Will Steel Tariffs put U.S. Jobs at Risk?

Harvard University and University of California, Davis

The Issue:

The U.S. Department of Commerce announced recommendations on February 16, 2018 to impose heavy tariffs or quotas on foreign producers of steel. The proposed tariffs are taxes on imported steel. The quotas would put caps on the volume of imported steel. Either type of measure would raise the price of steel in the United States. This could help domestic steel producers, but it would harm U. S. manufacturing industries that use steel and products made of steel as inputs. Tariffs and quotas are often presented as trading off domestic producer gains against consumer losses, but because steel is an input into so many other products, the measures more likely will trade off jobs saved in steel industry against job losses in other manufacturing industries. The losses could be substantial because the number of jobs in U.S. industries that use steel or inputs made of steel outnumber the number of jobs involved in the production of steel by roughly 80 to 1. For this reason, these trade recommendations raise concerns among many manufacturing companies.Jobs in U.S. industries that use steel or inputs made of steel outnumber those involved in the production of steel by roughly 80 to 1.

The Facts:

- Tariffs and quotas may stimulate greater domestic production by raising the price of steel in the United States. The United States relied on imports for 18 percent of its steel needs in 2017, according to data from the United States Geological Survey. The Commerce Department has recommended that the Administration adopt one of three new protectionist measures on steel: (1) a global tariff of 24 percent on all steel imports, (2) a 53 percent tariff on U.S. steel imports from twelve developing and transitional economies and quotas for all other nations capped at 2017 levels, or (3) a quota on steel imports from all countries capped at 63 percent of what those countries exported to the United States in 2017. Any of the three Commerce Department measures would raise the domestic price of steel. For example, when President George W. Bush imposed safeguard tariffs of 8 to 30 percent on certain steel products in 2002-2003, the domestic price for key steel products increased to a roughly similar degree (see Figures 2-2 to 2-13 in this report).

- Greater demand for domestic steel may have a muted effect on employment in steel production because of technological innovation. Technological progress has played an important role in displacing workers in steel production, just as it has in many areas of manufacturing. A recent study (also summarized here) shows that while the U.S. steel industry shed about three-quarters of its jobs between 1962 and 2005, output per worker quintupled—largely due to a new production technology called minimills. The authors observe that this innovation has made “the steel sector one of the fastest growing of the manufacturing industries over the last three decades, behind only the computer software and equipment industries (p.132),” at the same time steel employment has declined. Indeed, even between 2006 and 2016, employment in steel production fell more than 10 percent, to 140,000 workers, while output per worker increased more than 20 percent, according to data from the U.S. Bureau of Labor Statistics. Thus, even if trade protection leads to increased domestic production, increases in employment may be far less than many hope.

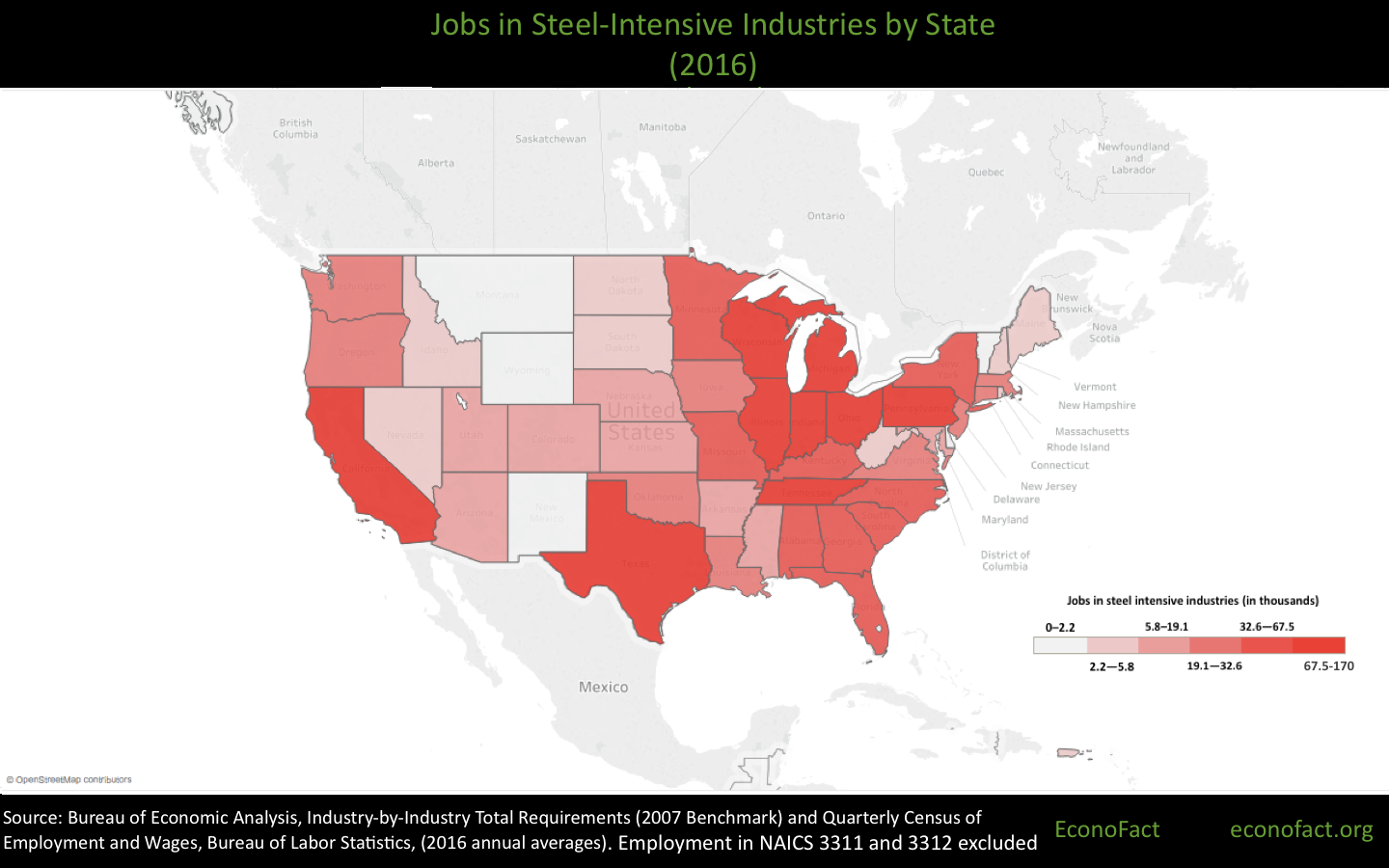

- Higher steel prices could adversely affect other U.S. manufacturing industries that depend on steel as an input to production. About 2 million jobs are in industries that use steel intensively, where “intensively” means that steel inputs represent 5 percent or more of the industry’s total (input) requirements. This criterion includes both the industry’s direct use of steel and its indirect use through inputs made of steel, like machinery and equipment. Steel-intensive U.S. industries include manufacturers of auto parts and motorcycles; household appliances, including large appliances like washing machines; farm machinery; machinery used in mining, oil extraction, and construction; batteries; armored military vehicles; and hardware. In the map, we show average 2016 quarterly employment in these industries by state. Jobs in steel-intensive industries are located in nearly every state in the country, but particularly concentrated in California, Texas, the Rust Belt states, and the Southeastern states

- Industries that use steel most intensively may be at risk of job losses and plant relocations if the United States imposes high tariffs on steel for a prolonged period. The higher price of steel in the United States cannot always be easily passed on to consumers because many steel-using manufacturing industries both export and face import competition. If they pass on steel cost increases in their final goods prices, companies in these industries risk losing market share, both at home and abroad, to suppliers who produce outside the United States where steel would not be subject to the U.S. trade restrictions. This was the case under the Bush Administration’s steel tariffs. The independent U.S. International Trade Commission reported that fewer than 1 in 5 surveyed steel-using firms were able to pass on any portion of the increase in their production costs after the Bush safeguard tariffs went into force (see page 2-14). Estimates of job losses in steel-using industries as a consequence of the safeguard tariffs imposed in the early 2000s are few but range from 26,000 to 200,000 jobs. It is difficult to know how many steel-producing jobs were saved, but a Peterson Institute report assessing various policy proposals floated before the Bush safeguards went into force suggests that it was between 3,000 and 10,000 jobs.

- Global overcapacity is the biggest challenge to the steel industry in the United States as well as across the world. China is a big player in the global market for steel, accounting for one-half of world steel production and 45 percent of world steel use. However, China is not a main direct supplier of steel to the United States — only about 2 percent of U.S. imports of steel mill products come directly from China, in part due to existing anti-dumping and countervailing duties already imposed on Chinese steel. Canada, Brazil, Korea, and Mexico were the main sources of U.S. imports in recent years, as well as others like Europe and Japan. Overcapacity is not an exclusively China-driven phenomenon, but a global one. The Organisation for Economic Co-operation and Development (OECD) identifies government interventions as a key cause of long-term excess capacity in the steel industry. Some emerging markets have intervened to encourage steel production as an engine for employment and to spark downstream industry or, like China and India, as a way to help support the construction needs of rapidly growing domestic economies. It is hard to unwind these policies. Because the steel industry has tended to support relatively high-paying jobs and innovation, governments in many advanced economies do not like to see steel plants close, either. The result has been a longer-term excess capacity: steel-producing capacity more than doubled and the gap between capacity and demand nearly tripled between 2000 and 2015 (see here Figure 1). While OECD countries as a group have reigned in capacity growth, non-OECD countries are still undertaking net capacity expansion (see Annexes 1 and 2 and Table 2). Previous administrations have tried to address this problem; President George W. Bush levied tariffs of up to 30 percent from March 2002 to December 2003 on a range of steel imports and focused attention on multilateral negotiations through the OECD, while the Obama Administration used a multi-pronged approach, with trade acts in 2015 to enable tighter enforcement of anti-dumping rules and countervailing duties. The Obama Administration also intensified bilateral and multilateral efforts, helping establish the OECD Global Forum on Steel Excess Capacity.

What this Means:

The Trump Administration has until April to decide whether to implement the recommendations to restrict or tax steel imports. The Commerce Department made the recommendations under a seldom-used legislative provision, Section 232 of the Trade Expansion Act of 1962, which allows trade interventions in the interests of national security. However, a recent memo from the Secretary of Defense reports that U.S. military requirements for steel (and aluminum) represent only three percent of U.S. production and expresses continuing concern that the two options involving global tariffs or quotas could have a “negative impact on our key allies.” At the same time, past experience shows trade restrictions on steel will raise costs for manufacturers that rely on steel as a direct or indirect input into production. Across many states, the number of jobs adversely affected in these steel-using industries could far exceed any steel jobs saved. Past experience also shows that unilateral action like Section 232 tariffs will invite retaliation — the Bush-era steel tariffs led many countries to target politically sensitive U.S. exports like Florida oranges and North Carolina textiles. China has already threatened to retaliate against agricultural goods such as soybeans (for which China is the largest U.S. export market) and EU officials have reportedly begun drafting possible measures aimed at Kentucky bourbon and Wisconsin dairy products. It is also unlikely that a unilateral U.S. tariff will provoke an end to production subsidies and other interventions in foreign countries. The root problem, global overcapacity in steel production, is best addressed through multilateral efforts like the OECD Global Forum on Steel Excess Capacity, which the United States helped pioneer in 2016, and has likely led to some cuts in production and capacity. But the current Administration did not send the United States Trade Representative or any Senate-confirmed representative to the recent Ministerial meeting of the Global Forum on Steel, weakening prospects for progress.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.