How Low Can We Go? Prospects for Negative Interest Rates

Williams College

The Issue:

There is increasing speculation regarding whether the Federal Reserve might set a negative target for the federal funds rate should the economy enter a recession. If it did, the Fed would not be the first central bank to do so. Although negative policy rates have been rare until recently, the European Central Bank has had a negative policy rate since 2015, and recently announced a 10 basis point (0.1%) cut that it would bring it to -0.5%. The Bank of Japan has had a negative policy rate since 2016. Former Federal Reserve Chair Alan Greenspan has said “it was only a matter of time” before the interest rate would fall below zero in the United States.

A negative rate could give the Fed more ammunition to fight a recession. But concerns about efficacy and possible adverse impacts on the banking system suggest that the Fed is likely to be very cautious.

The Facts:

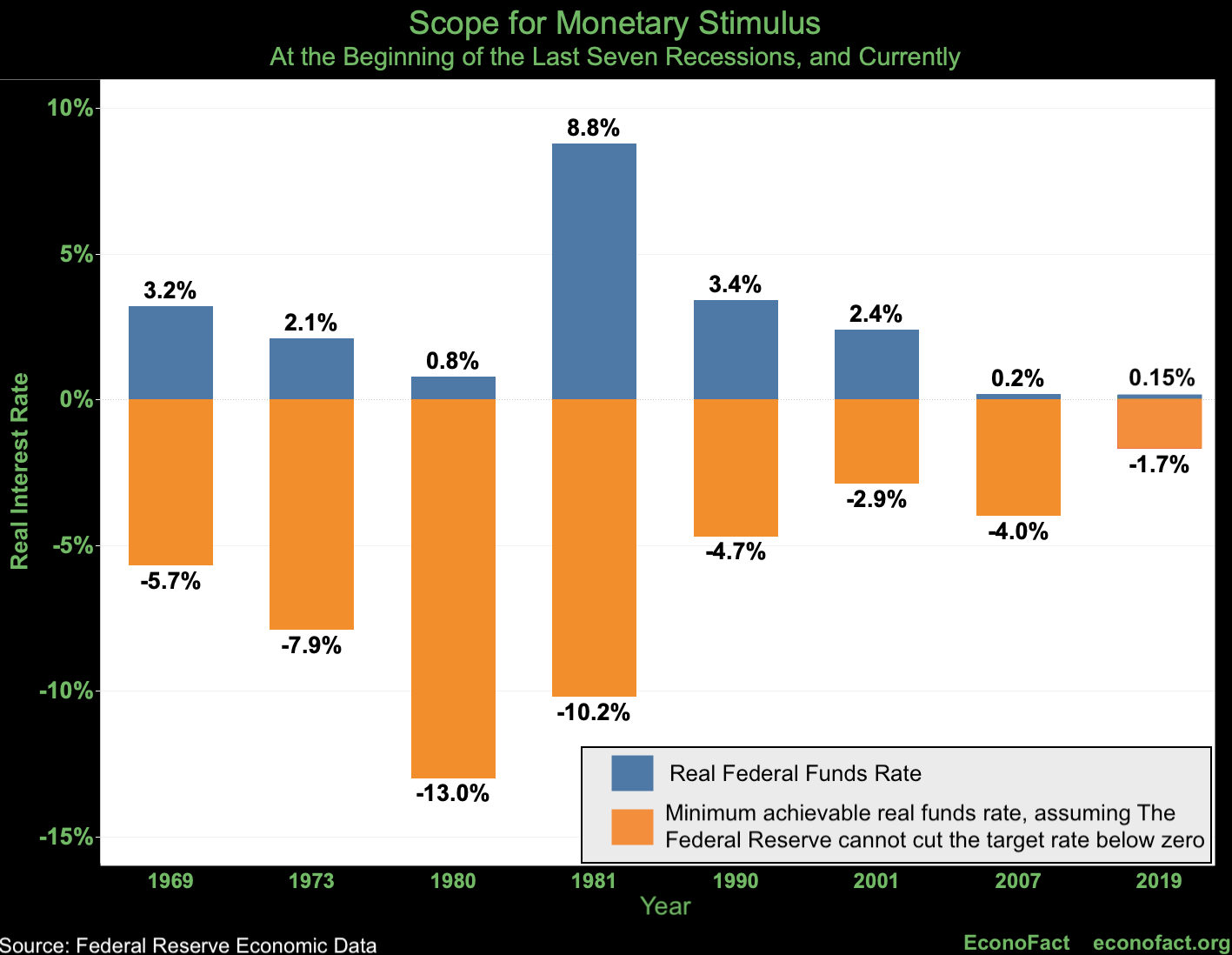

- The purpose of setting a negative funds rate target would be to provide additional monetary stimulus. The federal funds rate is the Fed’s main policy tool. Cuts in the federal funds rate tend to reduce private-sector borrowing costs, and this in turn encourages spending by households and firms. The problem is that with the federal funds rate already so low (in the 1.75 to 2% range, as of the September 18, 2019 meeting), there is very little room for further rate cuts, assuming the Fed stops at zero, as it has in the past. The chart illustrates the Fed’s quandary. The amount of monetary stimulus is measured by the real (inflation adjusted) federal funds rate. The bars above the horizontal axis show the real funds rate at the onset of each of the seven recessions in the past 50 years, plus its level as of September 2019. The bars below the axis show the minimum achievable real funds rate, assuming the Fed cannot cut the target rate below zero, since the real funds rate at a target rate of zero is the negative of the inflation rate. The bars’ overall height represents the amount of interest rate “ammunition” the Fed has as its disposal. The chart shows that if it were to cut the funds rate target to zero, the Fed would be able to achieve only a 2.1% reduction in the real funds rate – far less than in previous recessions. If the Fed could set a negative funds rate, it would be able to achieve a lower real funds rate, thus giving it more ammunition with which to fight a recession.

- The federal funds rate could become negative if the Federal Reserve charged banks for holding their reserve balances. Commercial banks, such as JP Morgan and Citi, currently earn interest on the funds (specifically, excess reserve balances) held at the Fed. The Fed manages the target federal funds rate by changing the interest rate it pays on excess reserves, known as the IOER (interest rate on excess reserves). Setting a negative IOER means commercial banks pay to deposit funds at the Fed. The federal funds rate, the rate at which commercial banks lend funds to each other, would presumably also fall below zero. In addition, commercial banks may set negative interest rates on some retail accounts, effectively making depositors pay to have banks hold money in their accounts.

- There is a practical limit on how far below zero interest rates can fall. The fact that banks and households can hold currency, which pays zero interest, sets an “effective lower bound” on the federal funds rate, and the rates on other short-term liquid assets. Commercial banks and households will be willing to pay for the privilege to hold deposits because holding cash is costly and inconvenient, but only up to a point. Pushing rates too far below zero will eventually lead individuals and institutions to move a significant volume of funds into cash — such as the proverbial cash under the mattress — in order to avoid the cost of holding deposits.

- The stimulative effects of a negative federal funds may be limited. In order for a negative policy rate to have the desired effects, other interest rates, such as those on bank loans, corporate bonds, and home mortgages, would also have to fall. The 10-year Treasury rate, the benchmark for corporate and mortgage rates, is already near its historic lows (less than 2%) so there is not much scope for further reductions. In addition, changes in the funds rate are typically not fully reflected in these rates. It is unlikely that a cut in the funds from zero to negative 50 basis points (half a percent) would lead to more than a 15 basis point reduction in the 10-year Treasury yield. (The magnitude of the reduction largely depends on how long the policy is expected to last.) The effects on bank lending rates are also likely to be small. In Sweden, for example, loan rates have not fallen along with the ECB’s policy rate, as had been hoped. Moreover, negative interest rates entail banks paying the central bank, which squeezes profits and could dampen loan supply.

- Lower interest rates would reduce the government’s borrowing costs, but only gradually. All else equal, a reduction in the federal funds rate that led to a reduction in interest rates on the U.S. Treasury debt would lighten the government’s debt burden and allow it to sustain a higher debt-to-GDP ratio. This would take time, however, as any cuts in the federal funds rate would not reduce the interest being paid on the existing stock of debt. The government would benefit from reduced borrowing costs only as the maturing debt is “rolled over” into newly issued securities with lower rates. (Unlike some corporate debt, U.S. Treasury securities cannot be retired, or “called,” before maturity.) With only 28% of government debt maturing within one year, the near-term benefits will therefore be relatively modest (see Table FD-5). In any case, reducing the debt burden should not be an objective for monetary policy, whose paramount goal is to ensure macroeconomic stability, not to make it easy for the government to run large budget deficits.

- The Fed may lack the legal authority to set a negative policy rate. As mentioned previously, pushing the federal funds rate into negative territory would require a negative IOER, meaning that banks would have to pay to carry balances in their reserve accounts. The Fed has the authority to pay (positive) interest on banks’ excess reserves, but an internal Federal Reserve Board memorandum from 2010 acknowledges that the legal basis for a negative IOER is questionable.

What this Means:

The Fed’s self-imposed zero lower limit on the target has in the past constrained the scope for rate cuts during recessions. Given the low interest rates and low inflation that have persisted since the end of the Great Recession, the Federal Reserve does not have much room to stimulate the economy with traditional monetary policy tools should the economy fall into recession. A negative rate policy would complement the Quantitative Easing (QE) and forward guidance measures it implemented in 2009, during the previous recession. The U.S. economy is not yet at that point, however, as GDP growth is steady and the unemployment rate remains low; in fact, the current funds rate target is still well below what would normally be warranted by economic conditions. In addition, concerns about the policies’ efficacy and possible adverse impacts on the banking system suggest that the Fed is likely to be very cautious in implementing a negative rate policy.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.