases, Initial Public Offerings (IPOs), and Secondary Equity Offerings (SEOs), confirm that gross repurchases have risen since the passage of the Tax Cut and Jobs Act in December 2017, but there is not a clear recent trend in net equity repurchases by United States corporations.

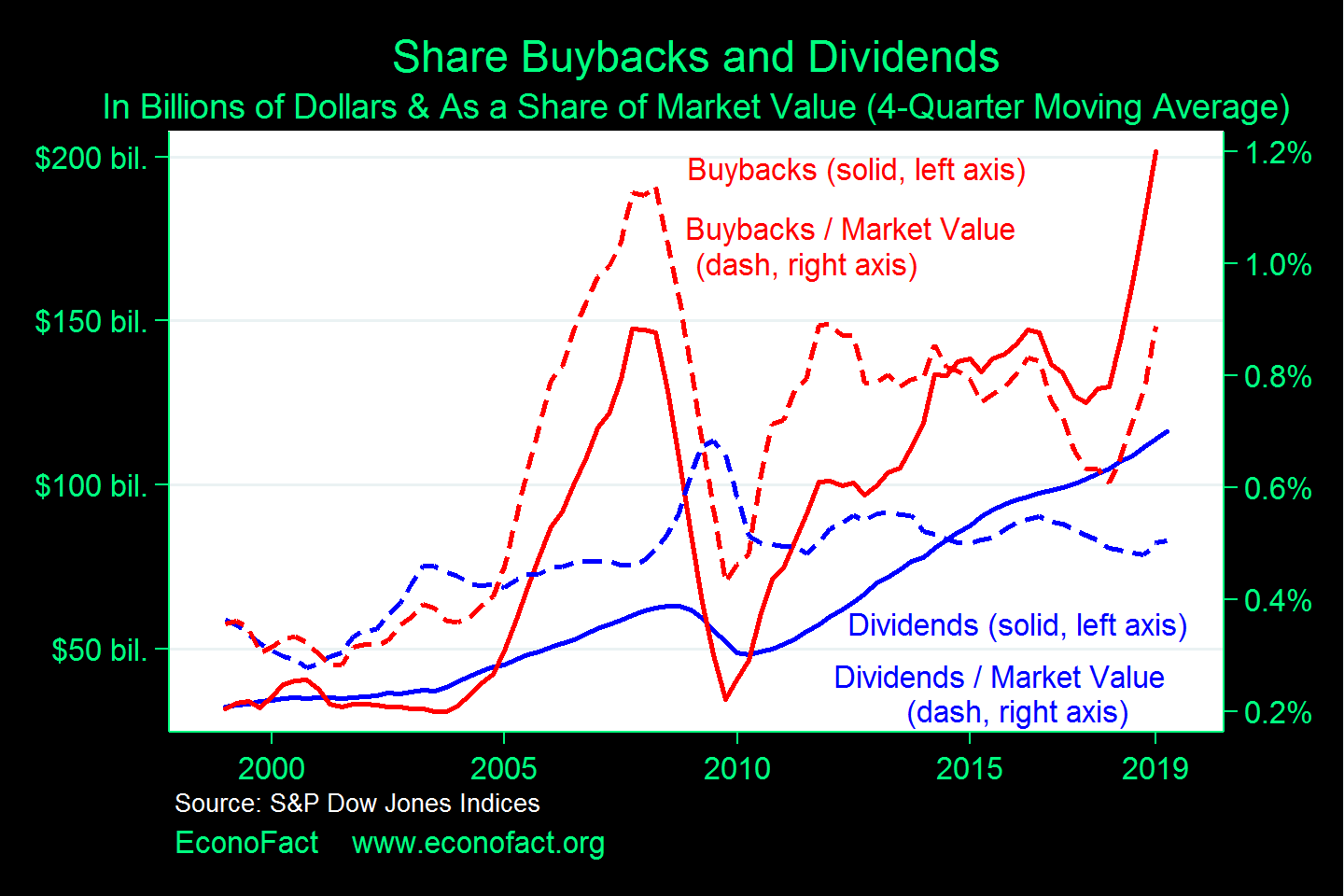

- One reason that stock buybacks have risen recently may have to do with the increasing overall value of the stock market. By scaling gross share repurchases (the solid red line in the figure) by the market value of corporations (the dashed red line), we see that there is no clear long-term trend since the recovery from the financial crisis of 2007-2009. Likewise, consider how scaling the value of dividends (the solid blue line) by the market value of corporations (the dashed blue line) flattens out that time series.

- Some of the increase in share repurchases may reflect a pivot from dividend payments to repurchases as a mechanism for distributing returns to shareholders. There is a close equivalence between stock buybacks and dividend payments. Both are means of returning capital to investors. But there are reasons why companies my prefer buybacks over dividends under certain circumstances. Corporate executives tend to be very wary about sending negative signals about their companies’ prospects, and this has historically made them very reluctant to cut the dividends once a certain level has been established, since this may be taken by the market as a sign of problems. In contrast, distributing cash in the form of share buybacks has not typically been viewed by the market as marking an ongoing commitment to future cash distributions as well. A survey of finance executives suggests that they view repurchases as a more flexible method to return cash to investors than dividends, and thus can be timed to take advantage of swings in stock prices. That survey also suggests that these managers believe investors are indifferent between dividends and repurchases.

- A pivot between dividends and repurchases as a mechanism for delivering returns to investors may be neutral in terms of aggregate capital flows. A simple numerical example illustrates this. Consider a corporation with ten shareholders, each of whom has one share. The value of the corporation is $1,000, comprised of a factory worth $900 and $100 in cash that it would like to return to its shareholders. Each of the ten shares is worth $100. The corporation could pay a $10 dividend per share, in which case shareholders have $10 in cash and a share now worth $90. Alternatively, the corporation could repurchase one of the outstanding shares for $100. The shareholder who sold the share back to the firm would get $100 in cash and the remaining shareholders would see no change in the price of their share since the nine remaining shareholders would each have one-ninth of the $900 value of the firm. In this simple example, the overall payments to investors are equivalent, although the dividend payments go to all ten investors while the repurchase focuses the cash distribution on the investor who sells the share of the firm back to the company. Also notice that the buyback does not boost the company’s share price in this example; there are fewer shares, but that is matched by a lower overall market value of the firm. In the data represented in the figure, note the general tendency for the value of buybacks and the value of dividends to move together.

- One problem that does arise with stock repurchases as opposed to dividend payments is due to tax rules. Because of the way that stock passed to heirs through estates gets taxed, and because of the fact that foreign investors are taxed on dividends but not on capital gains, a pivot to stock buybacks could impact federal tax revenues. The top federal tax rate paid on dividend income is 23.8 percent, which is the same rate that is paid on long-term capital gains (that is, capital gains on stocks held for more than one year – capital gains tax rates for stocks held less than one year are higher, and investors respond to these differences). So, in the numerical example above regarding dividend payouts, the ten shareholders who received dividends would each pay $2.38 and the total tax received by the federal government would be $23.80. In the numerical buyback example, the shareholder who sold stock back to the firm would pay 23.8 percent of the capital gain, which is the difference between the price as which the share was sold and the “basis,” the amount paid for the stock. Suppose the shareholder who sells her share in a buyback purchased the stock for $50; in that case, the sale of the share for $100 results in a tax liability of $11.90 ($50 x 23.8%). Furthermore, tax rules allow the basis to rise to the current market value of the stock upon the death of the shareholder, so her heirs would not pay any capital gains tax if they sold their inherited stock at the price prevailing at her death, regardless of how large the capital gains of the stock during the shareholder’s lifetime. This rule then allows avoidance of taxes on capital gains for bequests of shares of a corporation. Finally, the United States taxes foreign shareholders on dividends, but not on capital gains, so foreign holders of United States stocks avoid paying taxes to this country.

What this Means:

While stock buybacks reached record levels in 2018, it is not clear that this represents a barrier to overall corporate investment or that it calls for legislation to limit buyback activity. There is an intrinsic similarity between paying dividends and repurchasing shares of a corporation. Thus, one likely immediate consequence of only allowing firms to repurchase shares when certain conditions are met would be a pivot from repurchases to dividends as a method for distributing excess cash to investors. Over a longer horizon, forcing a corporation to go through a “gate” before it can repurchase their shares would likely act as a deterrent to new investors who want to invest in equity in the American corporate sector. Imagine barring the door at a party and preventing party-goers from leaving – doing this might keep the people currently in the room in the room for a bit longer, but it may also discourage anyone not currently at the party from joining the event.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.