Why Did the Fed Change Its Framework? And Why Does It Matter?

Harvard Kennedy School

The Issue:

Over the past two years, the Federal Reserve did something it had never done before: It conducted a systematic evaluation of its policy framework, to see how well it had done at delivering economic prosperity to the U.S. population, and whether alternative approaches to conducting monetary policy might do better. To be sure, changes both large and small have occurred over the Fed’s 107-year history. But this is the first time it has explicitly conducted a comprehensive review of its tools, strategies and communications — the basic elements of its “framework” (in full disclosure, I participated in this process). The Fed conducted this review because the current economic environment poses significant challenges to the Fed’s ability to achieve its congressionally mandated objectives of low, stable inflation and maximum sustainable employment. The new framework implies a marked policy change that likely portends keeping interest rates lower for longer as well as letting the economy run "hot" in ways that could yield benefits to low-income and minority communities. But, it is not without risks.

The Fed's new framework implies letting the economy run "hot" in ways that could yield benefits to low-income and minority communities.

The Facts:

- Interest rates that have been low — and are likely to remain so — coupled with persistently low inflation, present challenges for the Fed. The rate paid on 10-year Treasury bonds has averaged just above 2% for the past 10 years. In contrast, that average was about 4% during the preceding 10-year period, and it was 6% for the decade before that. Short-term interest rates, like the one that the Fed typically uses to influence the economy, have fallen by similar amounts. This appears to reflect an underlying real (inflation-adjusted) rate of interest that has slipped significantly over the same period. In addition, inflation has remained stubbornly below the Fed’s two percent goal: Over the past 10 years, the inflation rate based on the Fed’s preferred personal consumption expenditures chain-type price index measure has averaged 1.5 percent. Likely as a consequence, inflation expectations — especially expectations of inflation further in the future — have also come down. Interest rates decrease as realized and expected inflation decline, since the interest rate accepted by a borrower reflects, in part, compensation for being paid back in dollars whose value may be eroded by inflation (see here).

- Why do these conditions represent challenges for the Fed? Traditionally, the Fed offsets economic weakness by lowering short-term interest rates. Because it is difficult to lower rates much below zero, a lower interest rate at the start of a recession implies less room to lower rates to offset a recession. Prior to the pandemic-induced recession, for example, the federal funds rate was just above 1.5%. The average amount that the Fed has lowered rates in response to recessions has been about five percentage points. So the Fed at the outset of the COVID recession had less than one-third its normal interest rate ammunition to use in offsetting the downturn. As for expectations, a decline in longer-run inflation expectations signals skepticism that the Fed will be able to return inflation to its 2% goal, even in the longer-term. And a decline in such inflation expectations can also feed directly into realized inflation, keeping it lower than it would otherwise be. So expectations that are no longer “anchored” on the Fed’s 2% inflation goal can also make it difficult for the Fed to achieve its objectives.

- Since the Great Recession and financial crisis of 2007-2009, the Fed has also used so-called unconventional policy tools. But their effectiveness is also limited by current economic conditions. Most notable among these unconventional tools has been the purchase of longer-term bonds, with the goal of lowering the rates on these assets once the Fed had lowered the federal funds rate as low as it could. Because those longer-term interest rates are more closely tied to real economic activity — business borrowing, mortgages, and auto loans, for example — they are really the rates that conventional policy aims to influence. So unconventional policy is simply acting directly on the rates that conventional policy tries to affect indirectly. But here, too, the amount of policy ammunition is limited in current circumstances. With the 10-year Treasury rate below one percent for most of this year, there is only so much the Fed can hope to lower these rates by purchasing Treasury and related bonds.

- The Fed adopted two major changes to its framework, with the hope of providing more policy punch to offset recessions. First, it redefined its inflation goal in terms of the average rate of inflation, rather than the rate of inflation at a point in time. As the language in the new framework document describes it: “In order to anchor longer-term inflation expectations at this level, the Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.” Second, on the employment front, it highlighted that its primary (or perhaps sole) concern would be with shortfalls of employment relative to its maximum sustainable rate. Times in which employment is estimated to have exceeded its sustainable level will not be a primary focus of policy. “In setting monetary policy, the Committee seeks over time to mitigate shortfalls of employment from the Committee’s assessment of its maximum level …”

- The change in the definition of the Fed's inflation goal likely implies a policy of keeping interest rates lower for longer. Defining the inflation goal in terms of an average “over time” is a way of addressing persistently low inflation and inflation expectations. Under the previous framework, once the Fed attained two percent inflation, its job on the inflation front was done. But in this new framework, the Fed will strive to offset periods of persistently below-2% inflation — which would mechanically mean a lower average rate of inflation — with periods of above-2% inflation, bringing average inflation “over time” back to the two percent goal. But more importantly, the policy that would be implied to achieve this goal would almost surely keep interest rates lower for longer than otherwise. The three important outcomes of such a change in framework are (a) a closer adherence of realized inflation to a two percent average, which in turn would likely (b) keep inflation expectations better-anchored around two percent, and (c) reduce the severity of downturns, as both contemporaneous and expected policy rates would be lower than otherwise, helping to spur economic activity.

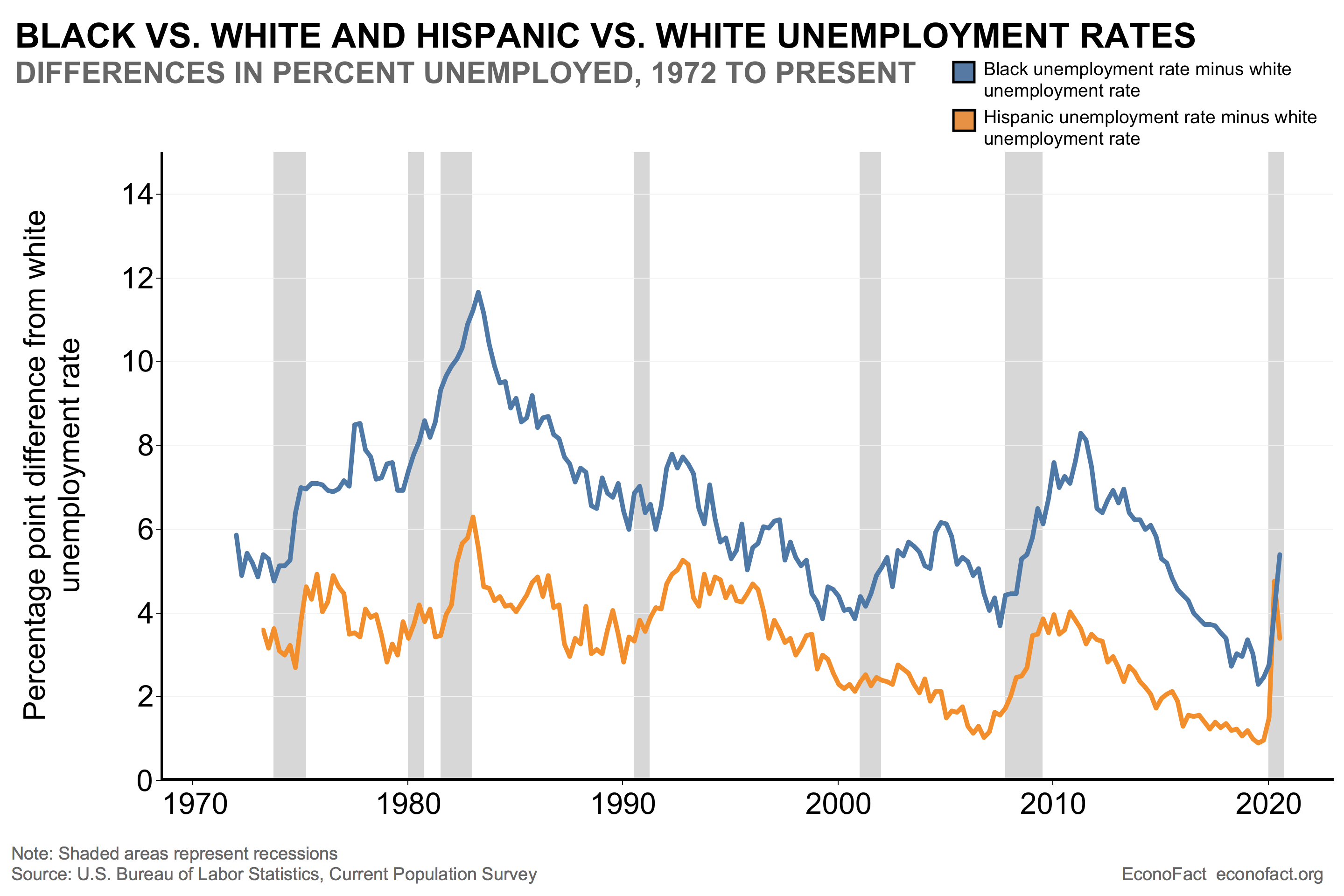

- Looking beyond the current crisis, the Fed's new emphasis on addressing employment shortfalls has an important bearing on income inequality (or more generally the wildly disparate outcomes of the affluent and white versus the poor and communities of color). The shift likely reflects input from the Fed’s “Listening Tour,” conducted between February and October 2019, which engaged representatives of low-income and minority communities, small businesses and retirees, putting monetary policymakers in direct contact with these constituents in a way that had not been typical. In particular, “… participants representing underserved communities generally saw the tight labor market in 2019 as offering significant benefits to their constituents — the main one being job opportunities for individuals who had difficulty finding employment in the past.” Despite the Fed’s repeated description of the overall U.S. labor market in 2019 as “hot,” many participants in the Listening Tour argued that this description did not apply to their specific communities, where unemployment had remained high well into the recovery. In some of these neighborhoods “where unemployment is persistently high — between 15 and 17 percent — ‘it’s always a recession’,” according to some in attendance. This compelling qualitative evidence from poorer, often minority communities is consistent with the unemployment trends observed for Black and Hispanic workers relative to white workers over the business cycle. Indeed, the difference in the unemployment rates between white and minority populations tends to increase during recessions, as Black and Hispanic workers face much larger increases in unemployment, while long recoveries help to lower the gap between white and minority unemployment (see chart). This by itself may suggest a higher tolerance for running a “hot” economy. But the strategy becomes even more compelling when linked with recent macroeconomic experience, in which low levels of unemployment have not been followed by higher inflation. A key puzzle of the past twenty years has been the relative tranquility of inflation in the face of both the Great Recession and the long and ultimately vigorous recovery that followed. Inflation fell little during the Great Recession: The core PCE measure that is often cited by the Fed as reflecting well the underlying trends in total PCE inflation dropped by just about one percentage point, even as unemployment soared to ten percent. By 2011, this measure of inflation had rebounded to a bit above 1.5%. But for the next nine years, it never showed a compelling trend upward toward the 2% goal, even as unemployment plunged to a 50-year low of 3.5%.

What this Means:

The lack of sensitivity of inflation to dramatic changes in economic conditions over the past two decades suggests that the adverse consequences in terms of inflation for allowing the economy to run “hot” seem far less likely to occur these days. If benefits to low-income and minority communities are significant, and inflation costs modest, why worry about a bit of economic overheating? The changes to the Fed's policy framework are likely to allow for the economy to run longer at lower levels of unemployment and low interest rates in the future, opening up the possibility of more widespread benefits across different minority and income groups. However, such a strategy is not without risk. While inflation may not be the outcome of a hot economy, other concerns may lurk in the anxiety closet as macroeconomic imbalances build. Prolonged periods of low interest rates and vigorous growth could lead to bouts of financial instability, although the link there is far from tight. Alternatively, low rates could cause inefficient, excess investment in interest-sensitive sectors, a phenomenon that became all too clear in the housing sector as it unraveled during the Great Recession and financial crisis.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.