Inflation and Prices

The Fletcher School, Tufts University

The Issue:

By many objective measures, the performance of the U.S. economy in 2023 was outstanding. The sharp decline in inflation from a high of almost 9 percent in June 2022 to 3.4 percent at the end of 2023 without triggering a rise in unemployment and with continued strong economic growth has been called by one prominent economic journalist “a miracle.” It seemed as though the U.S. economy might be on target to achieving the oft-sought but elusive “soft landing”. But until recently, there has been a disconnect between this surprisingly strong performance and the public’s views on the economy. Some of this disconnect likely reflects consumers’ continued experience of higher prices. What is the link between inflation and the prices consumers experience? What might headline inflation statistics miss that affects economic well being across different groups?

It is possible to have “high” prices and low, or even zero (or negative), inflation at the same time.

The Facts:

- It is possible to have “high” prices and low, or even zero (or negative), inflation at the same time. In general, prices tend to increase over the long run. Using the price of a representative basket of goods purchased by urban consumers that is tracked by the Bureau of Labor Statistics, the Consumer Price Index (CPI-U), prices have more than tripled over the past 40 years: The reported index number equal to 100 for the average value of prices between 1982 and 1984 was 306.7 in December 2023. Inflation is the rate of change in prices over a given period of time. In its mandate to keep prices stable, the Federal Reserve does not aim for zero inflation, as an inflation rate that is too low can also be problematic for a national economy. Since 2012, the Federal Reserve has set an explicit target inflation rate of 2 percent. But inflation rose well above the Fed’s target following the COVID pandemic, reaching a high of around 9% in June of 2022. As a result, by December 2023 consumers were seeing prices that were on average about 19% higher than they were before the pandemic in December 2019, as measured using the CPI-U. However, the rate of increase of prices had slowed dramatically to 3.4% by December of 2023.

- The inflation rates for particular categories of goods and services can be, and often are, quite different from the overall headline inflation rate. The headline inflation rate is the weighted average of price changes of a wide set of goods and services, with the weights representing the relative proportion of expenditures spent on each category. The twelve-month inflation rates in December 2023 range from -14.7 percent for fuel oil to 20.3 percent for Motor Vehicle Insurance. Over this period, energy prices fell 2 percent (weight of 0.067), food prices rose 2.7 percent (weight of 0.13), and all items less food and energy, so-called core inflation, rose 3.9 percent (the weight of these core items in headline inflation is the remaining 0.80).

- What matters most for consumers is how the changes in prices affect their overall purchasing power. Different groups of consumers purchase different sets of goods and, therefore, face different inflation rates and price levels. The different inflation rates for different categories of goods and services mean that the reduction in purchasing power from inflation can differ widely across groups of people since people’s patterns of purchases vary depending upon a range of factors. For example, people who live in rural areas typically need to drive longer distances than urban dwellers, so gasoline prices make up a bigger part of their overall expenditures. Notably, the typical pattern of expenditures of poorer people differs markedly from richer people, with a higher proportion of spending by the poor on food and shelter. Furthermore, prices can differ across locations for the same types of goods, and where you shop can be as important as what you buy in terms of the prices you face. Consequently, there have been calls for developing price indexes by subgroups, for example, across the income distribution. The Committee on National Statistics of the National Academies of Sciences, Engineering, and Medicine recommends that the development of income-based price indexes should be a “high priority” for the Bureau of Labor Statistics. (p. 151)

- While the impact of inflation varies for consumers depending on their characteristics and the mix of goods they purchase, comparing a standardized basket of goods over a set period of time allows economists to gauge the state of price changes. Monthly inflation is typically reported at an annual rate by comparing prices in one month to prices twelve months before. Reported in this format, the inflation rate at a given point in time can provide information on whether production is in line with demand (as well as how consumers expect prices to behave going forward). When inflation rates are given for different lengths of time, it makes it more difficult to make these comparisons. For instance, in October 2023, a statement from House Budget Committee Chairman Jodey Arrington (R-TX) and a report from the Heritage Foundation noted that prices had risen by 17 percent since January 2021. The 17.1 percent inflation rate reported by Congressman Arrington and the Heritage Foundation is the percentage change over 31 months. The average inflation rate over this period was 6.3 percent. But this average masks large changes in the rate of change in prices between the beginning of 2021 and the end of 2023; from 7.6 percent over the January 2021 to January 2022 period, to 8.9 percent in the twelve months ending in June 2022, but subsequently below 4 percent at an annual rate in each month after May 2023.

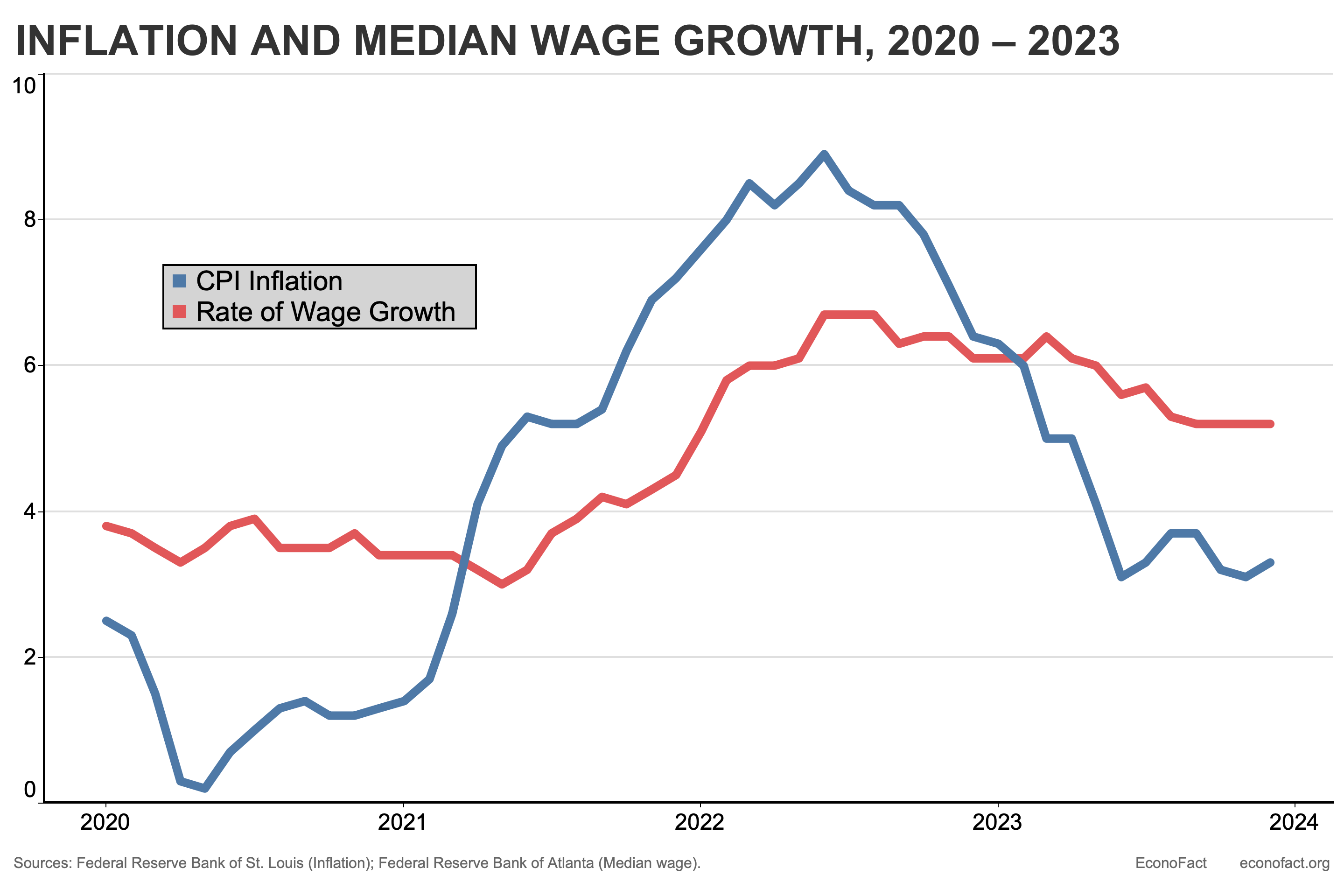

- Wages, as well as prices, tend to rise over time. The relevant statistic for considering the change in people’s purchasing power is not inflation itself but the percentage rise in wages relative to the inflation rate. The Federal Reserve Bank of Atlanta calculates a wage growth tracker for overall median wages as well as for median wages by different levels of educational attainment, full-time or part-time workers, men and women, hourly workers, and workers in service industries. While inflation exceeded wage growth from the beginning of 2021 to the end of 2022, the period since then has seen wage growth higher than inflation (see chart). The increase in median wages was 16.2 percent over the period 2021 to 2023, roughly corresponding to the period of a 17.1 percent increase in prices cited by Representative Arrington and the Heritage Foundation. This means that the shortfall in purchasing power due to inflation was 0.9 percent.

What this Means:

When inflation is coming down, but is still positive, prices will continue to be higher, albeit at a slower rate of increase. All else equal, this would erode people’s purchasing power, but wages tend to rise with prices and living standards increase over time – one indicator of this fact is that real (price-adjusted) national income per person was $67,036 in the third quarter of 2023 (expressed in 2017 prices), six percent larger than its value of $63,227 in the first quarter of 2021. Of course, this aggregate measure does not take into account the distribution of income across different groups. Wage growth across groups varies, as does the cost of respective baskets of goods and services. This is prompting serious study of inflation across income categories and age groups, which is important for gauging relative prosperity as well as properly adjusting benefits to keep up with the cost of purchases. The good news is that inflation is coming down. This is somewhat tempered by the fact that prices are high – but for many people, wage gains soften this blow.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.