(How) Will We Pay Back the Federal Debt?

The Fletcher School, Tufts University and The University of California, Berkeley

The Issue:

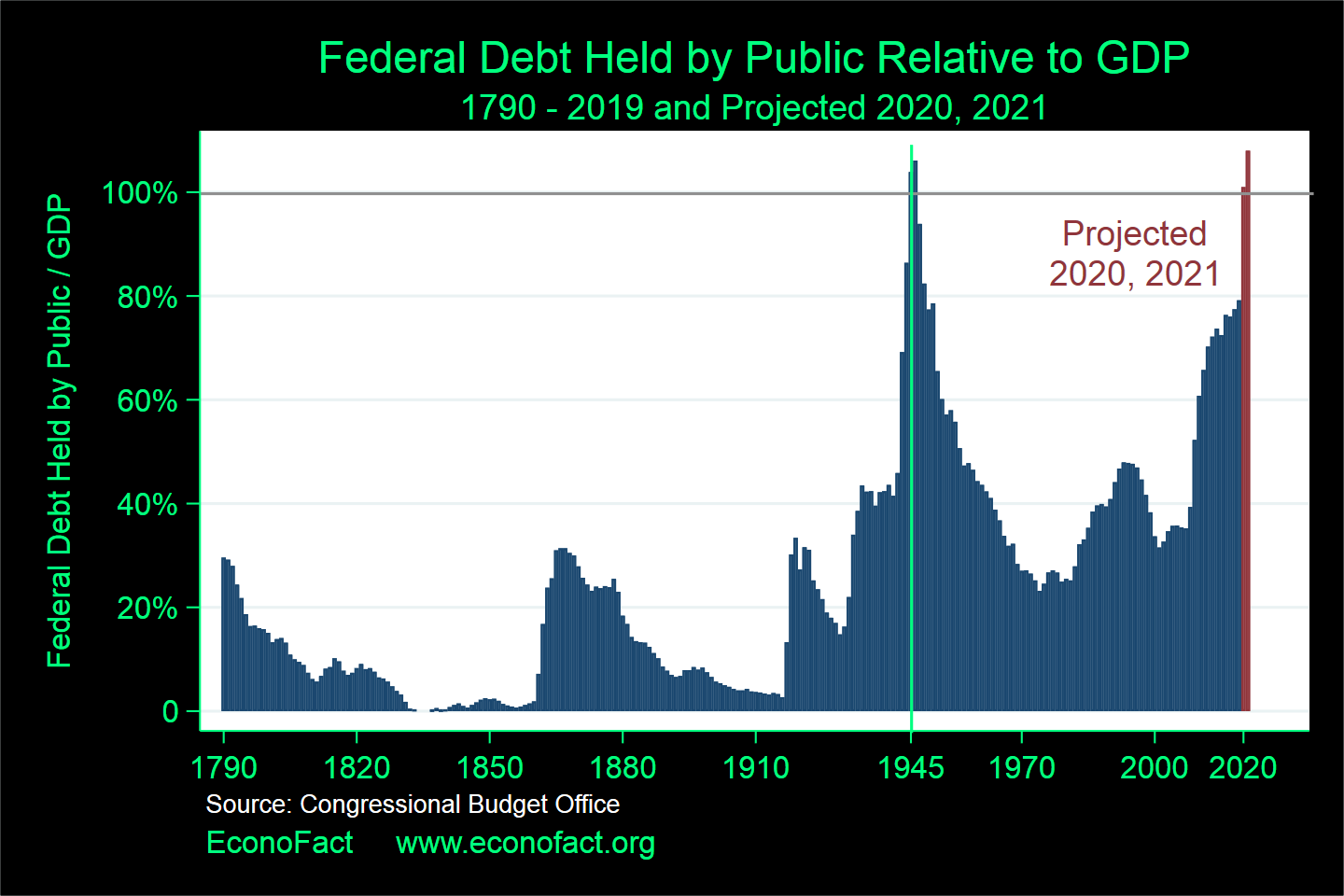

U.S. Federal government debt in the hands of the public amounted to 79 percent of Gross Domestic Product (GDP) at the end of 2019, but it could exceed 100 percent of GDP by the end of this year and rise even higher in 2021 and beyond. Debt levels this high were last seen at the end of World War II, which left the U.S. public debt at 106 percent of GDP. Other advanced economies will similarly exit the current global recession with sharply higher public debts. Will it be important for the United States to reduce its high debt burden rapidly through sharp cuts to government spending or big tax increases?

Low interest rates and a return to economic growth at levels slightly below what was expected before the crisis could make public debt less costly.

The Facts:

- A government issues additional debt when its net revenue does not fully cover its spending and the interest it owes on existing debt, creating a deficit. When the economy suffers a downturn, government borrowing normally rises owing to reduced tax revenue, higher automatic spending on social safety net programs like unemployment insurance, and purposeful spending and tax measures to support the economy. In turn, higher deficits make government debt rise more quickly. Then, as the economy recovers, deficits tend to fall, reducing the pace of increase in government debt. For example, the Federal budget deficit in 2019 was $984 billion (4.6 percent of GDP) while at the end of April this year, facing a precipitous decline in the economy, the Congressional Budget Office projected that the 2020 deficit would be $3.7 trillion, or 18.1 percent of GDP. The CBO also forecast the Federal debt held by the public would be 101 percent of GDP by the end of 2020 – earlier this year, before the economic implications of the coronavirus pandemic became clear, the CBO projected debt would be 80.7 percent of GDP by the end of 2020.

- The level of public debt relative to GDP is a key ratio because the costs of any debt level are less important when the economy is larger. There are two main costs of a higher public debt. First, the government must pay additional interest on its debt, which may require it to raise taxes or cut spending programs. Second, if the economy’s saving flows into government debt, less is available to finance accumulation of possibly more productive capital assets, such as machinery, factories, and intellectual property. For a given level of debt, both of these costs become less important as the economy grows because growth raises both the tax base and the flow of saving. Conversely, a rising ratio of debt to GDP could signal higher taxes and lower future economic growth. Historically, excessive debt-GDP ratios have sometimes led to financial crises in which governments may default on their debts.

- Because the debt-GDP ratio rises when debt rises due to a government deficit and falls when GDP rises, the evolution of debt relative to GDP depends on fiscal policies and growth, but it also depends on interest rates and prior debt. The overall deficit is the sum of government spending net of tax revenues (also called the primary government deficit) and interest paid on prior debt. Thus, the deficit today depends on how much borrowing the government did in the past as well as on the interest it pays on that prior debt. Putting all the components together, the interest rates at which the government has borrowed and its existing debt-GDP ratio are main determinants of the change in its debt-GDP ratio, along with the primary deficit and the pace of nominal GDP growth. (Nominal GDP growth is the sum of the growth in the volume of goods and services produced by the economy, that is, the growth in real GDP, and the increase in the price index of those goods and services, that is, the inflation rate.) The United States government is currently paying historically low interest rates on its borrowing. For example, the CBO forecast in April that the U.S. Treasury would pay 0.7 percent per year on its 10-year borrowing and 0.1 percent per year on its 3-month borrowing through 2021. At the end of 2019, those rates were 1.55 percent and 1.92 percent, respectively.

- Sharp increases in debt-GDP ratios have historically occurred during national emergencies, notably wars, but wartime ratios have tended to fall rapidly thereafter. In the United States, this pattern holds for the Revolutionary War (after the Federal assumption of States’ debts in 1790), the War of 1812, the Civil War, World War I, and World War II. The rise in debt during World War II was especially dramatic, but the subsequent reduction in debt-GDP also was very rapid, with the ratio falling from 106 percent in 1946 to only 51 percent ten years later (and to a low point of 23 percent by 1974). That development owed to lower primary deficits, but also to a rate of nominal GDP growth that persistently outstripped the interest rates the U.S. Treasury had to pay. Between 1946 and 1974, nominal GDP grew at an annual average rate of 6.9 percent per year, whereas the average of long-term Treasury interest rates over this period (which generally exceeded short-term rates) was 4.05 percent.

- The U.S. debt-GDP ratio has risen since the mid-1970s. Over the years 1975 to 2019 as a whole, nominal GDP grew annually by 6.0 percent on average, while the average 10-year Treasury interest rate was higher, at 6.27 percent (short-term interest rates were mostly lower, but the overall cost of debt was closer to nominal GDP growth than before 1975). Debt relative to GDP rose as primary deficits increased. In part, the rise in Treasury borrowing costs over this period reflected financial-market liberalization, which forced the Treasury to compete with private borrowers. The amount of debt in public hands would have increased even more through 2019 had the Federal Reserve not purchased substantial Treasury debt itself starting in 2011 to stimulate the economy following the 2007-09 financial crisis. U.S. interest rates have remained quite low since that crisis and the Federal Reserve slashed them again as a new recession emerged in February 2020 due to COVID-19. However, despite these very low interest rates, the negative impact of the new economic recession on the primary deficit and on nominal GDP growth means the United States will emerge from the current recession with a much higher ratio of debt to GDP.

- Even after recovery, the United States will not necessarily need to implement big tax increases or spending cuts quickly to bring down the high debt-GDP ratio. Most forecasts suggest that nominal interest rates will remain relatively low for a long time, and the Federal Reserve will likely play a role in maintaining those low rates. If inflation returns to its medium-term target of 2 percent per year while annual real GDP growth is 1.5 percent (slightly below many pre-crisis estimates of U.S. potential growth), then nominal GDP growth will be around 3.5 percent per year. If the U.S. Treasury’s average net cost of borrowing remains around 1.5 percent, then even without a primary budget surplus, the net effect of interest payments and growth would be to shrink the debt-GDP ratio at a rate of 2.0 (= 3.5 – 1.5) percent per year. While it persists, this configuration of interest and growth rates would make public debt less costly after the economy recovers.

- A permanently higher debt-GDP ratio after recovery could pose risks, however. The United States is open to foreign capital inflows and the large foreign market for Treasury debt means that higher U.S. public debt by itself would not significantly raise the cost of domestic investment in productive capital. However, other economies are also running big fiscal deficits in the current crisis, and collectively, the United States and other countries could exert upward pressure on government borrowing rates. The OECD has warned that in this year alone, the gross debt-GDP ratios of its member countries (including public debt held by central banks) will rise by 28 percentage points. Another risk is that the United States emerges from the crisis with persistently lower real GDP growth and deflationary pressures. At the other extreme, higher debt would become more problematic if an unexpectedly early resurgence of inflation and inflation expectations forces the Federal Reserve to raise interest rates abruptly, although that possibility seems unlikely anytime soon in view of the muted inflation over the past decade. Finally, the U.S. Treasury faces particularly favorable borrowing rates because of international confidence in U.S. institutions and financial markets, the dollar’s unique international role, and the high liquidity value that investors attach to Treasury securities. Instability in U.S. domestic politics or in its policies toward allies and trading partners could undermine the dollar’s role and raise U.S. government borrowing costs. Any scenario that pushed the interest rate above the GDP growth rate would make the debt-GDP ratio grow explosively in the absence of primary government budget surpluses.

What this Means:

The prospect of even a big increase in the ratio of debt to GDP does not imply that the U.S. government should tighten fiscal policy before the economy fully recovers. Moreover, policymakers should recognize the danger that too little support could leave the economy on a lower GDP growth path and facing stronger deflationary pressures. If this is the outcome, then too little fiscal stimulus will ultimately be more costly than too much. Penny wise would be pound (or dollar) foolish. In addition, the Fed should keep interest rates low to guard against deflation and to ease the Treasury’s interest burden, increasing rates only when there is a clear danger of destabilizing expectations of higher inflation. Indeed, some amount of inflation above the Fed’s 2 percent target (which the Fed has consistently undershot over the past decade) would help reduce the burden of debt. Given projected growth in nominal GDP, we will not see the debt-GDP ratio fall as rapidly as it did in the three decades after World War II. But once the current recession is past, the United States may nonetheless be able to place debt on a declining path without a rapid transition to primary budget surpluses.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.