The Rising Burden of U.S. Government Debt

Brandeis University

The Issue:

Interest payments on federal government debt are projected to reach $892 billion in 2024. This is more than the government is projected to spend on defense and almost a third higher than what the United States spent on debt interest payments in 2023. This increase reflects the combination of the rise in US government debt and higher interest rates. And, even though interest rates are expected to inch lower in the coming years as inflation subsides, the Congressional Budget Office (CBO) forecasts that interest payments as a percent of GDP will continue to rise. The extent of this increase was not foreseen even in the past few years — the CBO’s projections of the interest burden of the debt have been steadily increasing.

US debt interest payments have risen sharply due to the combination of increasing government debt and higher interest rates.

The Facts:

- The current high cost of servicing the national debt is partly a reflection of the historically large size of the federal government debt. Government debt is the sum of current and accumulated past budget deficits as well as the cumulative cost of financing those deficits. There has been a notable increase in US government debt since the economic downturn of the Great Recession, which required increased federal spending and lowered tax revenues and was followed by the pandemic shock. In addition, there has been a lasting downshift in government revenues due to changes in tax policy since 2000, which has also significantly contributed to the mismatch between government revenues and government spending (see here). Since 2020, debt-to-GDP levels have been higher than at any time since the late 1940s. At $28.2 trillion, the total federal debt held by the public is projected to be 99% of GDP by the end of 2024.

- The cost of servicing the debt has also been rising as a result of increasing interest rates. Interest rates have been high as the Federal Reserve raised its benchmark Fed funds rate from near zero in March of 2022 to a range of 5.25-5.5% in July of 2023 to fight the inflation surge that followed the pandemic recovery. As a result, borrowing costs have risen. The yield on the 10-year Treasury bill was 4.2% in June 2024, as yields have hit the highest levels in 15 years. While the Federal Reserve is expected to begin reducing the Fed funds rate as the slowdown in inflation continues, the Congressional Budget Office forecasts that the rate on 10-year Treasury notes will decline slowly to 3.6% by the fourth quarter of 2026 and then rise gradually again, reaching 4.1% by 2034.

- The combination of large debt and high interest rates means that the federal government’s cost of servicing its debt relative to national income is reaching all-time highs. At a projected $892 billion in 2024, interest payments on the federal debt represent 3.1% of GDP in 2024. Since 1940, net outlays for interest have never exceeded 3.2 percent of GDP. But, in the CBO’s June 18, 2024 outlook government spending on debt service is forecast to exceed that percentage every year from 2025 to 2034. About two-thirds of the growth in net interest costs forecast from 2024 to 2034 stems from expected increases in the average interest rate on federal debt, and the remaining third reflects the expected increase in the amount of debt.

- The interest burden of the debt partially depends upon the maturity structure of the debt. The US Treasury considers trade offs when deciding how to finance the current budget deficit and the rolling over of maturing debt. One decision involves the pattern of maturities of outstanding debt. The US Treasury issues debt with maturities as short as one month and as long as 30 years. Short-maturity debt requires frequent rolling-over of the debt which makes the Treasury susceptible to greater volatility in interest payments. Longer maturity debt such as 30-year Treasury bonds typically pay higher interest rates than shorter maturity debt such as 3-month Treasury bills (although not always, and not recently). Most of the outstanding debt in late 2022 was scheduled to mature within the subsequent three years. That debt has been refinanced at higher interest rates, sharply raising debt service costs. For example, almost $7 trillion worth of debt held by the public was refinanced during the 2023 fiscal year (October 2022 through September 2023) and each percentage point increase in interest rates on that refinanced debt meant $70 billion per year more in net interest payments in that first year (for context, this is about 10 percent of the entire United States defense budget). The maturity structure of debt remains very short, with half of outstanding debt now maturing by 2026. Recent forecasts of interest on the debt reflect the fact that large amounts of federal debt will be rolled over at higher rates.

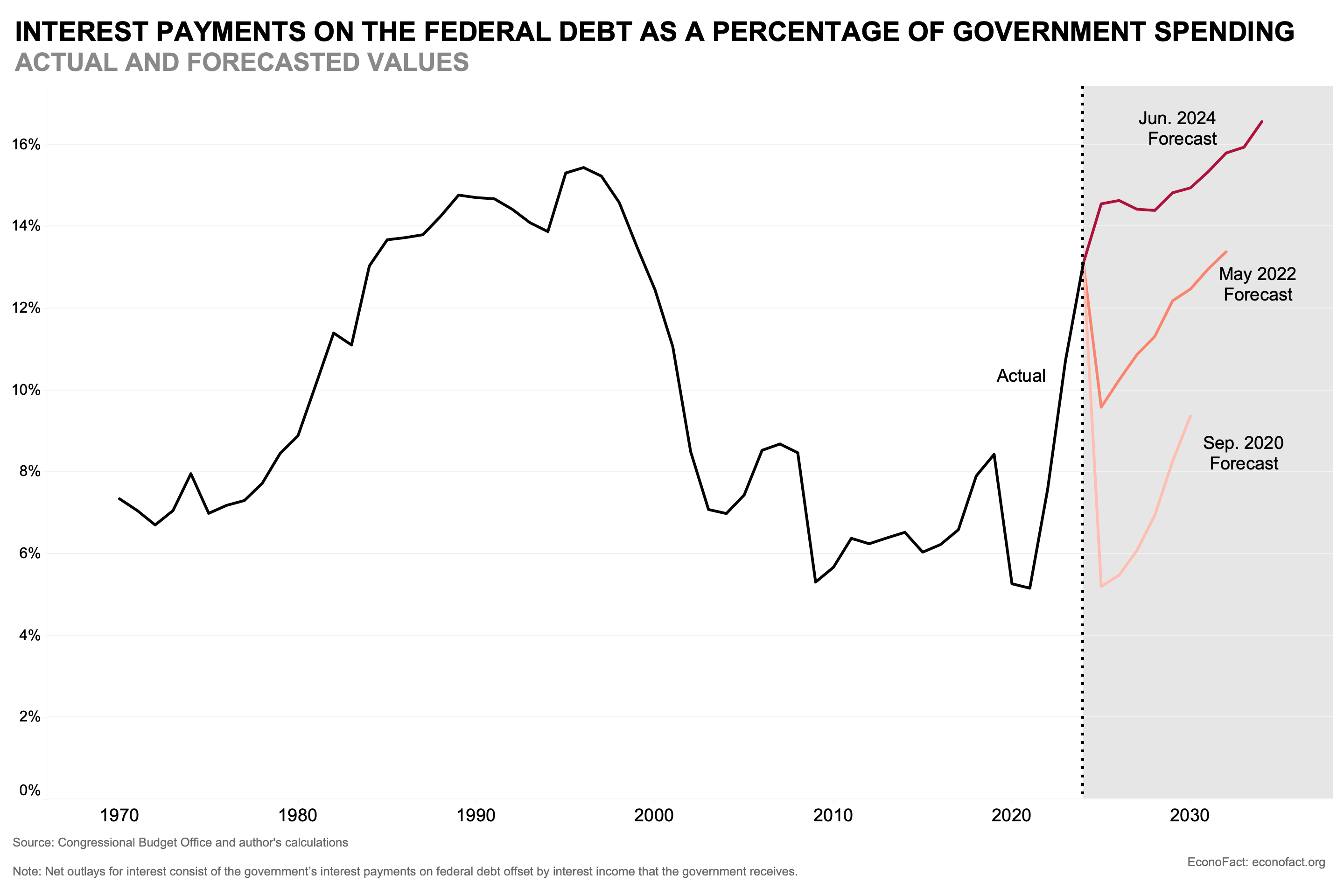

- Servicing the federal debt has been taking up an increasingly larger share of government spending. Interest payments made up about 13 percent of federal spending in 2024, being the third highest category of spending ahead of spending on defense, Medicare and income security programs (see here). This is a sharp increase from 2017, when net interest payments made up closer to 7% of government outlays and is approaching the situation of the mid-1990s when net interest payments reached over 15 percent of fiscal outlays (see chart). This was at a time when the overall debt held by the public as a percentage of GDP grew from 23 percent to 48 percent. The reduction of debt payments from the mid-1990s to the mid-2010s reflects both lower interest rates and a lower level of debt. Although the debt-to-GDP ratio rose between 2009 and 2017, net interest payments as a share of total federal outlays remained below 7 percent during this period primarily because of low interest rates.

- Projections of the interest burden of the debt have increased dramatically over the past four years. The Congressional Budget Office currently projects that interest payments on debt will be more than 16 percent of federal spending in 2034. Current projections are well above those made two or four years ago (see chart). The differences between forecast and actual values, and the rising forecasts over time, reflect the effects of changing expectations on both interest rates and debt.

What this Means:

Higher interest payments mean less government spending is available for defense, social safety net programs, research, and other important government functions. Rising levels of debt service contribute to fiscal challenges that our country faces. As interest payments become a higher share of government outlays, the US has to cut spending on other categories or raise tax revenues in order to keep deficits from ballooning and require even more borrowing. The cost of debt service will depend on both the level of debt outstanding and the level of interest rates. Debt has risen to levels that are high by historical standards, but — until recently — that increase has coincided with very low interest rates that have kept the costs of debt service relatively low. However, the high levels of debt mean that increases in interest rates like those that we have seen over the past two years will have a large impact on our country’s budget deficits that could require increases in taxes or reductions in spending.

Topics:

Debt and DeficitsLike what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.