Addressing Rising US Debt

Harvard University

The Issue:

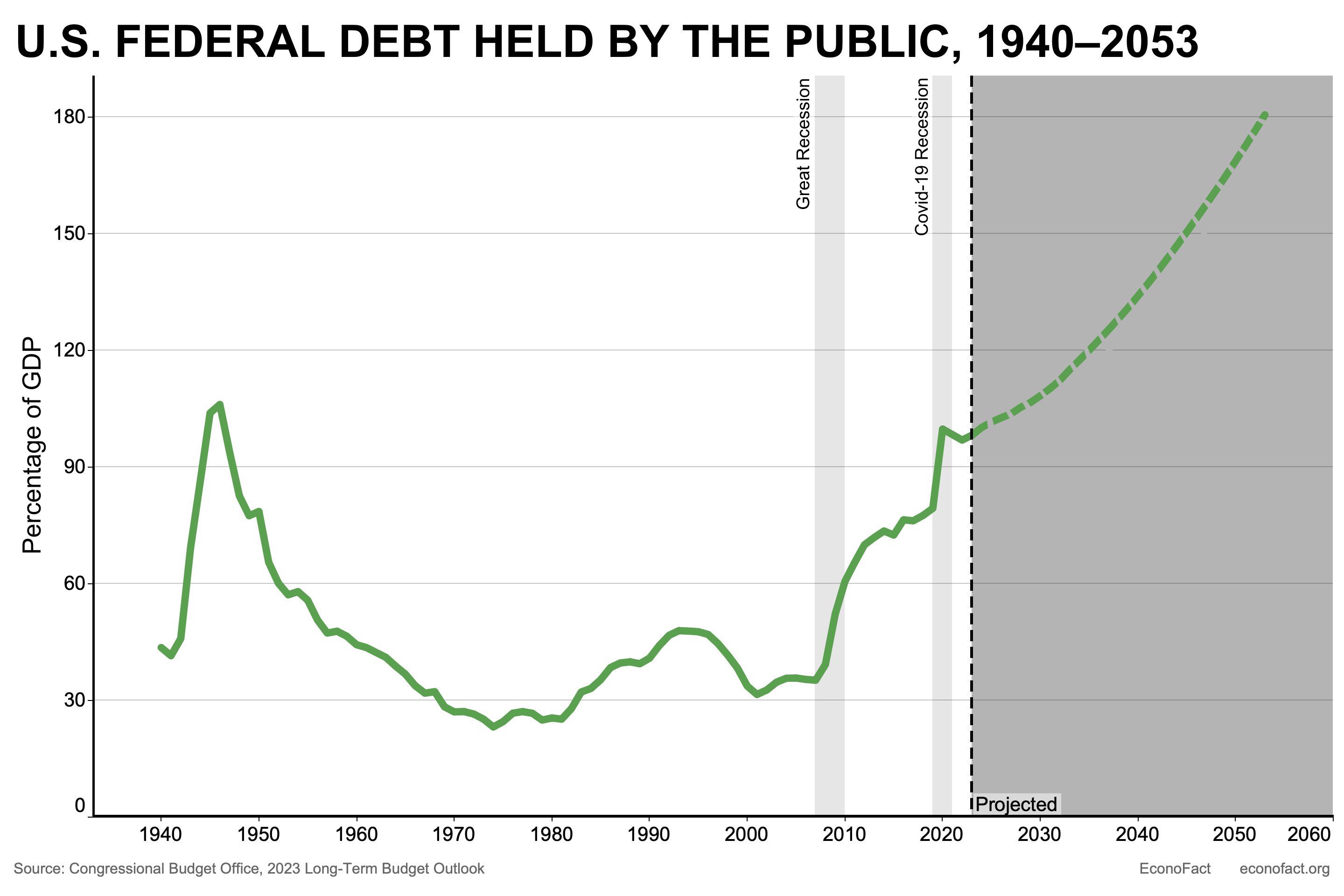

United States Federal Government debt rose sharply after the Great Recession and, at 98% of gross domestic product (GDP) in 2023, is close to its highest level ever. Moreover, under current policy, the federal debt is expected to continue rising over the next three decades to reach levels well above any historical experience — and that holds true even under optimistic assumptions about future economic conditions. In order to keep the federal debt from ballooning to the levels currently predicted, the balance of government spending and revenues needs to be brought into closer alignment in coming years. Changes in policy that substantially narrow the federal deficit going forward have economic and political disadvantages. But, such changes will be needed, as unprecedented levels of government debt impose significant economic costs and risks.

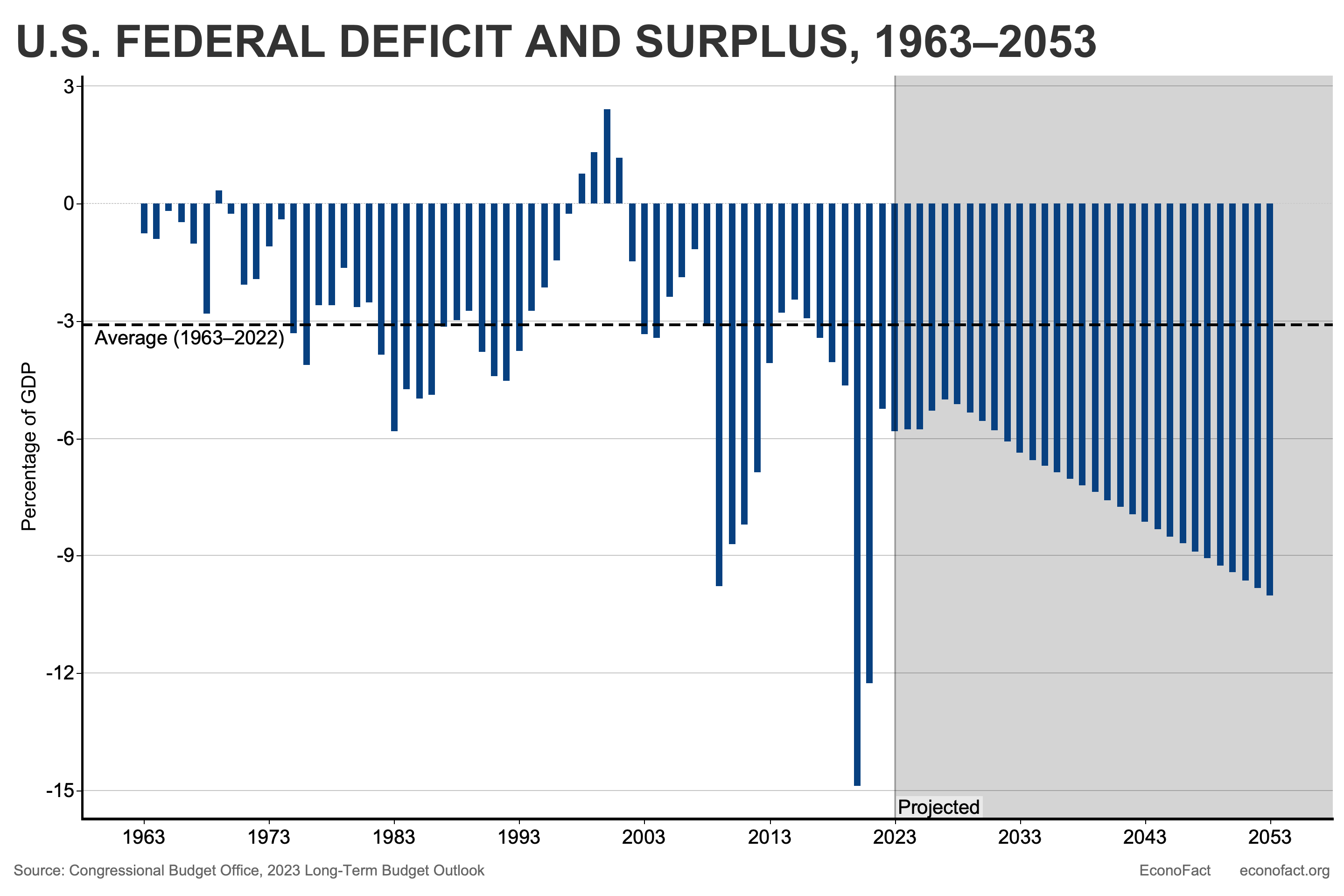

Ongoing large primary deficits, along with an already high level of debt and interest costs, lead to a dramatic snowball effect over time.

The Facts:

- Negative economic shocks and policy changes over the past two decades have shifted current and projected levels of federal debt to higher levels. The United States has seen two significant adverse shocks to economic activity in the 21st century — the deep and prolonged Great Recession that began in 2007 as a result of the global financial crisis, and the sharp economic downturn that followed the onset of the COVID-19 pandemic in early 2020. These episodes led to drops in economic activity and lower tax revenues and, at the same time, to increases in federal spending on recovery programs. In addition to the two major economic shocks, a lasting downshift in government revenues brought about by major changes in tax policy also contributed to higher levels of debt. The changes in tax policy include the extension of tax cuts from early in the first decade of the 2000s and tax cuts enacted in the Tax Cuts and Jobs Act of 2017. If the provisions of the 2017 tax cuts that are scheduled to expire in the next few years were to be extended, the projected path of tax revenues would shift further down — by between $400 billion and $500 billion per year in the late 2020s and early 2030s.

- Behind the projected surge in US federal debt over the next three decades is an expected increase of the federal budget deficit, which is currently high and projected to rise steeply under existing law. A federal budget deficit occurs when federal government spending exceeds its revenues, and the government needs to borrow in order to make up the difference. The federal debt is the accumulation of federal budget deficits over time. It is not uncommon for the US federal government to have a budget deficit, and having deficits that are modest in size is sustainable given growth in the economy. However, the current size of the federal deficit, while smaller than its pandemic highs, is large by historical standards (see chart below). Moreover, the budget deficit is projected to climb much higher over the next three decades, reaching 10% of GDP by 2053.

- The aging US population is a key factor contributing to higher projected government spending. The proportion of the US population aged 65 and older grew from about 12% in the first decade of the 2000s to 17% in 2023, with projections indicating a further increase to 22% by 2050. The growing older population will require significant federal support for both income and health care (see here and here). The Congressional Budget Office (CBO) projects that under current policy, by 2053, Social Security outlays will rise by nearly 1% of GDP and spending on major federal healthcare programs, including Medicare, will rise by 3% of GDP, such that spending on Social Security and federal health care programs will amount to 15% of GDP by 2053. This increase will drive the primary deficit (the deficit excluding interest payments on our existing debt) higher.

- Ongoing large primary deficits, along with an already-high level of debt and interest costs, lead to a dramatic snowball effect over time. A high level of accumulated debt and higher interest rates mean that interest payments on our debt are an increasing part of federal spending. Ongoing large primary deficits generate additional debt that then leads to mounting interest costs, which in turn leads to a considerable additional increase in the total deficit and debt. Under the assumption that government borrowing rates remain at levels somewhat higher than the levels of the late 2010s, the CBO estimates that higher interest costs will push up the overall deficit by an additional 4% of GDP by 2053. Absent policy changes, this dynamic will push the deficit and debt ever higher even in the years beyond CBO’s window.

- These structural challenges mean that even “good luck” with economic developments that would mitigate the debt burden, such as high productivity or low interest rates, will not put the debt on a sustainable path. Estimates of the growth of federal debt over time depend on assumptions about trends in productivity and interest rates, among other factors. Higher-than-expected productivity growth leads to higher GDP growth, which in turn reduces the burden of higher debt. However, even under the most optimistic scenario for productivity growth estimated by the CBO, the federal debt would increase to 137% of GDP by 2053 — well above the historical range. The same is true for the most optimistic interest rate scenario considered by the CBO: an interest rate path that starts 5 basis points lower than baseline in 2023, with the gap then growing by 5 basis points per year, still results in the federal debt held by the public in 2053 increasing to 143 percent of GDP (see here). These analyses underscore that even favorable macroeconomic outcomes are very unlikely to change the conclusion that federal debt is on an unsustainable path.

- The projected path of US federal debt presents significant economic costs and risks. First, increased borrowing by the government crowds out borrowing by households and businesses. This competition for funds drives up interest rates, making it more expensive for individuals and businesses to borrow. As a result, private investment in productive capital decreases, leading to lower future output and national income. Second, elevated borrowing raises the risk of a fiscal crisis. If investors become reluctant to lend money to the government because they fear the debt will not be repaid, government borrowing rates can rise suddenly as prospective lenders demand more compensation to hold government debt. Finally, higher debt also comes with the costs of reduced “fiscal space,” meaning a limited capacity to increase the budget deficit, even temporarily, without endangering the access of a country’s government to financial markets or the sustainability of its debt. A lack of fiscal space constrains a country’s ability to effectively address sudden domestic needs, such as economic crises or pandemics, as well as international threats.

- Many of the policy changes that could help put the debt on a sustainable path have disadvantages, so choices will need to be made carefully. Many of our federal spending programs serve important purposes such as promoting economic growth, fostering economic mobility, mitigating hardship, and protecting national security. Large increases in taxes would not be popular, and some such changes could lead people to work less, save less, invest less, and innovate less.

What this Means:

The challenge posed by high and rising federal debt is significant but manageable as a matter of economics. For example, CBO projects that a combination of reductions in noninterest spending and increases in taxes that reduce the deficit by an average of 2.8% of GDP in coming decades would be expected to keep the ratio of debt to GDP at its current level; alternatively, reducing the deficit by an average of 3.3% of GDP over the 2027 to 2052 period (which would balance the primary deficit) would result in a gradual decline in the debt relative to GDP over time. Policymakers will need to carefully weigh the economic tradeoffs as they make the needed changes to spending and taxes. But the biggest obstacle to addressing high and rising federal debt may be political. Promises not to touch substantial key federal spending programs or to raise taxes are popular, but they cannot all be realized if we are to put the budget on a sustainable path.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.