The Wealth Tax Debate

Independent Economic Consultant

The Issue:

There have been a number of recent proposals for a wealth tax at both the federal and state levels, which have been driven by several factors. Foremost has been concern about the rapid increase in U.S. income and wealth inequality and the apparent ease with which the wealthy are able to avoid income and estate taxes. Wealth taxes have also been seen as a convenient instrument for raising tax revenues and supporting under-funded social programs. However, these proposals have drawn criticism, including from those who argue that there are other, more effective ways to address inequality and raise revenues.

The wealthy have considerable scope to limit their income and estate tax liabilities. A tax on wealth risks potential economic and administrative costs.

The Facts:

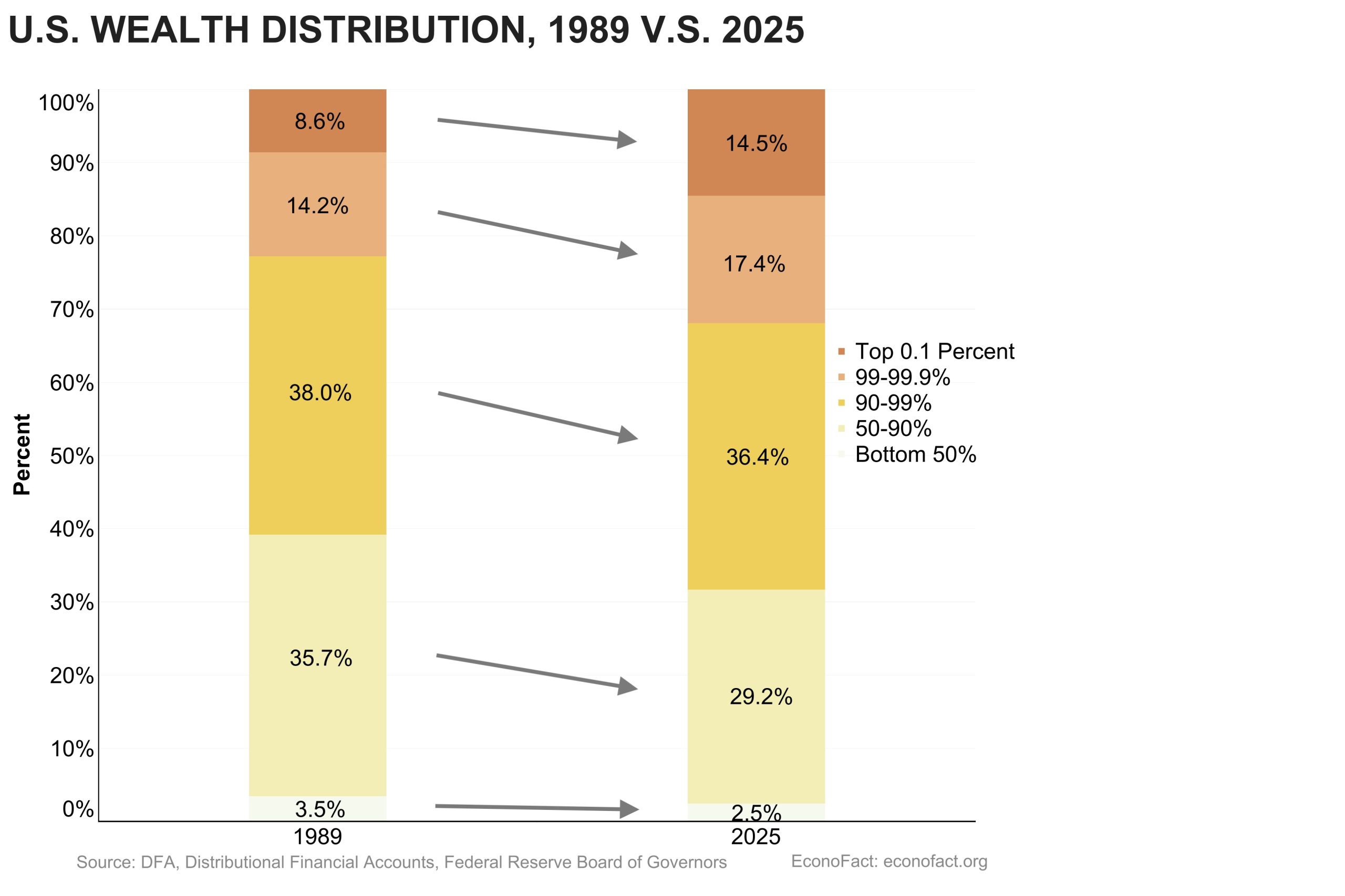

- Income and wealth inequality have risen sharply in the United States since the 1970s. Income inequality has widened steadily since the mid-1970s, and the United States is now considered as one of the most unequal countries among its OECD peers. Income disparities, together with other factors such as the historical legacy of racial discrimination and the sharp runup in asset prices in recent decades, have also led to a corresponding widening of wealth inequality. In 1989, the top 0.1 percent owned 8.6 percent of U.S. wealth. By 2025, their share of U.S. wealth had grown to 14.5 percent with the top 1 percent of the U.S. population estimated to own over 30 percent of wealth (see chart).

- High-income U.S. taxpayers are already subject to higher income tax rates, as well as other taxes that specifically target wealth. The marginal tax rate on income at the federal level rises to a maximum of 37 percent, and while some states do not tax income, the combined rate in California exceeds 50 percent. Annual property taxes on real estate are levied principally at the local level, with rates that can reach as high as 2½ percent in one county in New Jersey. These taxes yield roughly the equivalent of 3 percent of GDP and represent around 30 percent of total state and local tax revenues, providing an important source of funding for local government services. At death, an estate tax is levied by the federal government, with rates that rise to as high as 40 percent, and 17 states and the District of Columbia also impose estate taxes or tax on inheritances.

- However, the wealthy have considerable scope to limit their income and estate tax liabilities. Higher marginal tax rates generally only apply to wages and salaries, while (as in many countries) lower rates apply to investment and business income, to minimize double taxation on corporate income and to limit taxation of savings. These lower rates, as well as the scope for avoidance strategies, including the widespread use of pass-through business entities, favor the very wealthy, who derive a larger share of their income from investment and business sources than from wages and salaries. Although an Alternative Minimum Tax (AMT) is intended to limit the scope for tax avoidance, it still retains a preferential rate for investment income, and studies suggest that the wealthy face a relatively low effective tax rate on total income (here and here). Similarly, although the federal estate tax rate is high, it applies only to assets above a threshold of $15 million for individuals and $30 million for couples. Moreover, there is considerable scope for high-wealth individuals to use trusts and other strategies to remove assets from their taxable estates, leaving revenues from the federal estate tax at only about 0.1 percent of GDP in recent years. In addition, inherited assets benefit from a ‘step-up’ in their valuation for the purposes of calculating capital gains taxes, which significantly limits future tax liabilities for the heirs of wealthy decedents.

- It is also often argued that the wealthy benefit from disproportionate political influence, which can further widen wealth inequality. Studies suggest that the wealthy are able to tilt tax and other policies in their favor, which has the effect of helping to perpetuate wealth inequality and undermining broader confidence in the fairness of U.S. democratic processes (see here and here). Nonetheless, despite repeated efforts in recent decades, it has not been possible to enact legislation that would limit the size of political campaign donations.

- These and related concerns have led to several recent wealth tax proposals at both the federal and state levels. At the federal level, an Ultra Millionaires Tax Act was proposed in 2024. This would apply a 2 percent tax on the net worth of individuals and trusts above $50 million, rising to 3 percent on net worth above $1 billion. The base would include stocks, bonds, private business interests, and real estate. An alternative proposal, the Make Billionaires Pay Their Fair Share Act, would introduce a 5 percent tax on net assets (broadly defined) of over $1 billion. In both cases, the wealth tax would not be deductible from income tax. However, neither of these proposals presently has sufficient support in Congress. At the state level, the proposed 2026 California Billionaire Tax Act (CBTA) would apply a one-time 5 percent tax on the net worth of individuals/trusts of $1 billion or more. The asset base would include personal property, stocks, and financial assets, but exclude directly held real estate, pensions, and retirement accounts. Tax payments could be spread over five years. Illinois has considered the introduction of a 4.95 percent tax on the unrealized capital gains of residents with net assets in excess of $1 billion (see here). The Illinois proposal has not gone forward in the legislature, but supporters of the CBTA aim to have the proposal approved by voters in November 2026.

- Wealth taxes are often criticized for their potential to generate negative economic impacts. For example, many commentators warn that a wealth tax would impose “triple taxation” on investors, since income tax would already have been paid on the taxpayer’s initial income and on subsequent investment earnings (see here). This in turn would reduce incentives to take business risk, to invest, and to finance innovation, thereby damaging growth and economy-wide welfare. This concern is illustrated by a recent study, which estimated that a 2 percent wealth tax on net wealth holdings in excess of $50 million that was used to finance increased transfers to lower-income households would reduce GDP by 2 percent (see here with even larger impacts estimated here). Critics also warn that revenues from a wealth tax would be offset by the impact of weaker economic growth on other tax revenues (see here). However, these estimates depend on assumptions regarding how wealth tax revenues are used, and one study suggests a positive impact on GDP if revenues are used to reduce capital income taxes, since this would improve incentives facing more productive entrepreneurs (see here).

- Wealth taxes raise concerns about capital flight. Some studies have shown that there is a tendency for high-income taxpayers to migrate to low-tax U.S. states (for example, see here). However, the international experience seems to suggest that cross-border migration in response to tax differentials has been small (see here). Moreover, the risk of capital flight in response to a U.S. federal wealth tax would be at least partly mitigated by the fact that U.S. tax liabilities are based on citizenship not physical presence, and that renouncing citizenship triggers an exit tax.

- Taxing wealth presents legal and administrative hurdles. Many scholars have warned that the U.S. constitution prohibits a wealth tax since it disallows ‘direct taxes’ by the federal government with the only exception provided by the 16th Amendment, which gave the federal government the right to tax income (see here). By contrast, the federal estate tax has been interpreted as an excise tax on the transfer of property (see here). Wealth taxes also would involve high levels of administrative complexity. Many of the assets that would be subject to a wealth tax would be difficult to value — e.g., privately held businesses, works of art, etc. — which would increase the cost of administering the tax and the scope for evasion (see here). Others, however, have noted that these hurdles have been addressed in the context of the estate tax.

- Wealth taxes have fallen out of favor internationally. In 1995, there were 12 OECD countries utilizing wealth taxes, but many of these were abolished owing to concern that these were difficult to administer, yielded relatively limited revenues, and encouraged capital flight. Presently, only Colombia, Norway, Spain, and Switzerland still impose these taxes — the tax applies to wealth beyond a threshold, with maximum rates that range from around 1 percent in Switzerland and Norway to as high as 3.5 percent for taxpayers in some Spanish regions (see here and here). Also, some European countries tax selected assets — e.g., Italy applies a tax on foreign real estate holdings, and Belgium applies a tax on the value of securities accounts above a threshold.

What this Means:

On balance, many fiscal policy experts would recommend addressing the shortcomings of the existing tax system rather than risk the administrative and economic costs of a new wealth tax (here and here). On the income tax side, for example, some steps have been taken to reduce the tax preference that applies to unearned income: higher income taxpayers are subject to a 3.8 percent surcharge on investment income at the federal level, which was introduced as part of the Affordable Care Act, and some states have similar surcharges. But for high-income taxpayers, there remains a considerable gap relative to the standard income tax rates, as well as substantial other avenues for income tax avoidance (see here). To help close this gap, recent proposals have been made for a 30 percent flat tax on all income over $1 million, possibly as a replacement for the AMT. Reforms to the estate tax could also be considered, including by lowering the exemption level and by limiting the scope for avoidance through the use of trust vehicles (see here for how these vehicles work). Proposals have also been made to eliminate the step-up in basis that occurs at death, which presently allows taxpayers to pass on assets to their heirs free of any capital gains liability. A more fundamental reform would be to adopt the approach taken by Canada in 1972, which eliminated its estate tax in favor of the requirement that capital gains tax be paid on any unrealized gains upon the taxpayer’s death.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.