The Case For Protecting Student Loan Borrowers

·July 17, 2017

University of Michigan

University of Michigan

The Issue:

Debt from student loans has grown rapidly over the past decade. Policies that regulate the management and oversight of student loans impact over 40 million U.S. households. Since taking office as U.S. Secretary of Education, Betsy DeVos has taken measures to roll back some Obama-era regulations designed to limit fees and to ensure accountability of the private companies that manage federal student loans. At the same time, the Trump administration and Republicans in Congress have signaled a push to limit the powers of the Consumer Financial Protection Bureau, which is one agency outside the Department of Education that has taken a lead consumer advocate role over the student loan industry. How will these moves impact student borrowers?Students cannot choose the loan servicing company that manages their federal student loans — they are locked in with the private contractor assigned to them.

The Facts:

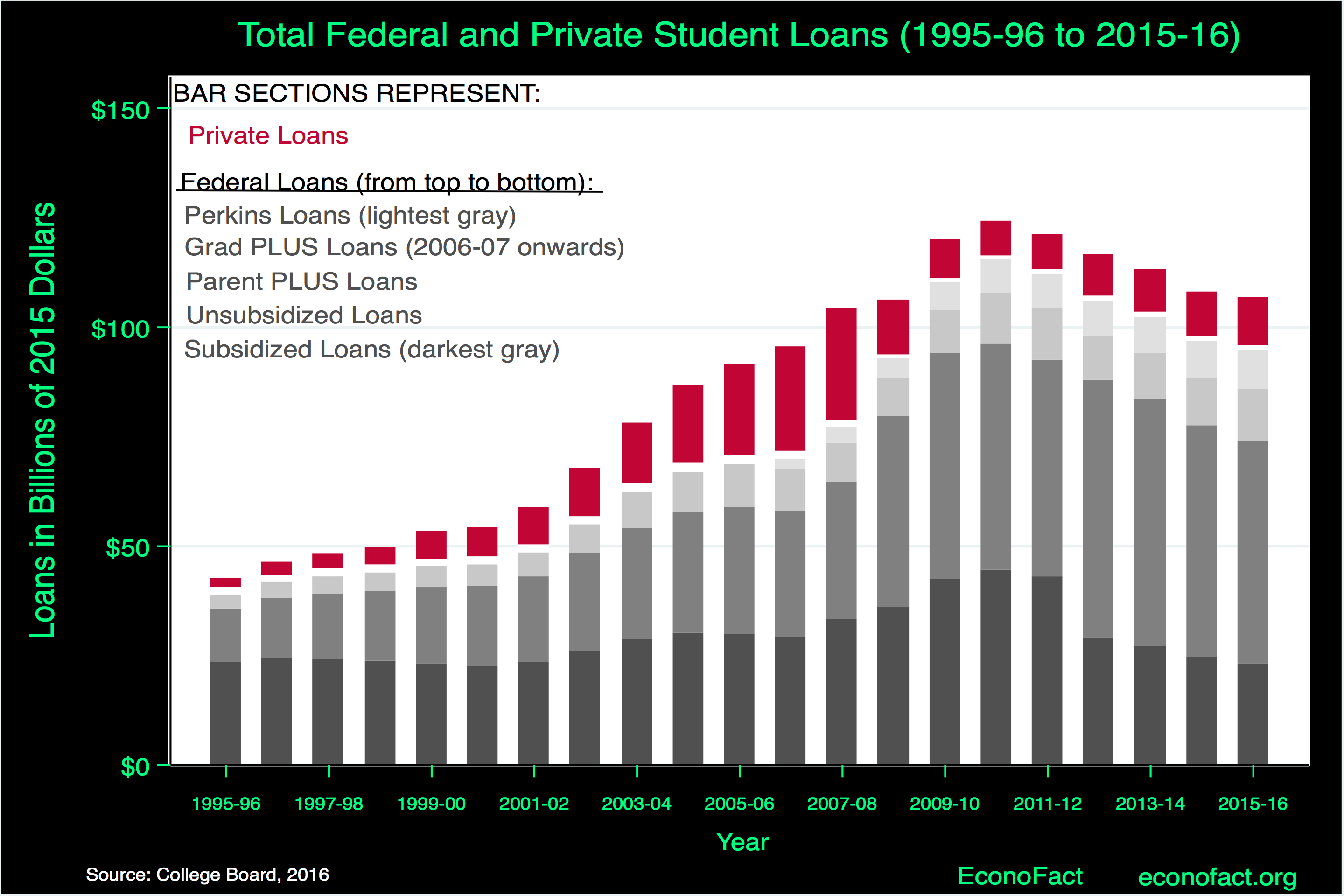

- Student loans increasingly matter for the economy and for millions of households. The U.S. Department of Education administers around $1.3 trillion in loans on behalf of nearly 43 million student borrowers. This is more than double the $611 billion owed less than ten years ago. As state funding for higher education has declined and tuition costs have continued to increase, students and families have increasingly turned to student loans. The outstanding balance on student loans has grown because more students are taking out loans, the loan amounts have increased, and the speed with which students repay their loans has slowed (see this working paper for historical trends and for the latest figures as of 2017 see this update from the Federal Reserve Bank of New York). As a result, student loans are now second to mortgages as a component of household debt: outstripping auto loans and credit cards, and making up 11 percent of household debt — up from 5 percent in the third quarter of 2008.

- The U.S. federal government is by far the largest provider of student loans. Student loans provided by private lenders comprised only around 10 percent of annual loans to students over the past decade and this form of lending declined during the Great Recession while government loans continued to rise (see chart).

- There is an economic rationale for government involvement in loans to students: Education is an investment that promises future returns in the form of increased earnings but involves present costs and foregone earnings while students are in school. Unlike a business deal or a mortgage, where borrowers can secure loans with capital goods such as machinery or a building, students have little to put up as collateral for the loan. This makes lenders more reluctant to lend and more likely to demand higher interest rates. Unlike federal loans, the private loans available to students require a creditworthy borrower or cosigner. The public sectors of most developed economies and many developing countries provide loans to students.

- While the federal government provides the funds, private companies are in charge of "servicing" them: collecting payments, keeping records and communicating with borrowers. From the beginning of the modern student loan program in 1965, federal student loans have been a joint venture between the government and the private sector in the United States (see here for a history). But the participation of the private sector in the federal student loan program has been scaled back since 2010 when the federal government became the sole provider of funds. However, a patchwork of nine private loan servicing companies remain in charge of sending bills to borrowers, collecting payments and handling any problems that arise.

- Student borrowers have no means by which to select the company servicing their loans. Borrowers are assigned to private loan servicing companies and cannot switch companies if they are unsatisfied with the customer service they receive.

- The Consumer Financial Protection Bureau, which maintains a database of consumer complaints about financial products, has documented thousands of reports in which students complain about the way in which their payments are being handled or problems with the fees or interest rates charged. In January, the bureau took a step further and filed a lawsuit against Navient, the nation's largest student loan company, for allegedly failing borrowers at every step of repayment and claiming it “illegally cheated borrowers out of repayment rights through shortcuts and deception.” While the legal case evolves, the CFPB's independence and ability to take on a strong advocacy role has increasingly become a target for reform. Presently, the CFPB has a budget that is isolated from political pressure and its director can be ousted only for “inefficiency, neglect of duty or malfeasance in office.” But, new legislation under the Republican sponsored CHOICE Act would allow the director to be fired by the President 'at will' and would significantly weaken the bureau's powers.

- The U.S. Department of Education has been moving toward less stringent criteria for awarding loan management contracts to private contractors as well as toward allowing for higher fees. The U.S. Department of Education allocates contracts with loan companies based on their collection performance by considering criteria such as the default rate on their loans. The Obama administration had added instructions to give weight to a company's track record and steer away from companies with histories of shoddy service. This guidance would presumably count against providers such as Navient, given the lawsuit in progress. However, the under the leadership of DeVos, the Department of Education has since rescinded this guidance. Similarly, in 2015, the Obama administration had limited the ability that loan companies had to impose punitive fees from borrowers who were in default (which could in some cases be as much as 16 percent of the amount in default). In March, the Department of Education overturned this position.

What this Means:

Students cannot vote with their feet by moving to the loan servicing company that provides them with the best service — they are locked in with the contractor assigned to them by the Education Department. For this reason, deregulating loan servicing companies is unlikely to increase competition that leads to innovation or improved services for borrowers. Moreover, as a captive market, if the government does not monitor these companies, borrowers are at risk.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.

Written by The EconoFact Network. To contact with any questions or comments, please email contact@econofact.org.