Breaking Barriers to College for High-Achieving, Low-Income Students

March 17, 2019

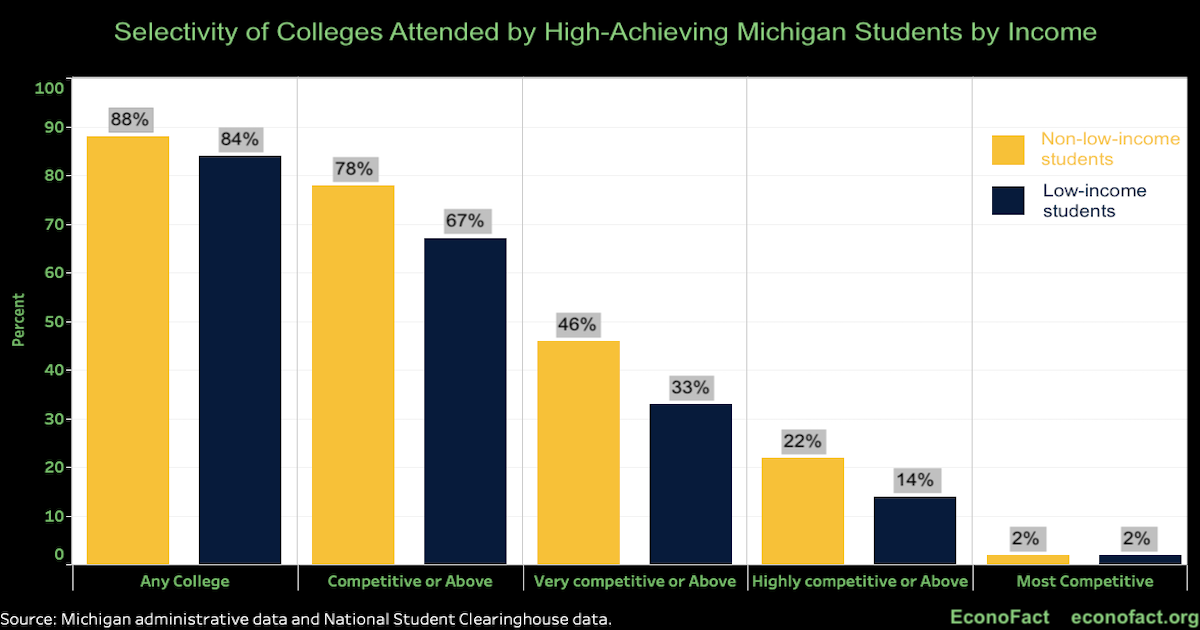

Most low-income students with strong academic credentials do not even apply to highly selective colleges. New evidence shows low-cost outreach can be effective.

March 17, 2019

Most low-income students with strong academic credentials do not even apply to highly selective colleges. New evidence shows low-cost outreach can be effective.

July 29, 2018

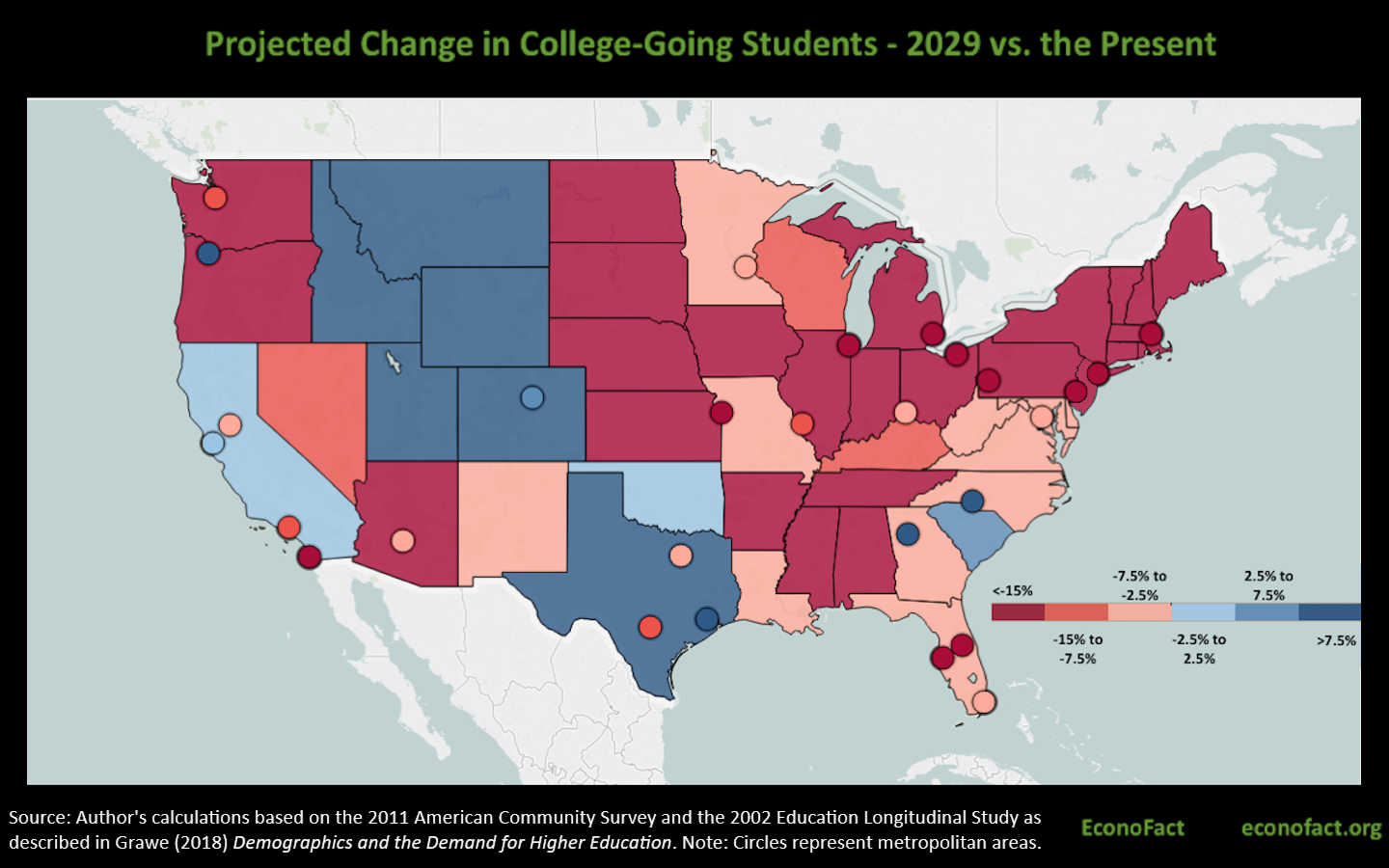

The population shift towards the Southwest, coupled with a drop in the U.S. fertility rate, suggest the potential for significant contraction and realignment in higher education in the next 10 to 15 years — if the patterns that currently link demographic factors to the demand for higher education continue to hold.

July 19, 2018

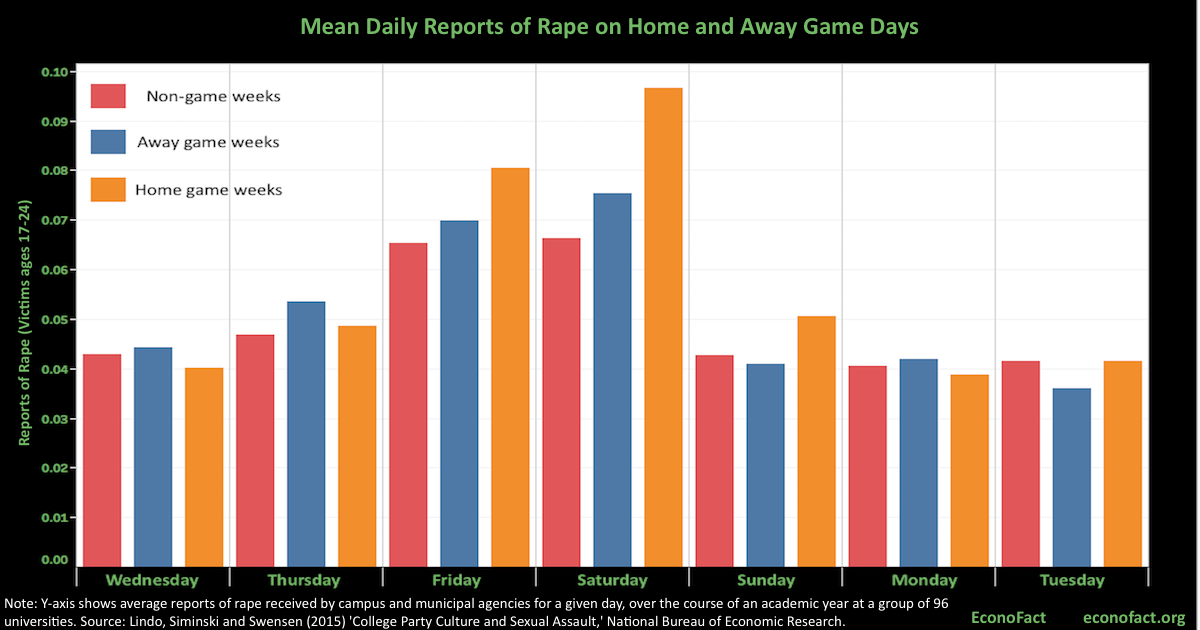

Football games at Division 1 schools are associated with increased reports of rape among 17 to 24 year olds. Could targeting alcohol and the party culture associated with game days help reduce sexual assaults on campus?

March 22, 2018

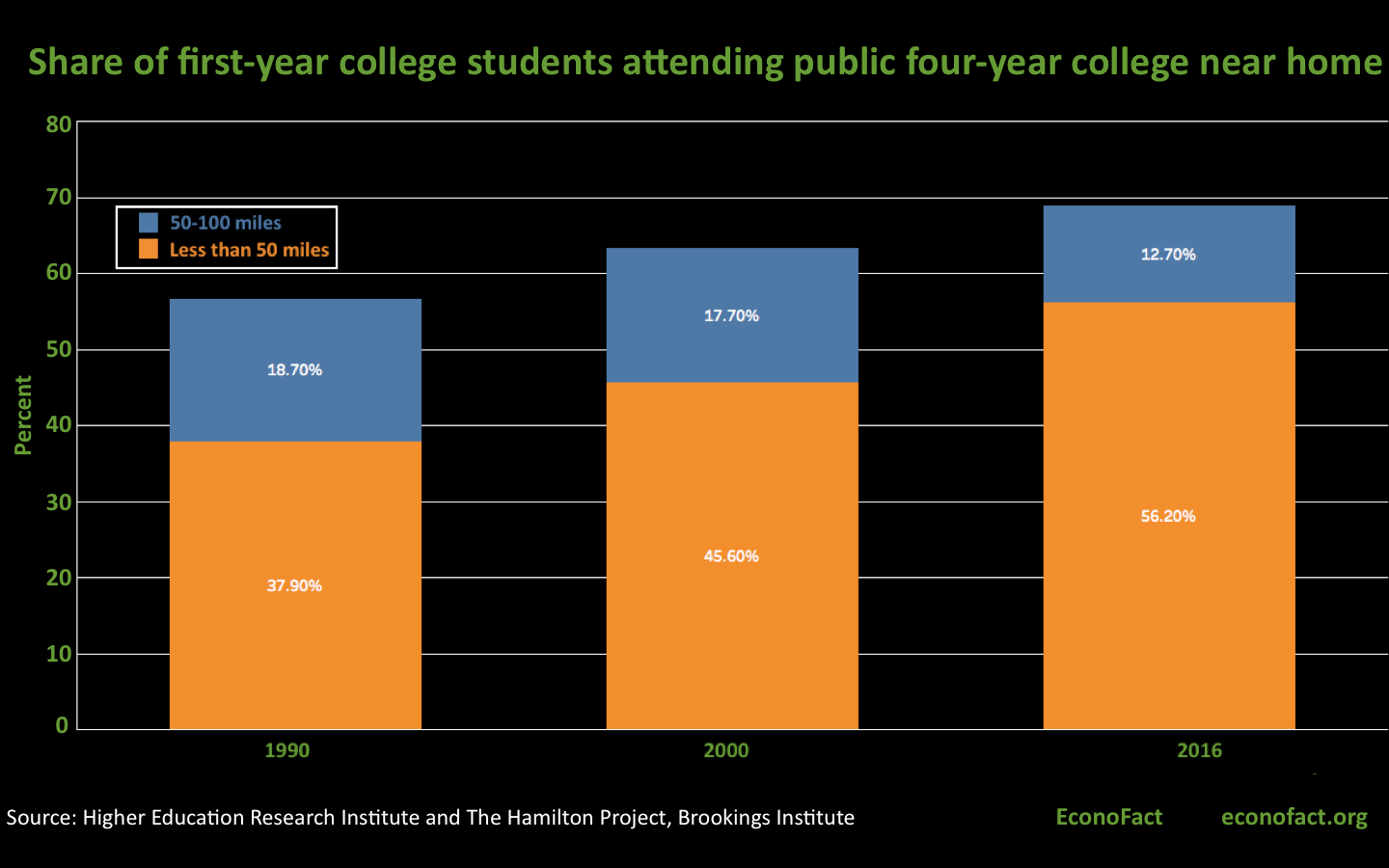

Geographic location is important in determining not just where, but whether, a high school senior goes on to college. About 1 in 6 lack a nearby college.

January 25, 2018

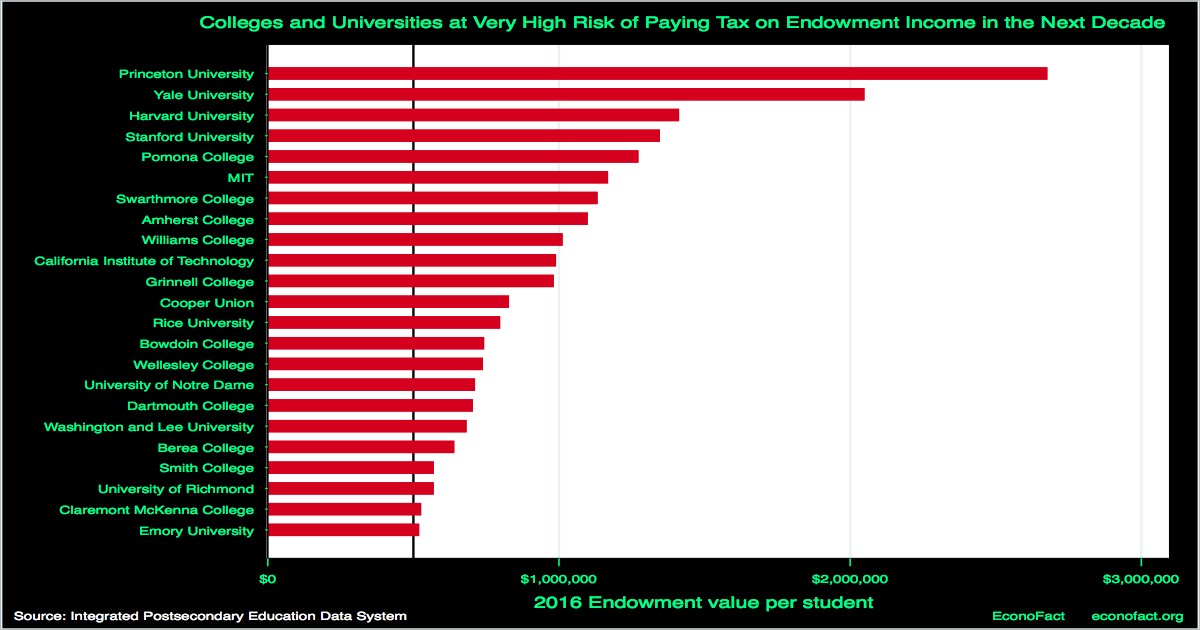

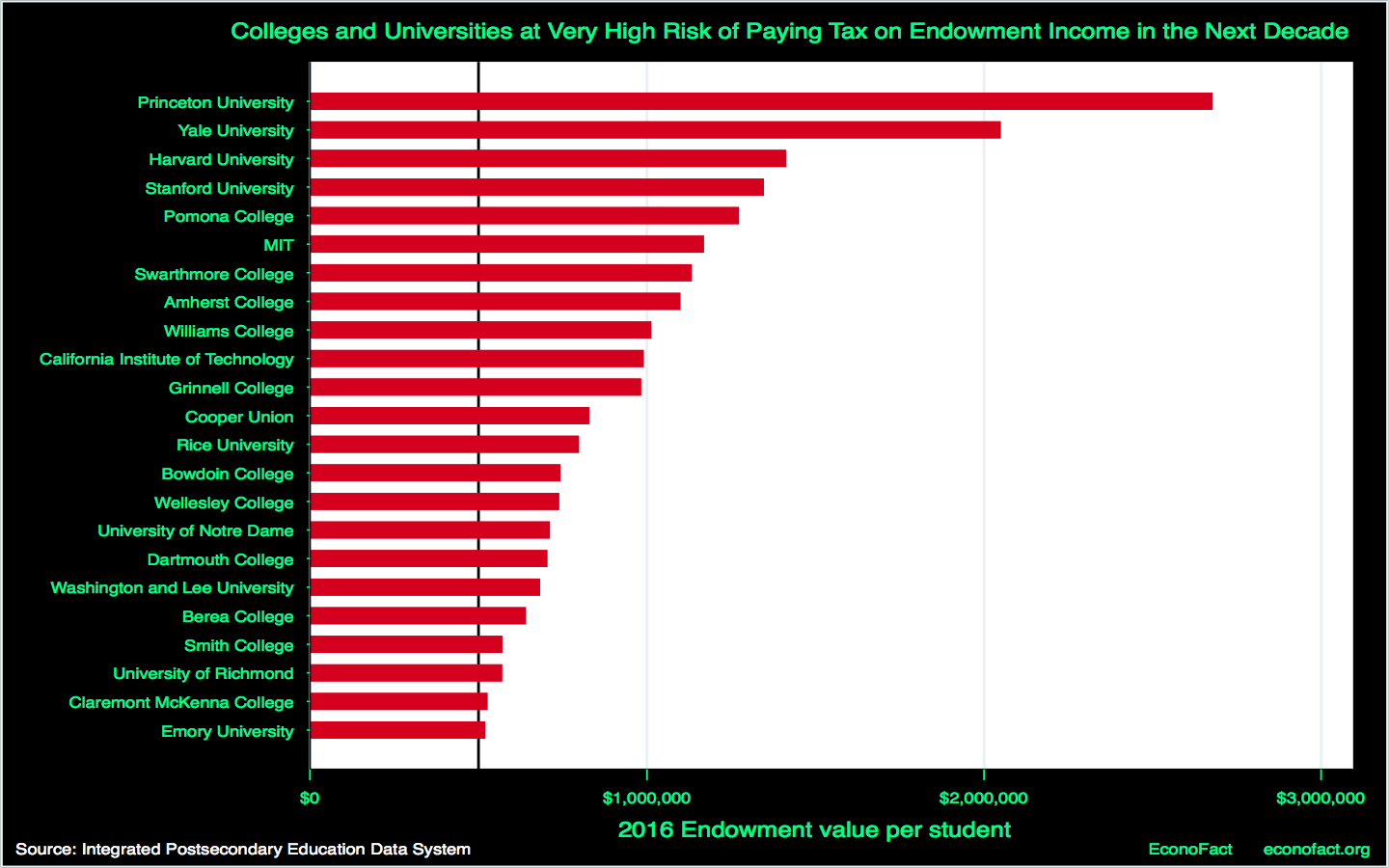

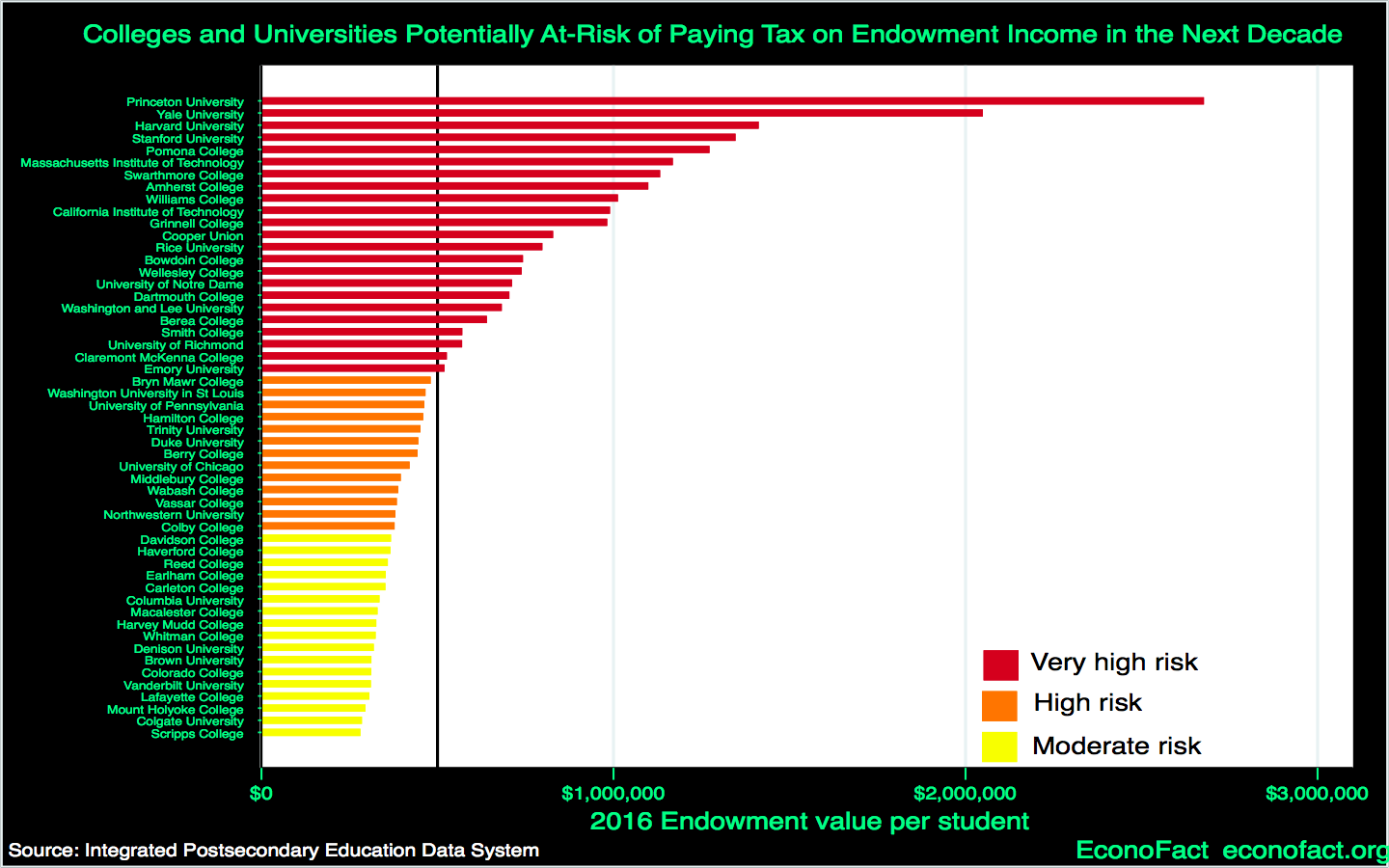

The recently enacted federal tax legislation levies a tax on the endowment income of colleges and universities with large endowments.

(This is an interactive graph. Hovering over the dots reveals institution names.)

July 17, 2017

U.S. Secretary of Education, Betsy DeVos has rolled back Obama-era regulations designed to protect student loan borrowers from punitive fees and shoddy service.

May 30, 2017

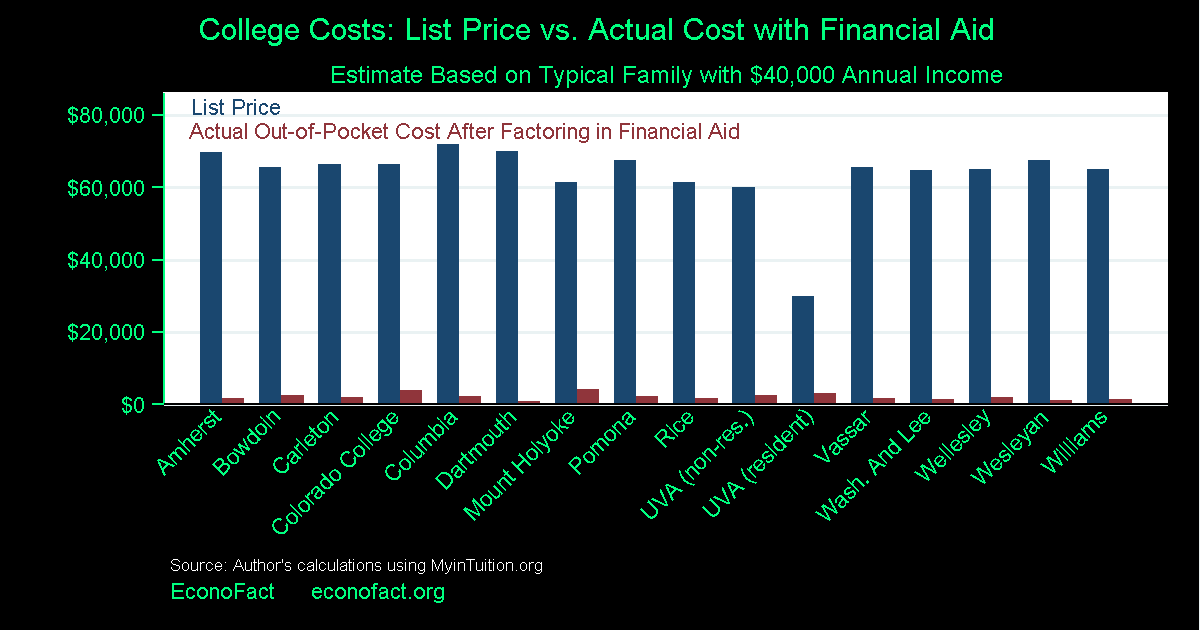

How much would a college education really cost? Schools are making it easier to answer this question and it may make a big difference for low-income students.

May 24, 2017

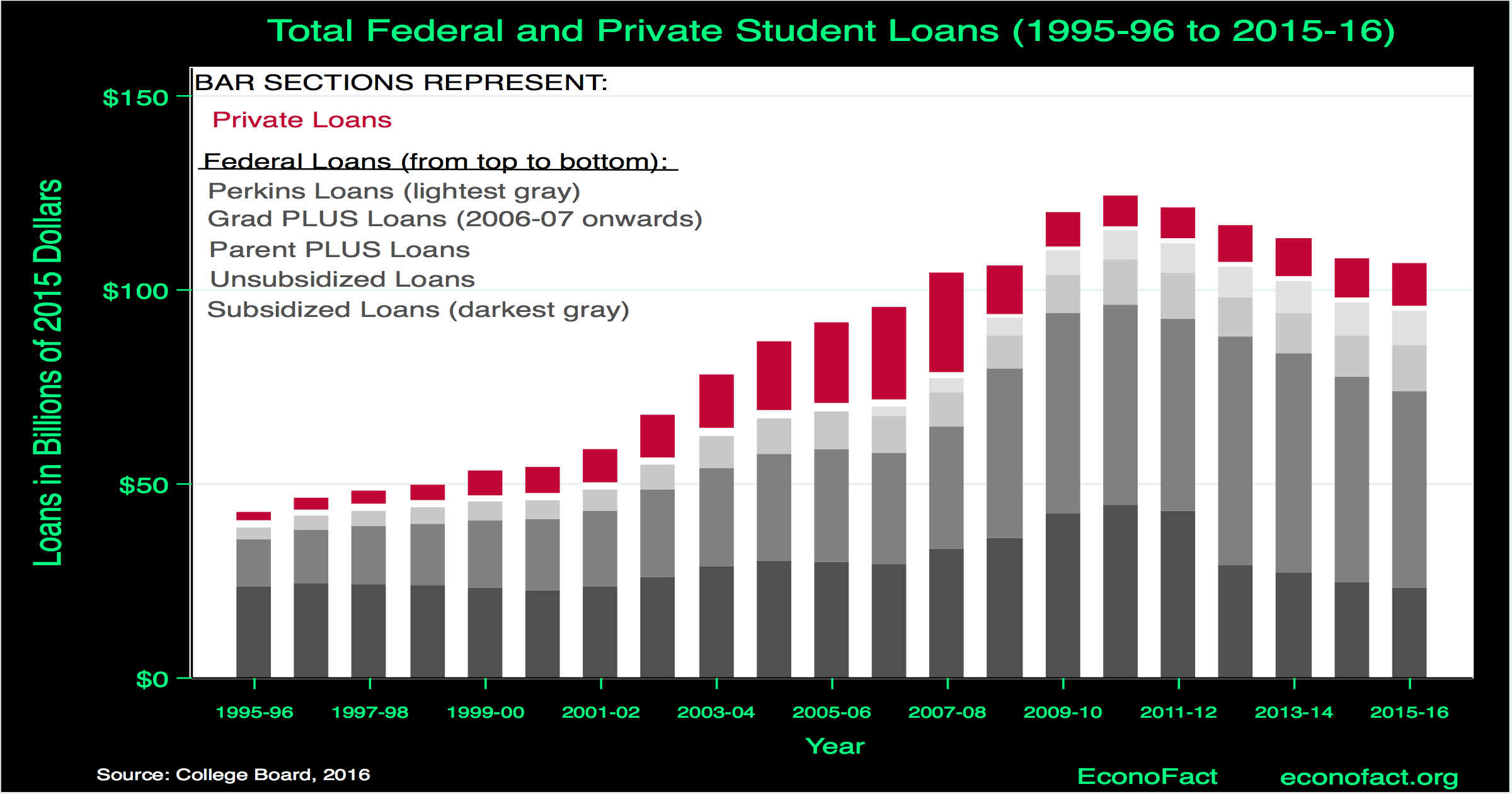

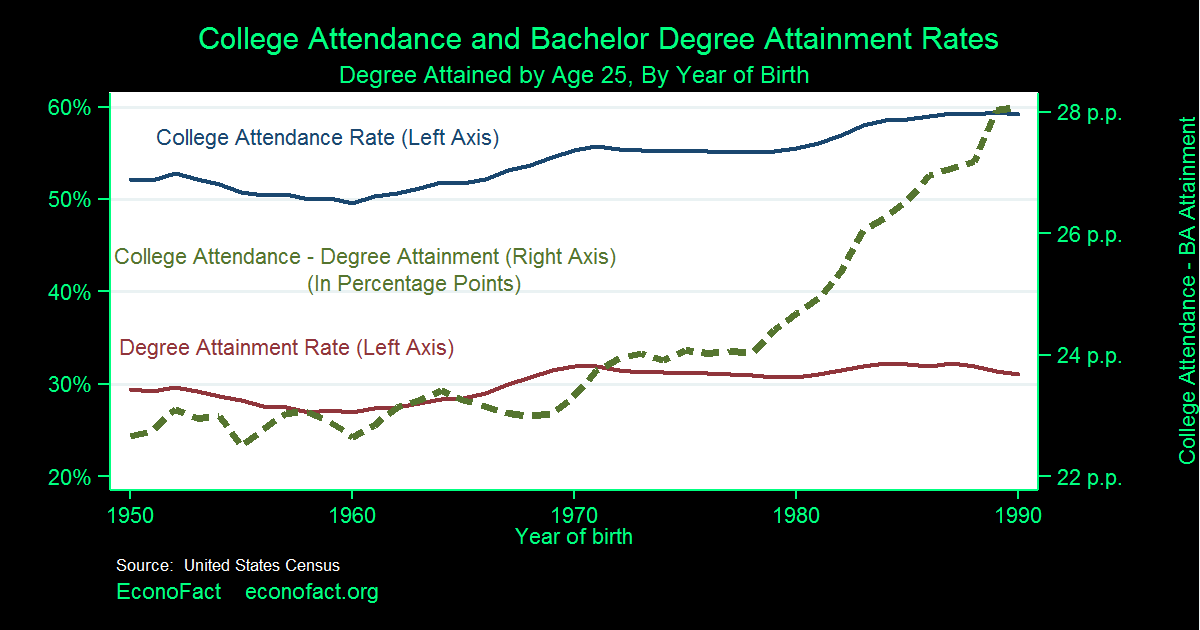

While college attendance rates have climbed steadily, college completion has not kept pace. College dropouts are much more likely to default on student loans.

{kind=link}