How the U.S. Fell Behind in Adopting the Electric Car

EconoFact

The Issue:

Adoption of electric cars has taken off globally — electric vehicles (EVs) made up a quarter of new car sales in the world in 2025. The United States was in the lead in launching the modern electric car — Tesla’s Model S was first delivered in 2012 — and, until recently, U.S. policies provided substantial encouragement to auto manufacturers and households to adopt the technology. However, China has dominated the recent global surge in production and sales of EVs, and Europe has also overtaken the U.S. in EV adoption. What explains the U.S.’s lagging performance?

The relatively slow rate of EV adoption in the U.S. is a function of national characteristics, as well as government policies.

The Facts:

- The plug-in battery-powered modern revival of EVs was led by Tesla in the United States from 2012. In fact, EVs are not a new innovation; they predated gasoline cars and represented one-third of U.S. motor vehicles at the start of the 20th century. However, their presence was quickly eclipsed by gasoline-powered internal combustion engine vehicles, which benefitted from the falling cost of mass-produced gasoline-powered cars, the discovery of cheap crude oil that reduced the price of gasoline, and the demand for longer driving ranges on expanding road networks. Electric-powered cars started their comeback in 1997 when Toyota introduced the Prius, a hybrid car that combines a gasoline and an electric engine, but not a plug-in battery (and thus is not formally classified as an EV). In recent years, there has been a proliferation of EV models beyond those produced by Tesla, particularly in China and Europe, both in the form of fully battery-powered cars and plug-in hybrids, as well as the introduction of electric trucks, buses, and 2-3 wheelers.

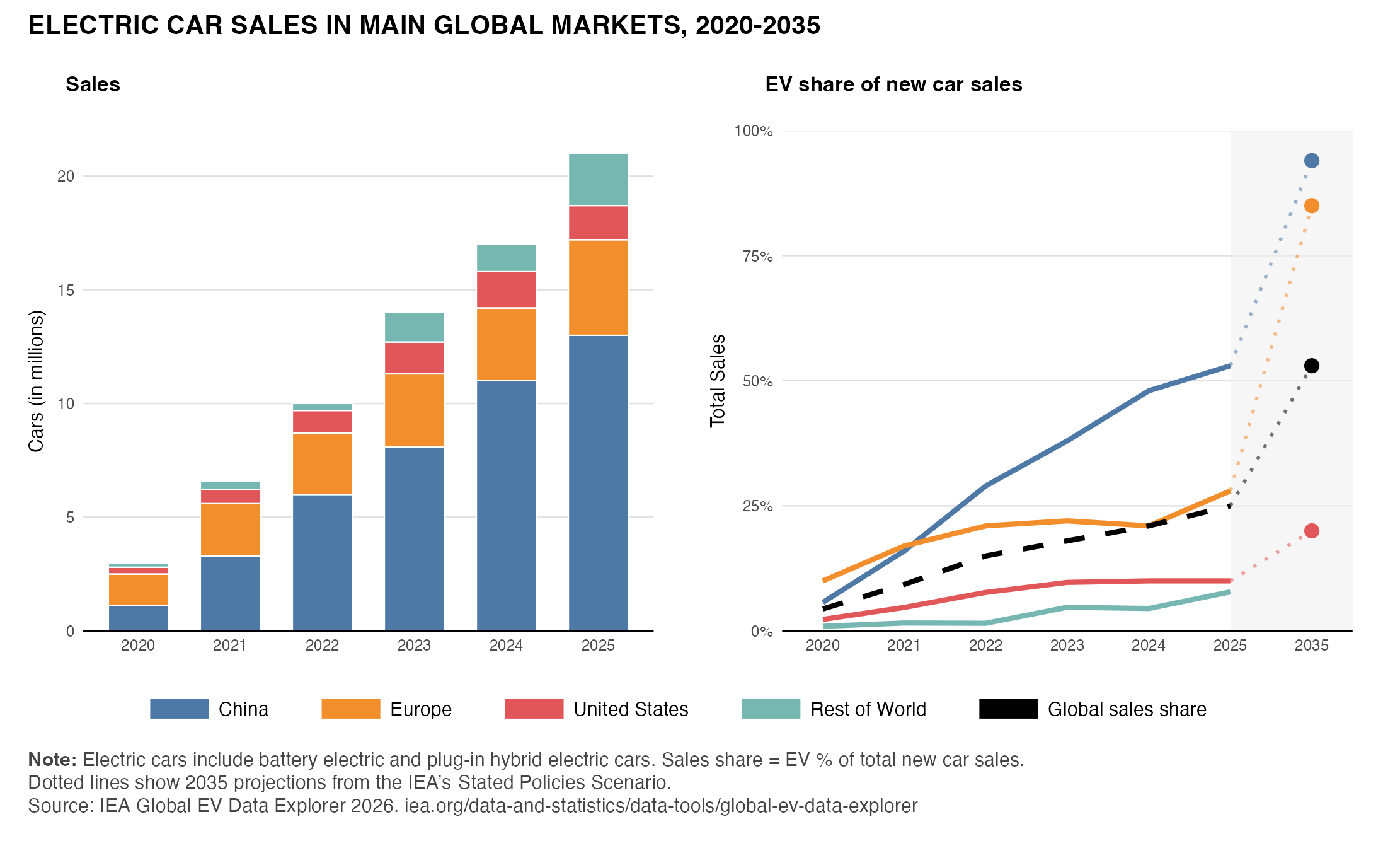

- EV sales surged 20 percent globally in 2025 to more than 20 million vehicles. China is now by far the largest market for EVs. More than 13 million electric cars were sold in China in 2025, where 55 percent of new vehicle sales were EVs (see chart). The European Union (EU) is in second place, with EVs accounting for 28 percent of sales after a strong increase in 2025 related to greater availability of low price models in response to tightening emissions standards. By contrast, new sales of EVs were flat in the United States amounting to 1.5 million vehicles in 2025, around 10 percent of sales.

- China is the world leader in the manufacture of EVs by an even greater margin, followed by the EU and then the United States. China accounted for 75 percent of global production in 2025, producing 15.9 million EVs, while the EU produced 3.2 million. The United States produced just 1 million EVs in 2025, around 5-7 percent of U.S. auto production, about half of which are manufactured by Tesla. Chinese production was initially led by foreign-owned companies (including Tesla) and joint ventures, but now production is primarily by domestic companies like BNY and Xiaomi. China also dominates global EV exports, even though it is shut out of the US market by high tariff barriers. The U.S. does retain some lead in certain market segments — such as large luxury vehicles and in software-driven self-driving technologies — but has little presence in smaller and more affordable models.

- The global surge in adoption of EVs has been boosted by wide-ranging public policies in many countries. Countries have encouraged EV sales to gain from a variety of possible economic and social benefits from their adoption: to reduce emissions of pollutants; to contribute to containing the global carbon footprint; and to help diversify energy sources to increase energy and security resilience, especially for countries that must import much of their hydrocarbon fuels. Some countries have also encouraged EV production, seeing benefits from achieving technological leadership, for example in battery manufacture, and the creation of integrated supply chains and economies of scale to support a healthy automobile sector and associated manufacturing jobs.

- The U.S. was an initial leader in providing policy incentives for EV adoption, but this support has been sharply curtailed. The Obama administration expanded an existing tax credit for EV purchases, provided loan guarantees for EV production investments, and offered support for battery manufacture and building out the charging infrastructure, while increased fuel economy standards encouraged auto manufacturers to shift towards lower emissions vehicles. This framework largely remained in place during the first Trump administration and was expanded during the Biden administration. However, the second Trump Administration eliminated the EV tax credit as of September 2025, cut back public support for the charging network, and has sought to ease fuel economy standards, while retaining a 100 percent import tariff on Chinese EVs imposed in 2024 — which protects domestic car manufacturers but does not support EV sales (see pg. 202).

- Policy support for EVs has been most comprehensive in China. It formally adopted EVs as a strategic industry in 2012 and has provided extensive support to EV manufacturers and battery suppliers as well as sales tax exemptions and registration incentives to purchasers. European fiscal support has also been larger in total than in the United States, varying country by country, although it has typically been lower on a per car sold basis. As the technology has become better established, EV subsidies have been scaled back recently in China and Europe, lowering the public share of spending per vehicle, but both countries retain broader policy frameworks to encourage the transition to EVs than the United States.

- The relatively slow rate of EV adoption in the United States is a function of national characteristics, as well as government policies. EV adoption in the U.S. was clearly falling behind that of other regions despite the relatively generous EV subsidies under the Obama and Biden administrations even before the rollback of fiscal incentives and environmental standards in the second Trump administration. There are several structural reasons for this. First, gasoline excise taxes in the United States are substantially lower than in China and Europe, so that fuel cost saving from switching to battery power is less. Second, journey distances in the United States are longer, with driving for vacations and visiting family in other states bringing “range anxiety” as long as charging networks are not fully developed and battery charging capacity is constrained. Third, benefitting from wider and less crowded roads, American families have a preference for large SUVs and light trucks, which require large and expensive batteries to run and have greater range issues.

- China’s lead in EV production and sales has been reinforced by network effects and scale economies. An important network effect for EVs is the building up of a dense and efficient physical charging network to increase convenience and reduce range anxiety, and this has been a major focus in China. In 2025, China accounted for more than 65 percent of public charging points globally at the end of 2025 compared to only 3 percent in the U.S., despite the accelerated program launch by the Biden administration. Production scale economies reduce unit production costs and encourage the build-up of supply chains — China’s large EV output and integrated supply chains mean that battery unit manufacturing costs are 30 percent lower than elsewhere. Scale economies also encourage innovation, for example in battery technology, as R&D costs can be spread more widely. As a result, Chinese car buyers can choose among a wide-range of affordable vehicles, which are now typically cheaper than their gas-powered equivalent models.

- By contrast, in the U.S., despite the overall size of the auto market, the EV sector has lacked volume, with a much more limited model range and charging infrastructure and limited investment in other parts of the EV ecosystem like batteries. In consequence, new EVs typically sell at a significant premium to their gas-powered equivalent, and there are few EV models in the lower price segment, discouraging adoption even if total cost of ownership (including fuel and maintenance costs) over the lifetime of an EV may be considerably lower than for an internal combustion vehicle. Moreover, while U.S. investment in EVs was spurred by the Biden Administration’s big push to encourage EV adoption, the traditional auto companies have slashed their plans to introduce new models over the past year as the Trump administration reversed policy support for EVs. Moreover, Tesla has shifted its focus to self-driving technologies and efforts to build out charging networks have slowed.

What this Means:

Going forward, EV adoption is likely to continue advancing rapidly around the world. The International Energy Agency (IEA) projects that the global fleet of EVs would rise six times from 2025 to 2035, as EVs come to account for an average of 50 percent of new sales globally by 2035. In the U.S., the development of new battery technologies providing much greater range and charging efficiency, the fuller build-out of the charging network, and eventual availability of more affordable EV models should help to raise market penetration over the next decade. However, this rise is expected to be much more gradual than in China and the EU, such that the gap in EV production and sales across the regions is likely to continue to widen. The recent jump in international oil prices in the context of the Iran war is raising the cost savings from driving an EV in the U.S. and is reported to be increasing U.S. consumer interest in EVs. However, this factor would if anything reinforce the diverging trend with China and the EU as gasoline in the U.S. remains much cheaper and as EVs remain relatively expensive compared to internal combustion equivalents.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.