The Financial and Psychological Costs of Income Volatility

Duke University and Georgetown University

The Issue:

Much attention is devoted to economic uncertainty at the national or even global level which can impact large swaths of the population directly. Issues such as unforeseen price spikes can impose very real constraints on people’s spending and lead to difficult choices; an unexpected financial shock can spread and cost jobs. Yet many families experience chronic, high levels of additional uncertainty in their daily lives due to the variability and unpredictability of the income they depend on. Income volatility can stem from unexpected layoffs, gig jobs with irregular and variable hours, compensation that depends on tipping, as well as uncertainty in the receipt of government assistance and benefits, among other factors. When it is not predictable or voluntary, this instability can impose large costs on workers and families, putting demands on people that can subsequently undermine their economic and general well-being. The instability can impact their mental health and sleep, as well as the cognitive attention they have available to put towards work, self-care, providing care for children, or to positively engage in parenting.

Individuals and households with the lowest baseline income level experience the most unpredictable earnings streams.

The Facts:

- Income volatility is the amount of income or earnings that deviates from what might be expected to represent average income available to people. The availability of money to households is typically measured by calculating income across all their sources over some time period, typically a year; it is then assumed that this amount is available for spending or saving in equal increments or that people can smooth spending irrespective of deviations or variation of income, whether higher or lower. But measures of annual income obscure the fact that, for some families, income can fluctuate widely from week to week, or month to month, or even day to day, over the course of a typical year. Some of these fluctuations are expected and some happen unexpectedly. Measures of income volatility try to capture these deviations.

- People experience income volatility, particularly earnings volatility, for many reasons. Earnings can be volatile because of seasonality of jobs, characteristics of work hours and work hour schedules, voluntary or involuntary job changes, entry into and exits from work, including those driven by life events such as a health crisis, formats of payment (as large lump sums or routine payments), or rebalancing of time in work and other obligations such as care giving that might require fewer hours in paid employment. Income received as assistance, either privately or from the government, can be stabilizing or further escalate income volatility. Some government assistance programs help buffer against earnings volatility. One prominent example is the Supplemental Nutrition Assistance Program (SNAP, formerly known as food stamps), which provides monthly benefits that are uncoupled from earnings requirements. Indeed, when you take into account the contribution from food stamp benefits, the gap in income volatility between poor and rich households becomes smaller, according to one study (see Figure 10.) However, government income support is not always predictable, can be time limited and can become unavailable unexpectedly due to recertification requirements to verify eligibility, or are simply difficult to access in real time in a way that can act as financial emergency back stops to income drops.

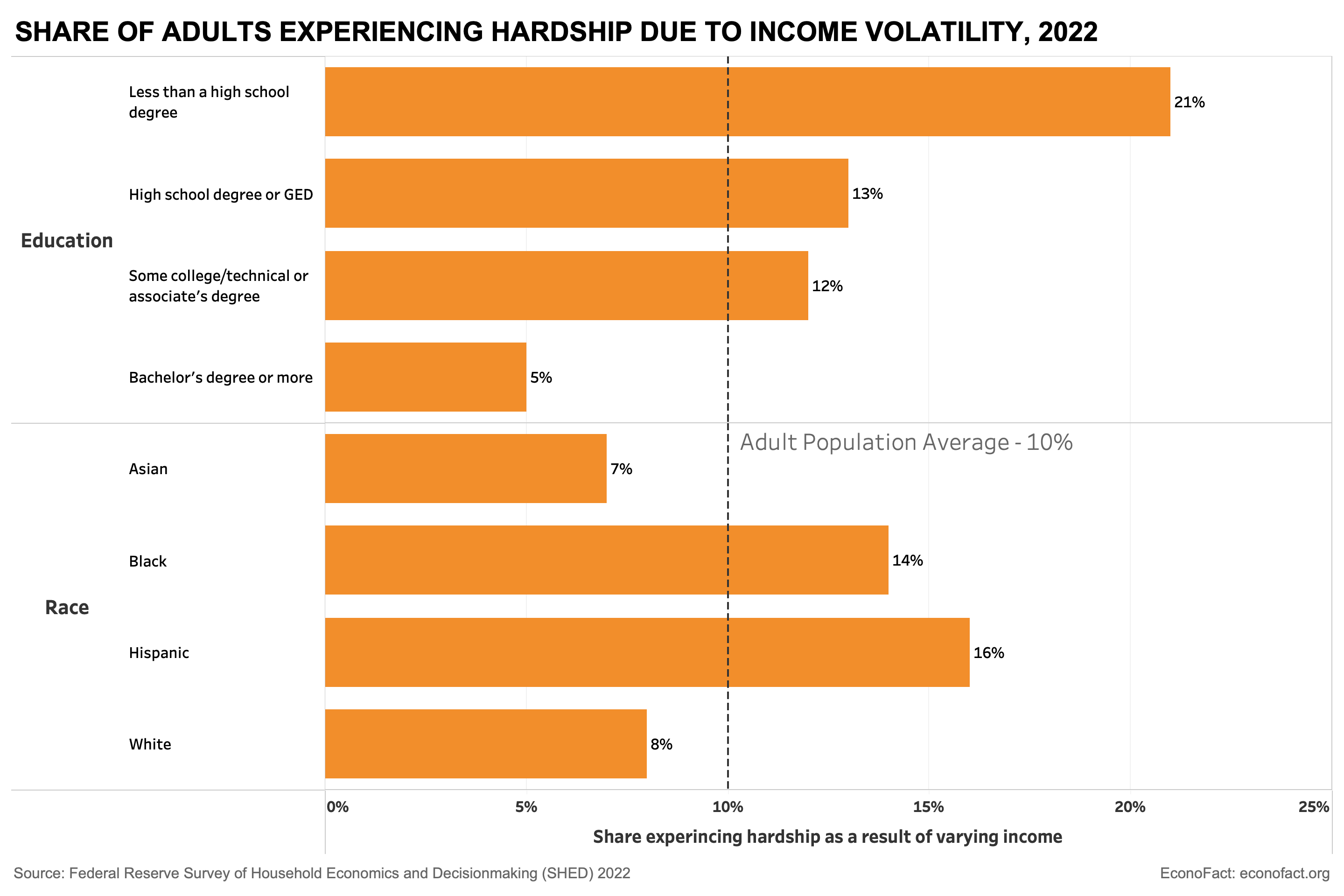

- There is consistent evidence that individuals and households with the lowest baseline income level experience the most unpredictable earnings streams. Income volatility is particularly pronounced for those at the bottom of the income distribution. In 2022, 3 out of 10 adults reported that their income varied from month to month. This variability represented financial hardship for 1 out of 10 who reported they struggled to pay their bills in the past 12 months, according to the Federal Reserve’s Survey of Household Economics and Decisionmaking (see chart). However, the share for whom income volatility caused financial hardship was much higher for those with lower education (20%) and for Black (14%) and Hispanic (16%) adults. And there is some evidence that the volatility of income for those at the lower end of the income distribution increased between 1980 to 2010 for households with children. One study finds that households with children at the 10th percentile of income experienced increasing volatility between 1984 and 2010 while income volatility for their affluent peers at the 90th percentile declined. As a result, the difference in monthly income volatility between low- and high-income households with children grew by more than four times during this period.

- There are many reasons why those at the lower end of the income distribution experience a greater degree of earnings instability. First, the structure of the low-wage labor market has shifted jobs away from stable, salaried employment, towards temporary and flexible positions for workers in service occupations with lower skill requirements. This means that workers with lower levels of education are more likely to experience large variations in hours worked. Second, over time, since the 1990s in particular, safety net benefits are conditioned on proof of employment or work-related activities (with the accompanying procedures to verify eligibility). The combination of less stable employment for lower income jobs with an increase of conditioning safety net benefits on meeting work requirements means that people with the lowest economic resources are the most susceptible to uncertainty in earnings and in government income support.

- Income volatility has negative impacts on consumption, parenting, and children’s schooling beyond the effects of income level. The involuntary income fluctuations experienced by low-income families directly affect their capacity to predictably consume basic needs. Recent research finds higher consumption variability for many economically vulnerable groups — including those with lower incomes, Blacks, and those with fewer educational credentials. Food, entertainment, and personal care goods and services show the highest consumption variability among households with low-income. In addition, financial volatility, particularly when income is low and not predictable, stretches attention and related cognitive resources. Adult workers must balance the task of planning finances under uncertainty and with limited access to loanable funds markets. Parents are additionally tasked with balancing the needs of their children. These circumstances are likely to increase family stress, disrupt family routines and direct parental attention towards juggling day-to-day basic needs. The instability has a measurable negative impact on children’s school engagement and attendance their behavior and disciplinary infractions, their achievement test scores and their long-term educational attainment. These conditions were all worsened over the COVID19 pandemic, further stressing workers and parents time and attention.

- Options for households to buffer against the cost of income volatility vary, particularly along dimensions of economic vulnerability. For many, low income is also coupled with low wealth, which makes it difficult to use savings to maintain a family’s consumption during periods when earnings drop. Up to 15 percent of households with children experience both income and net worth poverty, especially among Black and Latino child households (see here and here). Moreover, access to low-cost credit and insurance against catastrophic events are more limited for people with the lowest incomes and Black and Latino households face the highest-cost options for borrowing. Many government programs available to workers and parents with children — at times depending on the state or local government administering benefits — are not certain or predictable. Eligibility and amount of safety net benefits change when family or work circumstances change, and steps required to apply, re-apply, prove eligibility and the like (sometimes referred to as administrative burdens) can further impose uncertainty. This means that programs designed to provide immediate economic relief may not act quickly enough when assistance is most needed. COVID19 pandemic related cash support, and the expanded child tax credit, helped many households but their reliance on these sources was also precarious — it was unclear how long the benefits would last, for instance, making it difficult to plan. (Hence people may have used stimulus payments to save in anticipation of future income or consumption uncertainty rather than use them to fully supplement their immediate needs, given dramatic drops in income).

What this Means:

Prevailing attention on macroeconomic uncertainty is important but also does not help address income volatility that affects the daily lives of households. People cannot budget well when they do not know whether or how much income is to be available, even when policies deliver on their intent to increase overall household income. The financial and psychological toll of income volatility can be very high especially for people with low-incomes and their children—who face volatility with the fewest financial buffers or protections. Designing safety net and related income support policies may have bigger returns if they are stable and predictable and can act as economic buffers amidst other sources of macro or labor market uncertainty.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.