Risks of Growing Debt vs. Fiscal Stringency in the COVID-19 Crisis

The Brookings Institution and EconoFact

The Issue:

The U.S. government has responded to the severe economic downturn brought on by the coronavirus crisis with several major relief packages at an estimated cost over $2.9 trillion so far. Some political leaders are now questioning further government spending, pointing to sizable long-term fiscal shortfalls. But there are no signs that the economy is poised to rebound any time soon and a continuing deterioration poses high downside risks. As one example, since state and local governments face constraints on borrowing; the fall in revenues that they experience as the economy turns down would force spending cuts that would in turn drive the economy down further. Federal relief is necessary to prevent widespread layoffs and disruptions to vital health and human services that states provide for their residents. What commonalities and distinctions can we draw from other periods when government deficits ballooned in the face of national crises, and what consequences will they have for the current predicament?

Ballooning government debt raises legitimate concerns. But there are also risks associated with pulling back expansionary fiscal efforts too early.

The Facts:

- The economic downturn due to the COVID-19 pandemic and the policy response to this recession have caused historically high government budget deficits. Government deficits tend to rise during an economic downturn because of both less revenue and more social safety net spending; given the size of this economic downturn, and the major relief packages that Congress has enacted, in April 2020 the non-partisan Congressional Budget Office (CBO) deficit projections nearly quadrupled as compared to what was expected at the beginning of this year. In January, the CBO projected an annual deficit of about $1 trillion for 2020, or 5% of total output. The deficit is now expected to be $3.7 trillion for fiscal year 2020, or 17.8 percent of GDP. For comparison, even during the Great Recession of 2008, the deficit never exceeded 10 percent of GDP.

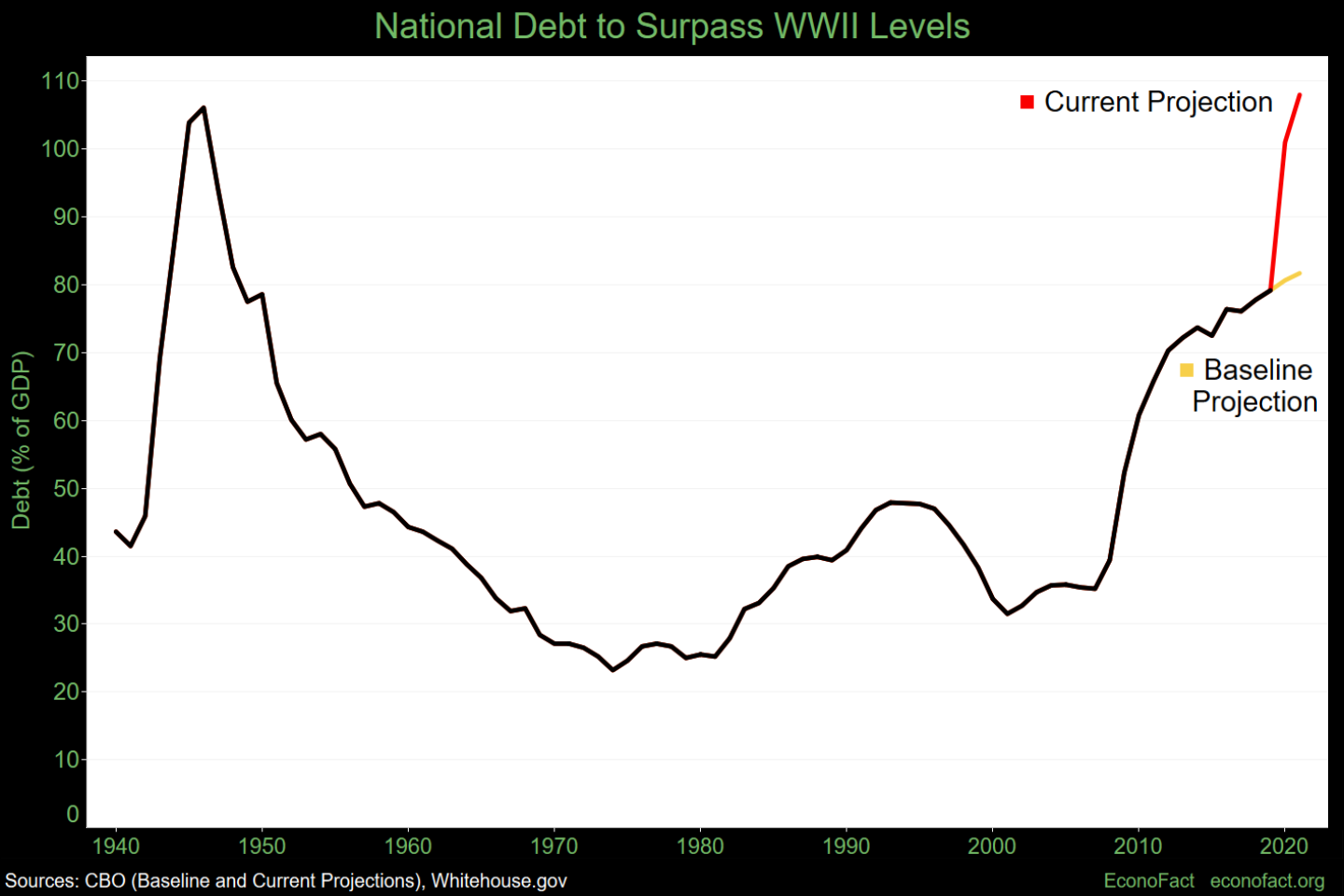

- Public debt is projected to rise to levels not seen since the conclusion of World War II. The public debt is the accumulated deficits, plus interest payments on previous debt. Before the onset of the economic fallout from the pandemic, in January 2020, the CBO projected the total stock of outstanding public to be 80 percent of GDP by the end of 2020 and 82 percent by the end of 2021. Now the CBO expects those figures to be 101 percent and 108 percent. As illustrated in the figure, these numbers represent sizable differences from prior estimates, with values not seen since the end of another national emergency, World War II. Existential threats call for hitherto unimagined levels of public spending. But, in the wake of these costs, worries legitimately arise concerning burgeoning debt. The repayment of high government debt can drain the economy of resources needed for other uses. It could conceivably foment a default crisis in which lenders lose because of either outright default or through the erosion of the debt because of inflationary financing that erodes the value of outstanding debt but that scenario is unlikely for the United States.

- The reduction in the United States debt-to-GDP ratio after World War II offers some insights about the current high debt situation. The immediate post-World War II experience shows that high debt levels need not lead to a crisis. Debt relative to GDP rose from 43.6 percent in 1940 to 106% by 1946. But the aftermath of the war saw no fiscal crisis, and in the 35 years that followed, the ratio of debt to GDP fell to 28%. A significant reason for the post-World War II decline in the debt-to-GDP ratio was the general tendency for interest rates to be below the economic growth rate, so that GDP rose faster than the interest rate on the outstanding debt. Higher economic growth also helps reduce deficits, and contribute to lower debt, through higher tax receipts and less spending on social safety net programs. Because of balanced primary budgets on average between 1947 and 1980 (the primary budget excludes interest payments on debt), low interest rates relative to growth led to a declining ratio of debt to GDP.

- We came into the coronavirus crisis with high budget deficits, given the state of the economy before the pandemic. Unlike the post-World War II period, balanced primary budgets are no longer the norm. Even before the pandemic, the CBO projected the primary deficit to average 2.6 percent of GDP annually from 2021 to 2030. When you take into account interest payments on existing debt as well, the CBO projected in January 2020, an annual deficit of 5 percent of GDP. This is unusual for a time when unemployment was at historic lows. This fiscal situation garnered concerns even before the coronavirus crisis began. GDP growth may be sluggish following the crisis. Even before the crisis, in its January projection, the CBO projection for GDP growth from 2021 to 2030 was a relatively tepid 1.7 percent. The uncertainty of the current situation precludes any forecasts a decade into the future, but the CBO now estimates that inflation-adjusted GDP will be 6.7 percent lower at the end of 2021 than what it projected for that quarter in its January 2020 economic outlook. But interest rates are projected to be even lower, and it is the interest rate minus the GDP growth rate that matters for most budget arithmetic. Under such conditions, the effective cost of government debt is reduced.

- The current situation does not imply, however, that a fiscal retrenchment should be undertaken while the economy is in a dire situation. There are many examples of countries that pulled back expansionary fiscal efforts too early, hindering recoveries and in some cases creating new recessions. For example, towards the latter stages of the Great Depression, the rapid withdrawal of United States government stimulus in 1937 reversed the recovery and led to a downturn until new spending began in 1939. More recently, during the Great Recession, the move to cut back on fiscal stimulus in the wake of the May 2010 G-7 summit led to countries that introduced significant austerity measures doing worse than those that did not. In 2013, the IMF issued a paper co-authored by its then Chief Economist, Olivier Blanchard, that said its earlier advice of relatively early fiscal retrenchment was incorrect.

What this Means:

Despite concerns about the long-term fiscal outlook, the government needs to continue to provide support to help distressed sectors survive this crisis. Responding too strongly to the present crisis carries small risks and relatively low costs compared with a response that falls short. The recovery from the economic crisis caused by the coronavirus pandemic, as well as the important financial lifeline that fiscal policy can play, would be derailed by fiscal stringency; but ultimately the economic damage cannot be repaired until the underlying disease is under some measure of control. Like a course of antibiotics, an economic relief package is most efficacious when administered to completion.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.