COVID-19 Social Insurance Payments to U.S. Households

University of Maryland

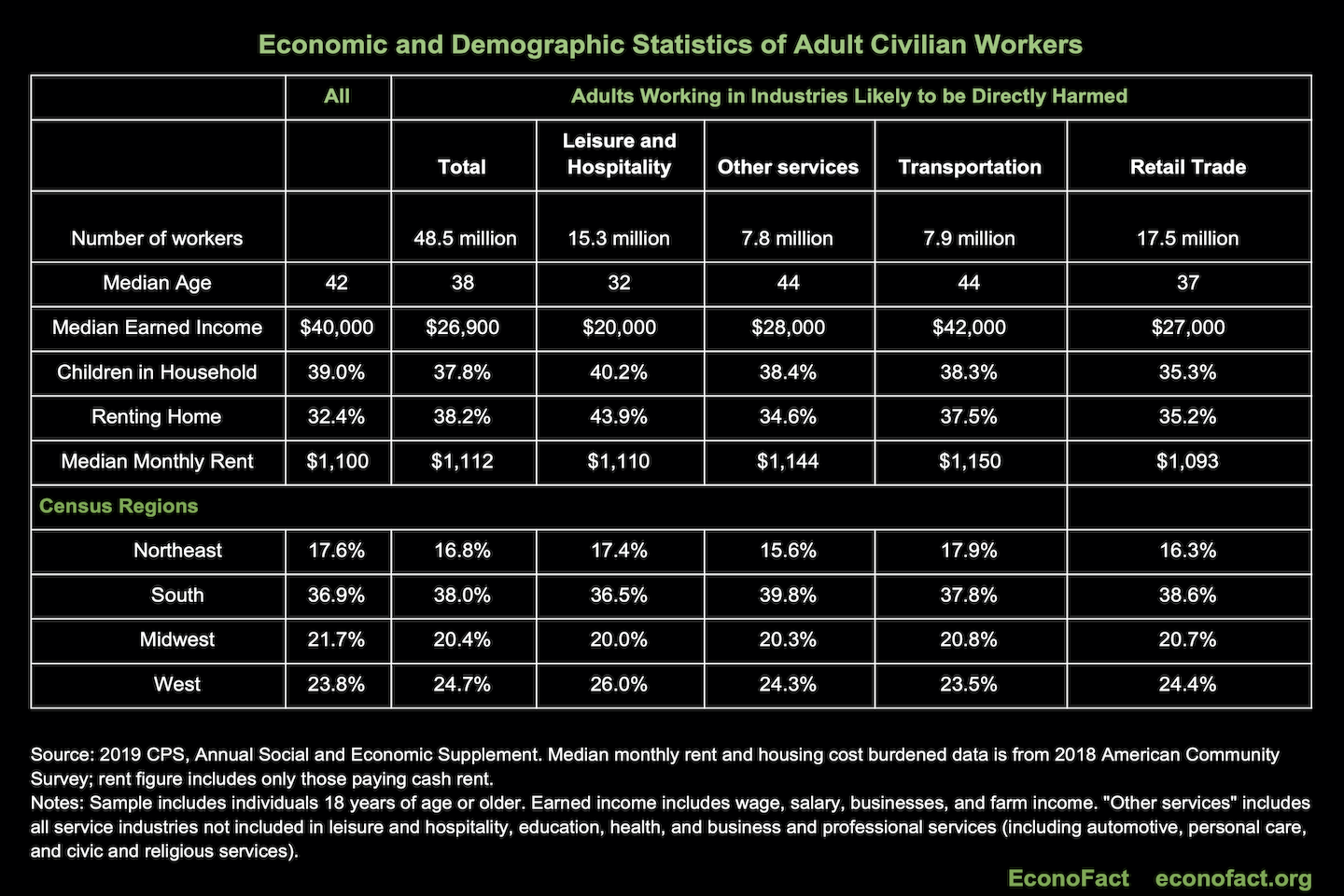

(Click here for a larger version.)

The Issue:

The United States government is gearing up to issue immediate direct payments to individuals to provide a financial lifeline at this time of income loss due to business closures and reduced demand for work and services. Such payments would provide an important measure of social insurance to maintain necessary spending on things like housing and food. Practical considerations make it difficult to perfectly target the payments to people who are likely to experience pandemic-induced job loss, but estimates suggest that many millions of Americans and more than a third of workers are likely to need income assistance during this economic slowdown.

Cash payments provide a financial lifeline through this time of income loss. Workers in the hardest hit industries have low earnings and few savings.

The Facts:

- Immediate cash payments, in the form of rebates, to U.S. adults during the coronavirus crisis would act as a form of social insurance to help people smooth consumption – that is, lessen their reduction in spending on goods and services – through a period of income loss. Social insurance refers to the government provision of insurance payments to individuals who experience financial challenges in contexts where market failures prevent a well-functioning private insurance market. Perhaps the most well-known example of social insurance is the federal social security program, which is meant to ensure that individuals who can no longer work do not fall into poverty in their old age. Cash payments to individuals at a time of sudden and severe income loss owing to a coronavirus pandemic is a prime example of when social insurance is needed, because private insurance is not available and full self-insurance through people’s own savings is highly improbable. Most American households do not have enough savings that they can readily access to insure themselves against the kind of large financial shock the current pandemic could cause. Only about 40 percent of families have accessible savings equivalent to at least three months of expenses, and less than 30 percent have an equivalent to at least six months of expenses, according to estimates by economists at the Federal Reserve Board.

- Who are the workers most likely to need emergency income support during the coronavirus crisis? It is extremely difficult to predict how many of the 164.4 million people who report working for pay at any point during the previous year (representing two-thirds of the roughly 250 million non-institutionalized civilian adults in the United States) will experience reduced hours or earnings as a result of the current coronavirus-related economic slowdown. This will depend on the length of time it takes to slow or halt the rate of virus transmission and the geographic spread of the pandemic. Nonetheless, an analysis by Moody’s Investors Service suggests that the industries likely to experience the greatest financial risks are passenger airlines, gaming, automotive, transportation/services, lodging, leisure, restaurants, and apparel. These industries can be aggregated into four broad categories: leisure and hospitality, transportation, other services, and retail. Workers in these four industries account for nearly 30 percent of the workforce (see table). The median incomes for workers in these four industries are below the national median of $48,700 for full-time wage and salary workers; $20,000 for leisure and hospitality, $42,000 in transportation, $27,000 in retail and $28,000 in other services. More than a third of workers in these four hard-hit industries have children living in their households who need to be fed, sheltered, and cared for. Immediate cash assistance will help families meet children’s basic needs through this crisis. Workers in these industries are spread throughout the country with 17 percent in the Northeast, 38 percent in the South, 20 percent in the Midwest and 25 percent in the West. We also know from existing economic research that male job loss is associated with increased rates of child maltreatment, a link that compounds the imperative of assisting families and getting the economy back on track as quickly as possible.

- The need for assistance will surely extend beyond workers in these four industries. There are also the overburdened workers on the “front lines” of the pandemic: 7.7 million workers in hospitals and another 11 million in health care services outside of hospitals, who will experience hardship throughout this crisis. These workers are certainly directly affected, though in a different way than workers whose jobs are being eliminated or hours reduced.

- The greatest per dollar social benefit of COVID-19 social insurance payments would come from targeting payments to those who are most affected and have the least means to deal with it, but this type of targeting of immediate assistance is impractical. Targeting is impractical in this highly unusual time. For instance, the federal government cannot readily observe who works in a non-salaried job with hours that are about to be cut or wholly eliminated. Nor can the federal government readily gauge whether someone has access to sufficient savings. The federal government could provide financial support to small and medium size businesses that are adversely affected, as some economists have proposed. It could also address the potential loss of housing during this crisis is through mortgage forbearance, as the Federal Housing Finance Agency has issued, and a corresponding moratorium on evictions for renters. But practical considerations dictate that broad based income-based payments are likely the most expedient option. People who receive payment but feel the cash assistance is not needed and want to help the wider community could donate to local charities and food banks that are well-equipped to get the resources to individuals in need, or to buy gift certificates to local businesses or pre-pay for future services to help their favorite local small businesses pay their current expenses.

- Who Will COVID-19 Payments Help? We have used the NBER TAXSIM model to simulate the distributional effects of the proposed payments included in the March 25, 2020 version of the Senate CARES Act (Coronavirus Aid, Relief, and Economic Security Act). This would provide a $1,200 refundable tax credit for individuals, with $2,400 for joint filers. There would be no minimum qualifying income requirements and no phase-in. Additionally, taxpayers with qualifying children will receive a $500 rebate for each child. The rebate phases out at $75,000 for singles, $112,500 for heads of household, and $150,000 for joint taxpayers at 5 percent per dollar of qualified income. This means that single taxpayers making over $99,000 and joint taxpayers making over $198,000 combined will not receive a payment. Actual rebates are calculated using income from the most recently filed tax return, 2019 if the taxpayer has already filed this year or 2018 if not. Our estimates (based on 2018 income data, the most recent data available) suggest that these refundable rebates would pay on the order of $233 billion directly to households, assuming complete take-up. They would yield $39.7 billion in cash assistance to households that report $22,556 or less in adjusted gross income (17 percent of rebate dollars); $47.2 billion to households that report between $22,557 and $50,133 (20 percent); $53.7 billion to households that report between $50,134 and $82,706 (23 percent of rebate dollars); $57.2 billion to households that report between $82,707 and $134,512 (24 percent of rebate dollars); and $34.7 billion to households that report over $132,512 in adjusted gross income in the year 2018 (15 percent). But note that the distribution of payments will not be made according to income in 2020, which means some households that had high income in 2018 but low income in 2020 might not get payments they would otherwise qualify for. Our estimates further show that 43.1 percent of the households who would receive a check have at least one child under the age of 18 in the household and that 31.8 percent are renters. About one-quarter of the rebate money would go to adults working in the four industries that are expected to be particularly hard hit. About one-fifth of the rebates would go to individuals who did not work last year.

- How much will COVID-19 payments to households cost the federal government? Our estimate of a total cost of $233 billion is lower than an estimate from the Penn-Wharton Budget Model of $270 billion and an estimate of $301 billion provided by The Tax Foundation (whose estimates are based on a general equilibrium model.) We offer a rough gauge since we are using only 2018 income and the ultimate cost will depend upon the share of households that take up these payments. To put the magnitude of these numbers in context, per the U.S. Joint Committee on Taxation, the annual decrease in federal revenue associated with other well-known tax deductions and credits include $146.1 billion for the exclusion of employer contributions to health care and health insurance premiums, $49.2 billion for subsidies for health insurance purchased through health insurance exchanges, $70.1 billion for the earned income tax credit (EITC), $33.7 billion for the mortgage interest deduction for owner-occupied residences, and $37.4 billion for the exclusion of capital gains at death.

- A coronavirus emergency payments policy is not a guaranteed universal basic income (UBI). These payments will take place during the emergency and are not meant to be ongoing, unlike what advocates for UBI have called for in response to challenges associated with income inequality and potential job loss on account of factors like robots and technology. One of us (Kearney) has argued against UBI in favor of a combination of safety net programs that target individuals who have observable measures of need and policies that encourage work and human capital development. Such arguments do not apply in the current context. In a time of national emergency when governors and mayors are mandating that non-essential businesses close and individuals are being encouraged to stay home. Social insurance payments should not be withheld out of a worry that such redistribution will keep people from going to work, as some have suggested. Furthermore, there is a critical distinction between short-term payments to help individuals through a difficult period when business activity is expressly being restricted for the sake of public health and a permanent guarantee of income maintenance during normal times.

- In addition to the social insurance and consumption smoothing benefits of these payments to individuals and families, the payments will have a fiscal stimulus effect of lessening the decline in aggregate spending in the economy. However, we should not expect that the stimulus effects of individual cash payments during this crisis will be akin to the effect of previous recession stimulus payments, as in 2001 and 2008. Research has found that the 2008 stimulus payments led to increases in household spending with the largest increases for older, lower-income, and home-owning households. A crucial distinction is that the payments to households during the COVID-19 crisis would be disbursed at a time when individuals are being told to stay home and practice social distancing, and there is great uncertainty about the depth and length of the underlying public health crisis. But, speculation that the fiscal stimulus effects of individual payments during this crisis will yield smaller fiscal stimulus effects than previous rebate checks should not detract from the important social insurance value the checks would provide to individuals and families facing large income losses and economic insecurity.

What this Means:

The current COVID-19 pandemic has devastating effects on individuals and families. Our nation’s first priority must be to stem the spread of the virus and its harmful health and mortality effects. Along with this, there is also a need to help people through this time of income loss owing to business closures and reduced demand for work and services with immediate, short-term cash payments. Given the practical difficulties with targeting payments, and the need to provide cash assistance quickly, broad-based income-based payments make good policy sense (and efforts need to be made to ensure that the most vulnerable are reached in this program). Our analysis finds that the payments currently being proposed under the Senate CARES Act would deliver large sums of money to individuals working in industries expected to be most hard hit, and to families with children. Moreover, there would be an indirect broader benefit by lessening the decline in aggregate spending in the economy. Such payments should be part of a multi-pronged policy response, that should also include expansions of the government’s unemployment insurance program, as well as loans to businesses, among other fiscal and monetary responses.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.