What Are the Financial Risks From Climate Change?

University of California, Santa Cruz

The Issue:

Climate change is no longer a future threat; some of its effects are already being felt. Rising temperatures are increasing the frequency of devastating weather events as hurricanes, fires, floods, droughts, extreme heat, and extreme cold. In addition to their direct impact on the population, these effects bring about substantial economic costs. Although the worst predicted impacts of climate change are still far away in the future, some financial risks associated with climate change and climate change mitigation efforts are more imminent.

Although the worst predicted impacts of climate change are still far away in the future, some financial risks associated with climate change and climate change mitigation efforts are more imminent.

The Facts:

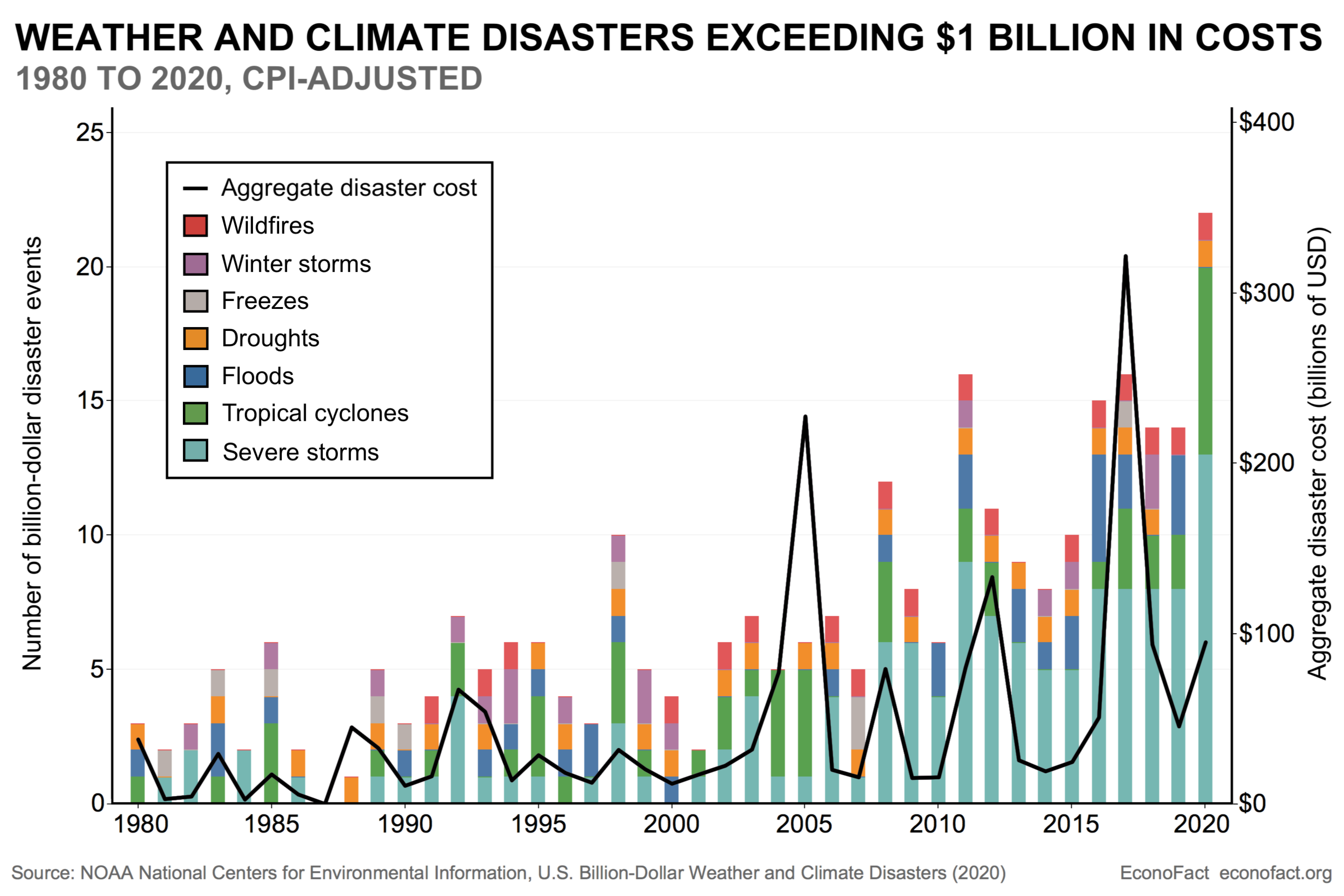

- Climate change impacts all areas of the economy. The frequency of high-cost climate and weather disasters increased over the past four decades in the United States according to data tracked by the National Oceanic and Atmospheric Administration (see chart). Agriculture, infrastructure, human health and productivity, tourism, businesses, and financial markets are already affected by extreme weather events becoming more frequent (see here). These direct impacts include flooded and burned land, companies going out of business, destruction of residential and commercial real estate, increased burden of insurance companies, and in some cases bankruptcies — most notably the case of PG&E, California's largest utility after devastating wildfires in the state. The risks of such losses becoming more widespread as global temperatures continue to rise are frequently referred to as physical risks.

- The localized nature of physical risks combined with the fact that disasters are being projected for some later time in the future, lead to a lack of bold action by policymakers in the present. For now, physical risks remain largely localized, although the recent fires in Australia give us a preview of what scientists project for the future if global warming is not contained. Because of their localized nature, however, extreme weather events so far have not posed a systemic financial threat. And the conditions under which the losses from physical risks will become systemic are still far enough in the future. According to Mark Carney, Governor of the Bank of England, this constitutes a "tragedy of the horizon" because the catastrophic impacts of climate change will be felt beyond the traditional horizons of most actors – imposing a cost on future generations that the current generation has no direct incentive to fix and is largely responsible for lack of bold actions on the part of policymakers.

- Much less broadly recognized are “transition” risks that come from potential climate change mitigation efforts via government policies or changes in consumer and investor behavior. Such risks may be realized much sooner than the bulk of the impact of “physical” risks. As governments, companies and consumers begin to take actions to address climate change, the resulting changes in policies, technologies and consumer and investor behavior could lead to big changes in how certain assets, industries or properties are valued. Some governments are already implementing policies designed to reduce emission of greenhouse gases. For example, the United Kingdom is aiming to phase out coal power generation by 2025. In addition, there are efforts by consumers and businesses to decarbonize; for instance, U.S. solar installations increased at annual growth rate of 50% in the last 10 years and electric car sales are increasing exponentially. Moreover, investors, private and institutional, are increasingly demanding sustainable or “green” investment opportunities (take BlackRock's sustainability announcement or Morgan Stanley's Green Corporate Bonds). All these changes are likely to put pressure on industries and assets that are related to fossil fuels. Potential shocks such as imposition of or an increase in an already existing carbon tax, divestment by large and high-profile funds from fossil-fuel related assets and companies, or rapid switch of consumer demand to alternative transportation and utilities can lead to sharp repricing of financial assets associated with fossil fuel and related industries. Moreover, some assets, such as coal-industry related assets may become “stranded,” with their value dropping to zero. Financial institutions that are highly exposed to such industries and assets may then experience losses that have potential of generating systemic financial stability problems. Such risks are referred to as “transition” risks associated with climate change and they describe risks that may materialize much sooner than physical risks.

- What role do central banks play in addressing the financial risks from climate change? In recent years, central banks around the world have recognized that they have to play a role in recognizing and mitigating climate-related risks (see here). All aspects of central banks’ mandate are affected by climate change, as described recently, for the case of the Federal Reserve, by Governor Lael Brainard. Many central banks now include assessment of financial risks related to climate change in their financial stability reports and special publications (see the Bank of England or European Central Bank, for examples). Moreover, some central banks have tools at their disposal that could incentivize investment in “green” finance. In addition, central banks can use their convening power to accelerate collaboration between academics, markets, and policymakers in order to understand and address climate-related risks. The Federal Reserve system had it’s first such conference in November, 2019.

- Recognizing transition risks would help the financial sector to reduce their exposure to assets and industries that are subject to these risks. This work is already under way, by the industry’s own initiative as well as through climate related stress-testing by the Bank of England and the central bank of the Netherlands. The main challenge in this effort is the ability to classify assets and industries into “green”, “brown”, and “neutral”. The European Commission took the first step towards alleviating this barrier by providing a first taxonomy of “green industries”. Such a taxonomy could also be used to facilitate other issues of “green” financial instruments.

What this Means:

Climate change presents two types of risks to the economy: physical risks, those stemming from increased frequency of extreme weather events, rising temperature, and sea level rise; and transition risks, those resulting from rapid repricing of financial assets as a result of changes in policies or shifts in consumer and investment demand. Physical risks are more obvious, but do not yet affect the majority of the population. Transition risks are imminent given increasing calls to action to mitigate climate change. Recognizing transition risks would allow for more gradual divestment from assets that are subject to repricing or may become stranded, which by itself will help transition to carbon-free economy. The importance of transition risks is just beginning to be recognized by the financial industry and policymakers.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.