Is China Weakening the Yuan to Fight U.S. Tariffs? (UPDATE)

Fletcher School, Tufts University

The Issue:

The yuan has declined in value against the dollar by about 9 percent since the Spring of 2018. A weaker yuan tends to make Chinese goods cheaper in the United States and would partially offset the tariffs that the Trump administration is imposing on Chinese imports. Treasury Secretary Steven Mnuchin accused China of allowing the yuan to weaken to offset the effects of U.S. tariffs while at the G-20 Economic Summit in Japan in June. The Commerce Department is considering regulations to treat currency undervaluation as an unfair export subsidy. But while the yuan has been weak against the dollar, its value has remained stable against other currencies, with an index of the yuan against the currency of 60 countries 0.7 percent stronger in May 2019 than it was in October 2016. And, as will be demonstrated below, while the dollar has been strong against the yuan, it has also been strong against other currencies as well.

While the Chinese government maintains broad control over its currency’s value, the key point is that the dollar is strong against a wide range of currencies, and not just the yuan.

The Facts:

- The Chinese government largely manages the value of the yuan, not least through its restrictions on capital flows into and out of the country and the use of its stock of foreign currency reserves. However, the capital controls are not airtight, and market pressures do influence the exchange rate to some degree. Exchange rate policy in China has gone through gradual reform since 2005; the government shifted from promoting exports with a fixed exchange rate that many considered undervalued to allowing its currency to appreciate and even, in the wake of financial disruption in August 2015, undertook efforts to keep the yuan from falling in value (See this 2019 International Monetary Fund (IMF) report for a recent history of exchange rate policy in China). The IMF estimated the value of an index of China’s currency with respect to its trading partners to be fairly valued in 2017, and this index shows a stronger yuan in the first half of 2019 than its 2017 average value. Similarly, the Japanese financial firm Nomura published a March 2018 report stating that the yuan was stronger against the dollar than what was warranted by underlying economic conditions and, if anything, was poised to weaken in the future.

- Most analysts agree that the dollar is significantly overvalued against the currencies of its trading partners — not just the yuan. A broad index of the value of the dollar against its trading partners (adjusting for inflation) has risen by over 7 percent since April 2018. This reflects U.S. policies, including the fiscal expansion related to the December 2017 tax cut and subsequent increase in government spending, and the strong U.S. growth relative to other countries. One important source of the overall strength of the dollar is the large federal budget deficit, and the prospect for ongoing and increasing deficits, since these draw in capital from the rest of the world to finance the deficit and the inflow of capital bids up the value of the dollar.

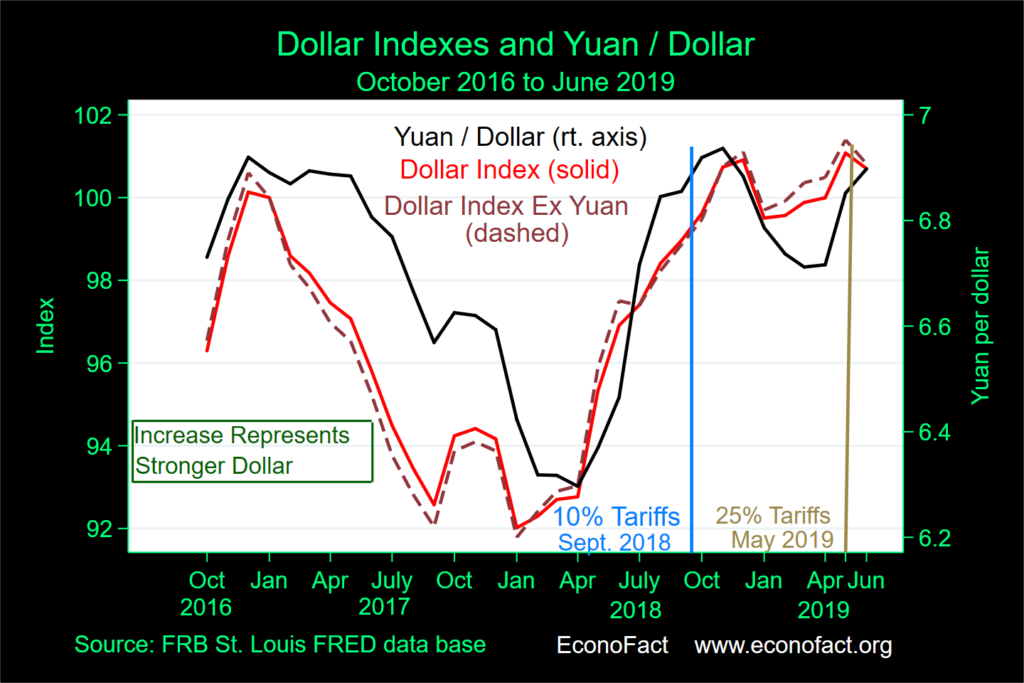

- The movements of the dollar against the yuan closely track an index of the dollar against its other major trading partners. The chart illustrates the movement of the bilateral exchange rate between the United States and China, as well as the value of the dollar against its other major trading partners. The dollar weakened against the yuan and also against the currencies of the major trading countries between late 2016 and the beginning of 2018 (it took fewer yuan to purchase a dollar, as shown with reference to the right axis, and the index fell, as shown with reference to the left axis). Subsequently, the dollar strengthened both against the yuan and against all other currencies. The common path of the dollar against the yuan, and of the dollar against currencies other than the yuan, becomes even clearer by comparing the solid orange line (the dollar against all its major trading partners) and the dashed red line (the dollar against all its major trading partners but for China). These two lines follow each other very closely over the entire three-year period depicted in the figure. In particular, both index lines show a strengthening of the dollar during the first three quarters of 2018 and, after a small retrenchment at the end of the year, continued strengthening in the Spring of 2019. In fact, the index that excludes the yuan strengthened a bit more during 2019 than the index that included it. (The index of the dollar against the currencies of 25 countries plus the euro area weights currencies by the amount of their trade with the United States. The dashed red line represents the broad index but excludes the Chinese yuan, the weight given to the yuan is about 16 percent during this period).

What this Means:

President Trump claims that the weak yuan represents an effort to offset tariffs imposed on China by his administration; the 10 percent tariffs on $200 billion of Chinese imports in September 2018 and the raising of these tariff rate to 25 percent in May 2019. The President has even demanded that the Federal Reserve weaken the dollar in response. While the Chinese government maintains broad control over its currency’s value, the key point is that the dollar is strong against a wide range of currencies, and not just the yuan. This broad strength points to domestic sources of the dollar’s high value, not Chinese actions. The most likely sources are widening U.S. budget deficits and the strength of the U.S. economy relative to its trading partners.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.