Tracking the AI Boom: Some Lessons From Economic History

EconoFact

The Issue:

Recent years have witnessed an extraordinary boom in Artificial Intelligence (AI) based on a widespread perception that AI is a truly transformative technology that will drive economic growth for many years, comparable to the adoption of the railroad, electric power, the automotive, the personal computer, and the internet over the past two centuries. But there are also many skeptical voices that warn that this boom is greatly overdone, that the economic gains will be slow to come, and that AI is an inflating bubble that could burst with dangerous consequences for the U.S. economy. Previous cycles of dramatic investment in technological change can provide lessons for understanding different ways in which AI might indeed be a bubble, what would be the consequences of different forms of a bubble, and what to look for to judge which path AI is actually on.

Prior waves of technological change have experienced busts along the way, even if innovations ultimately became foundational technologies.

The Facts:

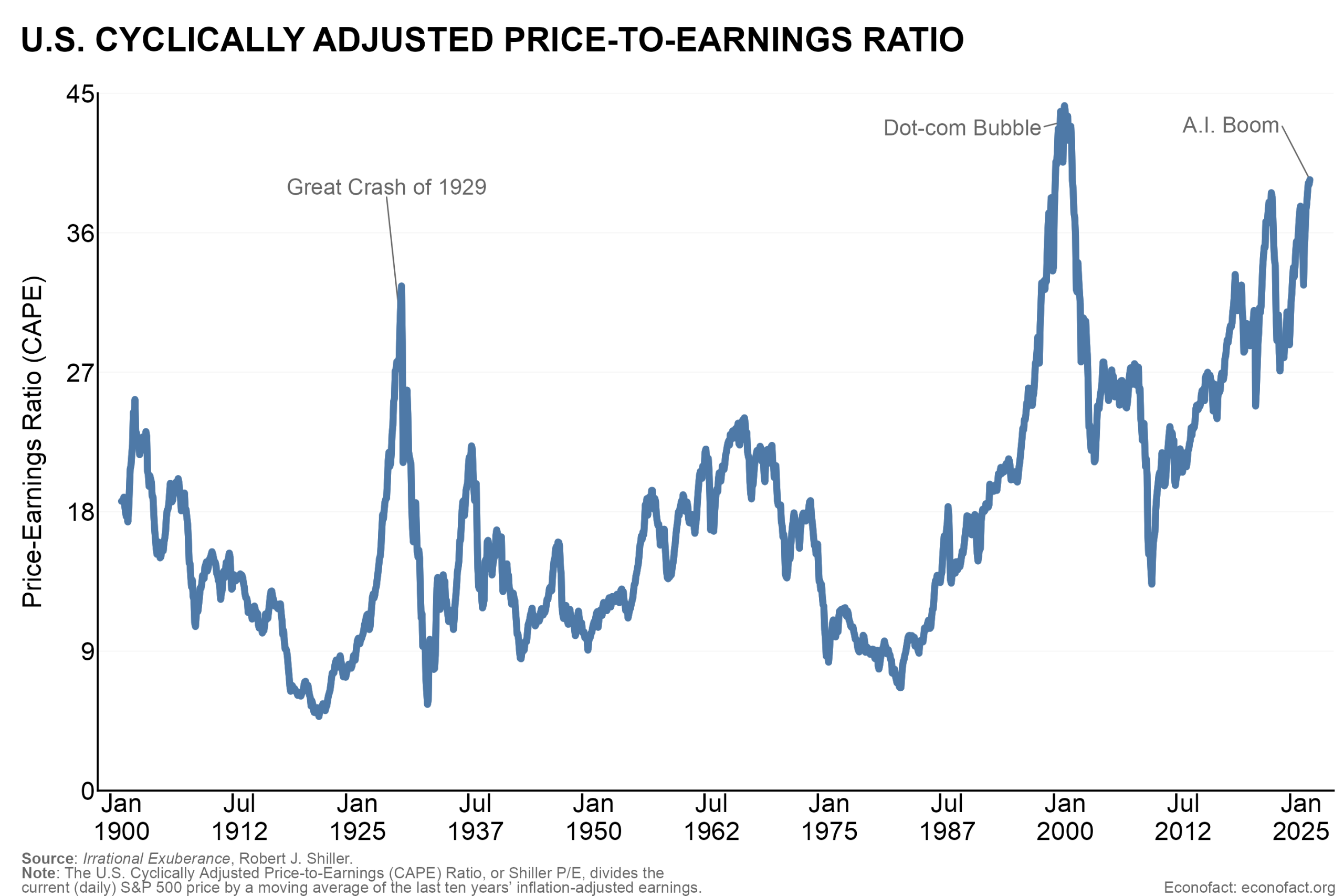

- The boom in AI has many dimensions. Artificial Intelligence has been a long-term aspiration for computer science. After years of slow progress, AI’s use has exploded since November 2022 with the introduction of user-friendly interactive chatbots developed from sophisticated statistical analysis of large data sets. ChatGPT and other AI chatbots have been adopted both by individuals and firms at a pace well-exceeding previous waves of computing innovation. An extraordinary boom in AI-related hardware (data centers, chip making factories) and software (new AI models and tools) in the United States has accounted for a significant share of recent US economic growth — around 1% of GDP growth in 2025 by some estimates. The stock market prices for the top seven tech firms have risen far in excess of the rest of the market, driving the widely-used Schiller PE ratio, which provides a measure of whether a stock is undervalued or overvalued, close to its previous peak at the height of the dot-com bubble (see chart). And, there has been a mind-boggling explosion in compensation packages for top AI innovators.

- The challenge is to anticipate to what extent this AI boom will be justified by continued extraordinary technological gains matched by economic returns. Notwithstanding the amazing recent progress, there remains broad uncertainty regarding the path of continued AI innovation, as well as of its potential applications and their economic impact. It has to be recognized that AI is already being applied across a wide variety of fields. For individual consumers it offers powerful but user-friendly software, e.g. for search, for image creation, for communication, and for learning. For businesses, it provides a tool to quickly perform many mid-level white-collar tasks including coding, data analysis and report writing. AI tools are advancing with new iterations that address previous flaws like “AI hallucinations” (where the chatbot makes up an incorrect answer) and introduce higher-level reasoning capabilities. As AI continues to evolve, it could potentially be used to transform many areas of economic activity, for example to support self-driving robocars, personalized education, the development of new pharmaceuticals and medical diagnostic tools tailored to individual health needs — or in ways that are hard to anticipate. But there are diverse views about the extent to which AI’s capacity will continue to race ahead or whether it could instead hit a technology-limited plateau.

- One of the key lessons from economic history is that prior waves of enthusiastic technological innovation have seldom gone smoothly and many have experienced busts along the way, even if ultimately innovations have become foundational technologies. These booms and busts often take the form of a bubble. The classic form of a bubble occurs in financial markets where investors’ hopes for asset price appreciation pull in additional funding, driving up prices well above the true underlying value of the asset until eventually sentiment reverses, new funding dries up, and prices collapse. The “dotcom bubble” of the late 1990s is a good example of excitement about a new technology — the internet — being accompanied by such a financial bubble, culminating in a collapse of equity prices. There can also be a bubble in the real economy, where a new technology leads to a surge in infrastructure investment from entrepreneurs trying to be the first to build network capacity and capture markets, followed by a bust when it’s realized that the total build in infrastructure far exceeds needs — at least for the immediate future. Railroad building in the US in the 19th century provides a well-known example. Railroad companies borrowed heavily to build new lines. When there were more railroad bonds for sale than investors wanted to purchase, many railroads went bankrupt, taking down one of the biggest banks in New York City, and the financial panic of 1873 followed. Note that financial bubbles and real economy boom and bust cycles typically go hand-in-hand, as shown by the dot-com and railroad experiences.

- Previous episodes of technology-driven investment booms suggest different scenarios for how the AI boom could play out over the next few years. Not infrequently, technology booms have ended with dashed expectations in which, though the technology brought substantial returns in certain sectors, it had a limited impact on aggregate productivity or profitability at least in the short-to-medium term (although the longer-term returns were eventually sizeable). This was the pattern with earlier waves of innovation like railroads and the internet. Often, it has taken more time than expected to develop new skills and products to take full advantage of the emerging new technology. Sometimes, the new technology is largely superseded by a further wave of innovation —canals built in the first half of the 19th century were made redundant by the railroads. (Such a fate could also befall the current Large Language Model-based AI technology.) Either way, the end result has been a broad bust with a collapse in investment to more normal levels, sharp reversals in stock market prices, and widespread financial distress in companies that overinvested.

- Alternatively, a technology-led boom can end in a profitability bust, in which investors find it hard to capture genuine economic gains in company profits adequate to remunerate the extraordinary levels of investment. When the dot-com bubble burst, many of the companies that went bankrupt had high valuations but little to show in terms of profits. After the dot-com crash, successful software firms found ways to effectively monetize large investments in the 2000s. For example, Google and Facebook were able to do so through sophisticated advertising algorithms developed for their search and social network applications, while Microsoft continued to prosper through a fee-based structure (subscription or pay to play) for use of business productivity software. So far in the current AI cycle, while the manufacturers of advanced chips like Nvidia have been able to achieve sky-rocketing profits, the income from the use of AI software has remained quite limited. At best, future income streams would seem likely constrained except for a few successful companies that capture the lion’s share of the market. And both chipmakers and software designers could be vulnerable if AI becomes largely a standardized commodity or if an alternative, even better technology emerges. In this scenario, there would be retrenchment and consolidation in the AI software and infrastructure industries, but the broader economy could continue to prosper from AI applications. The stock market would see a rebalancing with tech firms producing AI software and infrastructure underperforming and companies that apply AI tools to improve products and increase profitability gaining.

- Even with hoped-for gains being achieved in productivity and profitability in the aggregate, there could be a shakeout in the midst of a sustained boom. As befell previous software market leaders like Netscape and MySpace, in the AI sector itself there might be a few big winners and many losers given network effects and economies of scale. Even ChatGPT, which recently declared “code red” over threats to its AI lead, could fall by the wayside. Similarly, many firms in AI-using industries could fall behind others that are more successful in applying newly available AI tools or be absorbed by the leaders in AI adoption, a form familiar from past cycles. And workers more generally will need to adapt to the fact that many companies will no longer need so many employees doing routine tasks, like basic coding or report-writing tasks, either by upgrading their AI skills or by looking for alternative activities less easily substituted by AI, such as hands-on creative and manual skills.

- While each cycle is different, and it’s important to recognize specific features of the current experience, economic history does suggest some particular signals that would be helpful to watch for as the current AI boom continues to evolve in order to anticipate how it may end up. Are adoption of AI tools and the efficiency of AI in work tasks continuing to grow dramatically? So far, the user base continues to grow rapidly and the efficiency of new models continues to rise exponentially. Will this continue as Moore’s Law has for fifty years? If not, the chances of a “dashed expectations” scenario rise, constraining further adoption and profit streams in the AI sector. In a similar vein, are business users of AI tools achieving major improvements in productivity and amazing new innovations to justify major AI expenditures? Studies by MIT Media Lab and McKinsey suggest that so far most businesses are not yet realizing meaningful returns from their investments, but nevertheless these efforts race ahead. Is market pricing of “hot stocks” being driven primarily by hopes for further short-term price momentum beyond any reasonable expectations of future earnings? Such behavior would inevitably be reversed, most likely leading to a market crash such as occurred during the “dot-com bubble”.

What this Means:

There is no question that recent technological advances in AI have been hugely consequential and are providing major support to the US economy and stock market. But learning from the long history of past waves of technological innovation, it’s important to realize that periods of rapid technological change seldom go smoothly. Given the pace of change and the uncertainty and complexity of innovation, it’s very hard to distinguish between reasonable expectations and the hype to anticipate how AI technology will develop in the years ahead and to assess the extent of risks of various types of bubble outcomes. Recent developments certainly have bubble-like features, but will this time be different? Various paths ahead seem quite plausible: it remains to be determined whether we are in the early stages of a golden era of growth fueled by AI applications (albeit with inevitable creative destruction affecting those unable to adapt to the new world); at the other extreme, an AI bust in which great expectations are dashed and the economy suffers a serious recession as the AI boom’s excesses are unwound; or a middling scenario in which AI does bring sustained high returns for users, but where the AI sector itself goes through a major downsizing and consolidation.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.