Rising U.S. Interest Rates and Emerging Market Distress

The World Bank

The Issue:

The recent swift tightening of monetary policy in advanced economies, especially the United States, in response to high inflation poses significant challenges to emerging market and developing economies. The international spillovers associated with rapidly rising U.S. interest rates can heighten the likelihood of financial distress in these economies; however, this likelihood depends upon the reasons why U.S. interest rates rise. Interest rate increases are likely to be particularly injurious when they are driven by market perceptions of more hawkish Federal Reserve policy. They are also more damaging in economies with pre-existing vulnerabilities. New research from the World Bank addresses these issues, analyzing the reasons for recent increases in U.S. interest rates, the effects on financial conditions in emerging and developing economies of these increases, and sources of the differences in the risk across these economies.

Increases in U.S. interest rates that reflect perceptions of more hawkish Fed policy have especially adverse spillovers on emerging and developing economies with greater economic vulnerabilities.

The Facts:

- U.S. interest rates can rise due to different reasons. The World Bank study identifies three potential drivers for increases in U.S. Treasury bond yields: (1) “inflation shocks,” which reflect expectations of rising U.S. inflation, which encourage investors to demand higher interest rates to compensate them for inflation’s erosion of the value of future dollar payments; (2) “reaction shocks,” which reflect investors’ assessments that the Federal Reserve has shifted to a more aggressive monetary policy, implying the prospect of higher interest rates in the future that results in higher current interest rates; and (3) “real shocks,” prompted by improved prospects for U.S. economic activity which raises the demand for funding and, therefore, raises interest rates which represent the cost of borrowing. This study attributes the lion’s share of the recent steep and rapid rise in U.S. interest rates (the Federal Reserve raised the policy interest rate by 5 percentage points in 10 consecutive Open Market Committee meetings) to reaction shocks. Indeed, reaction shocks accounted for almost 60 percent of all shocks from early 2022 to May 2023. In contrast, inflation and real shocks accounted for about 20 percent each.

- There are a range of reasons that higher U.S. interest rates adversely affect emerging market economies. One way is by making assets offered in emerging market economies less attractive, leading to lower financial flows to these countries. This increases the cost of borrowing in emerging markets, depressing demand. The falloff in capital flows also puts pressure on countries’ exchange rates to lose value against the dollar. This raises the cost of imports whose prices are denominated in dollars (as is the case with commodities like oil, foods, and raw materials, along with many manufactured goods) putting upward pressure on inflation. To counter these effects, emerging market central banks may raise their own domestic policy interest rates to continue to attract foreign funding and counter inflation, which depresses domestic demand. Higher interest rates, along with a depreciation against the dollar, make it more expensive to pay back borrowing denominated in dollars.

- Increases in U.S. interest rates associated with higher inflation expectations or, especially, the perception that the Fed has shifted toward a more aggressive policy are likely to lead to more adverse spillovers on emerging and developing economies than when higher interest rates are the result of improved prospects for the U.S. economy. When U.S. interest rates rise because of a reaction shock or an inflation shock there is not an accompanying increase in U.S. income (which would draw in more exports from emerging and developing economies) as opposed to an increase in U.S. interest rates due to a real shock that raises prospects for U.S. growth. Using historical data, the World Bank study estimated that, for the average emerging market/developing economy, the probability of facing a financial crisis in a given year from 1985 to 2018 was 3½ percent. But the study estimated that the probability of a crisis almost doubled, to about 6½ percent, when the 2-year yields in the U.S. increased by 25 basis points because of market expectations of a shift toward more aggressive Fed policy. By comparison, the impact of an increase in interest rates due to improved prospects for the U.S. economy did not materially affect the likelihood of currency crises in emerging markets and developing economies.

- The extent to which particular emerging market and developing countries are affected by rising U.S. interest rates differs with existing conditions in these countries. Countries that have higher levels of sovereign debt are more vulnerable to adverse outcomes arising from an increase in U.S. interest rates because the cost of their debt burden is larger with higher interest rates and a weaker currency. Countries that pay a higher premium for borrowing, as reflected by a higher interest rate spread between their sovereign debt and safer assets, or by a lower credit rating, are also more vulnerable because of a proportionally bigger reduction in willingness to hold risky assets. Initial macroeconomic conditions matter as well. Countries with larger budget deficits have less fiscal space to offset downturns and are therefore more vulnerable. Countries with larger trade deficits are at greater risk of larger currency depreciations. There are greater vulnerabilities in countries that have less developed (and therefore more unstable) financial markets, as well as lower levels of political stability and less robust institutions. World Bank research estimates suggest that for any given increase in U.S. interest rates driven by reaction shocks, more vulnerable economies tend to experience local-currency yield increases that are almost twice as large as those in less-vulnerable economies. The estimated likelihood of financial crises is also higher in these more vulnerable economies.

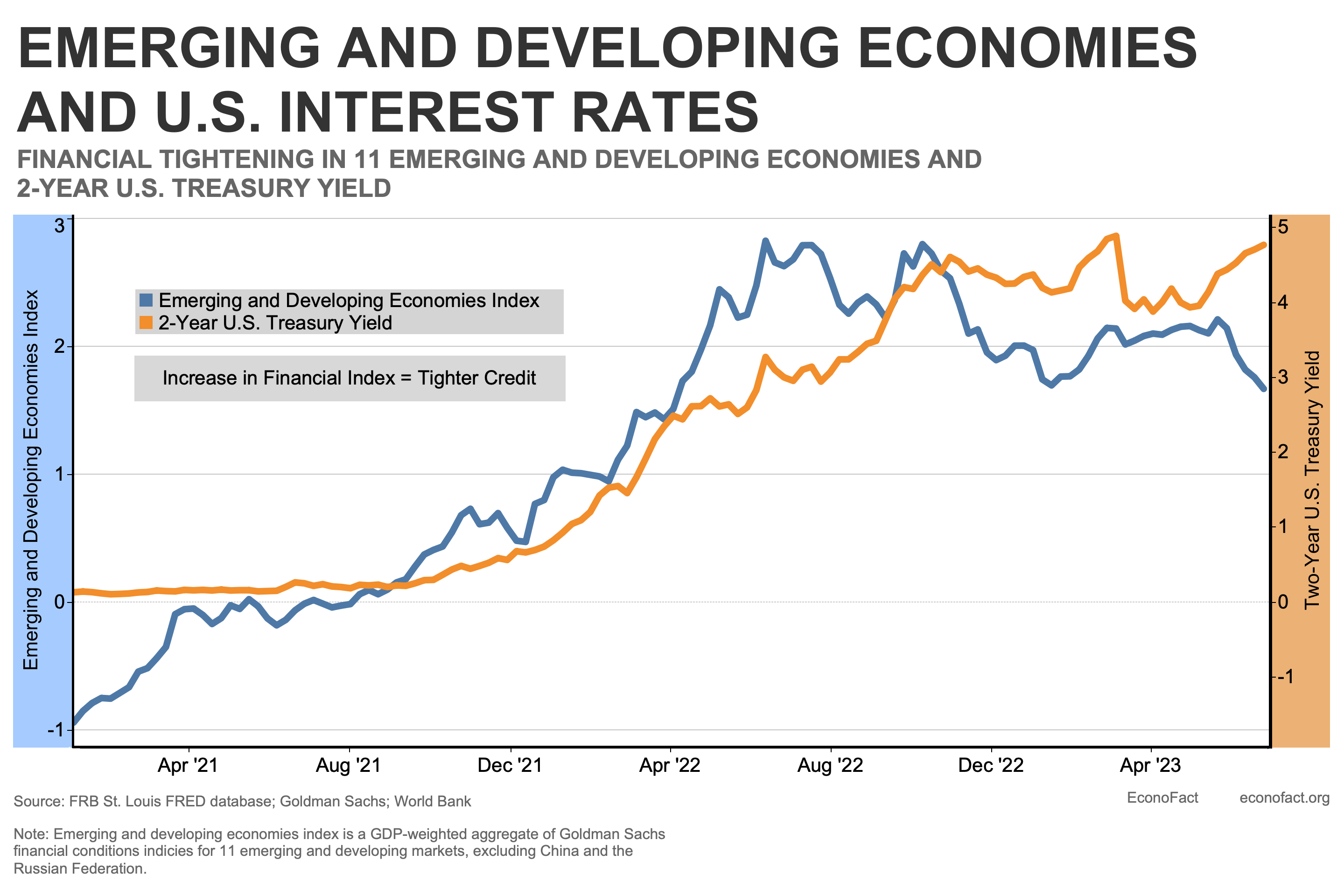

- These findings are consistent with developments in the financial conditions in emerging and developing economies in the past year and a half. Since the end of 2021, there has been an increase in the share of emerging markets and developing economies with sovereign spreads exceeding 10 percentage points (that is, government bond yields that are 10 percentage points or greater than the bond yields of countries with AAA ratings): This share jumped from 13 percent of economies in December 2021 to 26 percent of economies in May 2023. The interest rate facing corporate borrowers in an emerging market or developing economy rises with increases in that country’s sovereign interest rate. The financial conditions in these economies have become more challenging with rising U.S. interest rates: emerging market financing conditions rose rapidly in tandem with the yield on U.S. two-year Treasury bonds amid the rapid tightening of monetary policy that began in March 2022 (see chart). (The index in the chart represents the level of a range of financial variables—including policy rates, bond yields, risk spreads, equity prices and exchange rates—for a sample of 11 large EMDEs with relatively deep financial markets). High sovereign interest rates indicate difficulty in borrowing in international markets and an increase in the risk of default. But the risk of default depends upon existing conditions. Financial conditions in emerging markets with strong fundamentals and adept macroeconomic management generally remained stable. Conversely, those economies with weaker fundamentals have experienced more pronounced financial downdrafts. Countries with shorter records of borrowing in international markets and countries whose borrowing is below investment grade with weak monetary and fiscal policy frameworks have been particularly exposed. Indeed, from January 2022 to May2023, sovereign risk spreads in emerging and developing economies with weaker credit ratings (Caa and below) rose by more than 12 percentage points; in contrast, spreads in emerging and developing economies with stronger credit ratings (Baa and above) increased by only 0.2 percentage points (see figure 3.6 here).

What this Means:

The recent rapid rise in interest rates in the United States generates potential risks to emerging and developing economies, particularly since a substantial part of the sharp increases in U.S. interest rates since early 2022 has been driven by market perceptions that the Federal Reserve has pivoted toward a more hawkish stance to rein in inflation. Although the policy mandate in the United States does not include consideration of spillover effects, emerging market and developing economies could nonetheless benefit if U.S. monetary policy avoided abrupt changes, and abrupt perceptions of coming changes, to reduce volatility. Emerging and developing economy central banks may need to tighten their own policies to moderate the risks of disruptive capital outflows, currency depreciation, and resultant increases in inflation, but this comes with the potential of generating a recession, and taking the proper policy stance can be difficult. A longer-term strategy to mute disruptive spillover effects is to reduce fundamental vulnerabilities, but these changes may be challenging to implement.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.