The Other 95%: Taxes on Pass-Through Businesses

Brookings Institution

The Issue:

Policy debates about business taxes usually focus on corporations. But most businesses and most business income come from so-called “pass-through” entities: businesses that are not organized as traditional corporations. Both the 1986 tax reforms and the more recent 2017 Tax Cuts and Jobs Act provided subsidies to pass-through businesses.

Public policy must address the fairness, efficiency, compliance, and revenue concerns raised by the taxation of of pass-through businesses.

The Facts:

- Pass-through entities are remarkably diverse and account for a large majority of all businesses. They include sole proprietorships (owned by a single person) as well as partnerships (owned by two or more people), which can be structured as limited liability corporations (LLCs). Another type of pass-through business is an S-Corporation, which has restrictions on the number of owners and, unlike a partnership, must allocate net income proportional to each owner’s share. In all these types of businesses, profits are not subject to an entity-level tax but are instead “passed through” to owners and taxed as owner’s income under the personal income tax. In contrast, the profits of traditional (“C”) corporations face tax at the corporate level and then shareholders pay taxes on dividends and capital gains.

- While most pass-through businesses are owned by middle-income households, the overwhelming majority of pass-through business income goes to the top 1% of the income distribution. Most sole proprietorships are small businesses, typically owned by middle-income households, and they generally account for less than half of the owner’s income. However, many large businesses, which generate much more income, are also classified as pass-through businesses. Over 98% of business income earned by partnerships and S-Corporations goes to households in the top fifth of the income distribution, with the top 1% earning 71% of business income and the top 0.1% earning one-third. The rise of pass-through income accounts for 40 percent of the 10-percentage point increase (from 10 percent to 20 percent) of the share of income going to the top 1% between 1980 and 2013.

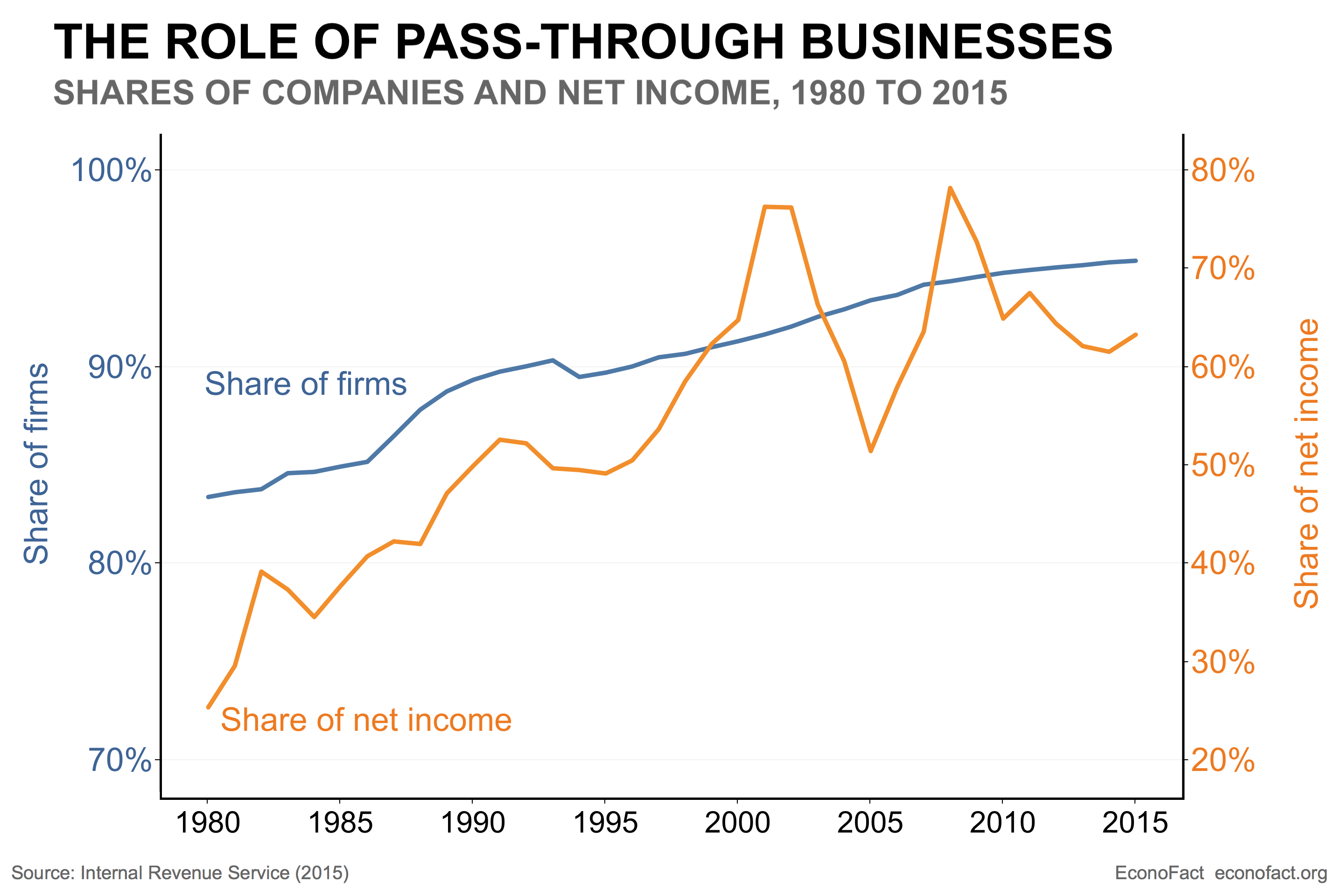

- The proportion of businesses that are pass-throughs rather than corporations has grown enormously since 1980. Pass-through businesses represented 83 percent of businesses and 25 percent of business income in 1980. In 2015, these values had grown to 95 percent of all businesses and 63 percent of all business income (see chart). Much of the growth in pass-through businesses can be attributed to more favorable tax treatment of pass-throughs relative to corporations, liberalization of rules regarding the ownership of S-corporations, and expansion of limited liability to non-corporate businesses under state laws. For example, the 1986 tax reforms made pass-through businesses more attractive by significantly reducing the top individual income tax rate relative to the top corporate tax rate. The shift in the composition of businesses toward pass-throughs has reduced government revenues. Even before the 2017 tax act, estimates suggested that the shift toward pass-throughs had reduced federal revenues by $100 billion per year.

- Tax avoidance and tax evasion also contribute to the loss of government revenues when businesses switch from a corporate organization to a pass-through organization. The ownership structure in partnerships can be opaque, making it difficult to trace how business income is allocated in this particular type of pass-through business. A study by U.S. Treasury economists suggests substantial tax evasion occurs in partnerships: 20 percent of partnership income could not be traced in tax return data and another 15 percent was earned by groups of partnerships that collectively owned each other, an arrangement that suggests efforts at tax avoidance or evasion. Tax evasion is illegal and can be either deliberate, as when not reporting income, or inadvertent, as when making mistakes in filing tax returns. (Tax evasion is distinct from tax avoidance, which involves reducing tax liability through legal means, like saving in tax-preferred accounts). An IRS analysis indicates the evasion rate on partnership income is about 11 percent and the evasion rate on sole proprietor income is 56 percent — as compared to just 1 percent on wage income.

- The 2017 Tax Cuts and Jobs Act (TCJA) included a provision that reduced the effective tax rate on pass-through businesses and introduced unequal treatment within the set of pass-through firms. The so-called 199A (named for the relevant IRS code section) or “qualified business income” deduction allows up to 20 percent deduction for certain pass-through income through 2025, after which the measure is scheduled to expire. This effectively reduces the top marginal tax rate on qualifying pass-through income from the top ordinary rate of 37 percent to 29.6. The 199A pass-through deduction violates the common tax policy goal of horizontal equity because businesses with similar incomes do not pay the same tax, and a person with a given amount of wage income will likely pay more tax than a person with the same amount of business income. The deduction also makes business taxation less progressive: It gives very large tax cuts to the very highest income taxpayers and little to middle- or low-income taxpayers. JCT (2018) found that 44% of the direct tax benefits in 2018 (rising to 52% by 2024) would go to taxpayers with incomes greater than $1,000,000 per year, while only 7% of benefits would go to those making less than $100,000 per year. Similarly, a Tax Policy Center study found that 55% of the direct tax benefits in 2019 would go to households in the top 1% of the income distribution and more than 27% would go to the top 0.1%, while only 10% of the benefits would accrue to the bottom 80% of earners. While some argued that the deduction would help to stimulate investment and lead to higher wages, there is little evidence that this deduction has influenced economic activity to date. One recent analysis of the deduction found no evidence of changes in real economic activity as measured by physical investment, wages to non-owners, or employment of non-owners. At the aggregate level, rates of business formation did not rise after TCJA.

What this Means:

Ideally business taxes should be designed to avoid influencing the value-neutral choices that companies make, like how to finance investment. But businesses inevitably respond to incentives created by tax policy. Pass-through businesses, ranging from tiny “mom and pop” operations to world-wide partnerships, are a vital part of the economy, representing a larger share of income than corporations do. Public policy must address the fairness, efficiency, compliance, and revenue concerns raised by taxation of these companies.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.