Can a Tax Credit Help Balance Work and Caregiving?

W.E. Upjohn Institute for Employment Research

The Issue:

Paying for the care of children or adult dependents is a significant expense for a large share of working families. To make it easier for families to afford care, the federal government and many states allow families to claim some amount of caregiving expenses and receive a tax credit to reduce tax liabilities. Emerging research finds that increasing the generosity of the Child and Dependent Care Tax Credit increases paid child care use. This suggests that the credit assists at least some working parents in paying for care. Nonetheless, the value of the credit is small relative to the cost of care, does not keep pace with inflation, and fails to reach low-income families who do not have positive tax liability after deductions.

Between 2009 and 2023, Child and Dependent Care Tax Credit benefits covered just 10–20% of out-of-pocket child care spending.

The Facts:

- High care costs for children and older adults put an increasing strain on American families. Child care prices for just one child typically range from 9–16 percent of median family income, and costs for long-term care services for older adults exceed these households’ median annual income. High care costs may push caregivers out of the labor force, jeopardizing their long-term earnings, or shift care recipients into less expensive, lower-quality care arrangements that could compromise their safety and, for children, hinder their human capital development.

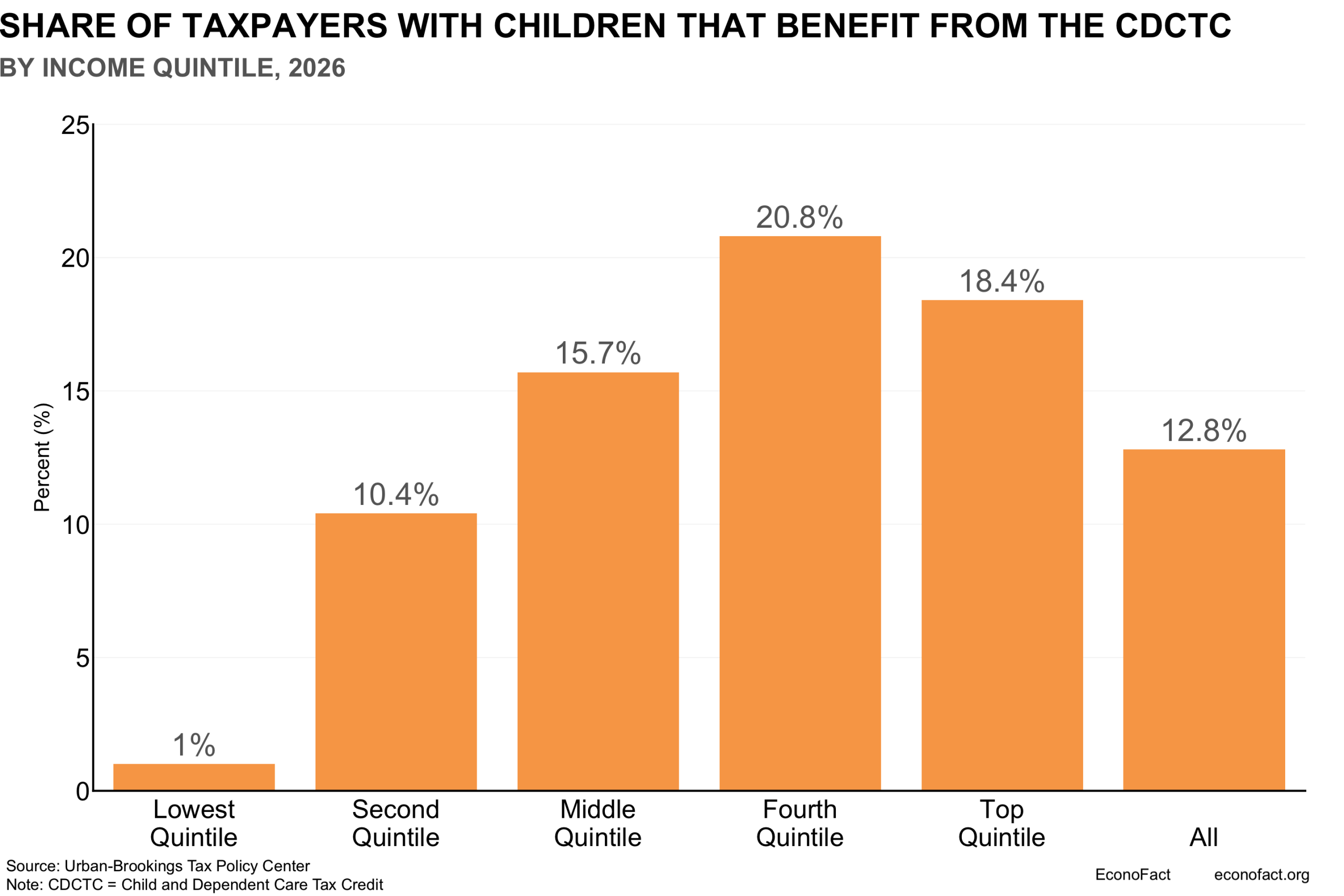

- The Child and Dependent Care Tax Credit (CDCTC) is designed to partially offset working families’ care expenses. In 1976, Congress implemented the federal CDCTC to defray taxpayers’ expenses related to caregiving services. The credit makes it easier for the taxpayer to work instead of providing care themselves. Each year, families can claim up to $3,000 of care-related costs on their taxes for up to two members of their household under the age of 13, or for qualifying disabled adults. The amount of the credit depends on the household’s income (see here). Claimants must work in order to qualify for benefits, and this applies to both spouses among married taxpayers filing jointly. It is a nonrefundable credit, which means that it can be used to reduce a taxpayer’s tax bill until they have zero tax liabilities — any excess credit beyond that is forfeited. As a result, low-income working families who owe little or no income tax receive little benefit from the credit. The Urban-Brookings Tax Policy Center estimates that in 2026, only 1 percent of families with children in the lowest quintile of income will benefit from the CDCTC (see chart). Moreover, the average benefit awarded to the families in the lowest quintile that receive the CDCTC is substantially lower than for higher income families. The Tax Policy Center estimates that families in the lowest quintile that receive the CDCTC will receive an average of $420 in 2026 — compared to an estimated average benefit of $890 among all taxpayers with children that receive the CDCTC.

- The CDCTC is one aspect of a patchwork of tax-based, in-kind, and other limited supports available to families with caregiving expenses. In addition to the CDCTC, this patchwork includes dependent care flexible spending accounts (FSA), employer-provided or state-mandated family and sick leave, and financial assistance for targeted groups, such as veterans or those with very low incomes and assets. The CDCTC and dependent care FSA are the only federal programs that directly subsidize out-of-pocket care expenditures. The CDCTC has the potential to reach taxpayers who may not benefit from the dependent care FSA: less than half of civilian workers have access to these accounts, and families must determine FSA contributions at the beginning of the year, precluding taxpayers whose caregiving responsibilities unexpectedly begin mid-year.

- There is evidence that the CDCTC can increase the use of paid child care and that it directly promotes labor force participation among secondary earners. The tax credit was expanded in 2003, generating differential increases in generosity across states and family sizes. I found that a $100 increase in tax credit generosity increased paid child care participation by 0.6 percentage points among single mothers and 2.2 percentage points among married mothers with children younger than 13 years old. Since both spouses in a married couple must work (unless one of them is the disabled qualifying individual) in order to claim the CDCTC, I find that CDCTC benefits increase workforce participation among married mothers in ways that other programs do not.

- Because the CDCTC is nonrefundable, it fails to reach about one in five earners — households making less than about $30,000 who do not earn enough to owe federal income taxes. This group includes many service workers, retail clerks, healthcare aides, and workers in other low-pay occupations. If the CDCTC were made refundable — which would allow households that do not earn enough to owe federal income taxes to receive tax refunds — I estimate that an additional 1 in 20 single parents would gain eligibility. Similarly, in joint work with Yulya Truskinovsky, we find that refundability would approximately double the number of eligible spousal caregivers. Eligibility increases would be largest among demographic groups with lower average household incomes and greater participation in Medicaid.

- The CDCTC has not kept pace with inflation and does not come close to covering typical care costs. The maximum credit in practice, after accounting for the CDCTC’s nonrefundability, is about $1,050 per qualifying individual, or a maximum of $2,100 for households with two qualifying individuals. To put these numbers into context, I find that between 2009 and 2023, benefits covered just 10–20 percent of out-of-pocket child care spending on average. In 2021, The American Rescue Plan Act made the CDCTC refundable and increased the maximum benefit to $4,000 per qualifying individual for that year only. I find that this covered around 40% of child care spending for most eligible households with children.

- CDCTC participation is low among taxpayers caring for adults. Ninety-five percent of CDCTC claims are made exclusively for child dependents. The CDCTC was designed “to help families pay employment-related expenses for care of a child,” and its requirements that its recipients both have earnings and live with the dependent may be better targeted at parents paying for child care than at adult caregivers. In many cases, adult caregivers do not live with their care recipients, and they tend to be further along in their careers than parents of young children. To better reach adult caregivers, the tax program could be split into separate child and adult care credits.

- States are experimenting with their own child care credits. About half of states offer supplements to the federal CDCTC, and a handful of states offer tax credits for adult caregivers. When states offer refundable and generous state tax credits, they help to compensate for the ways in which the federal CDCTC falls short.

What this Means:

When good care is affordable, the benefits extend beyond just parents and other caregivers. Subsidizing family caregivers’ out-of-pocket costs can keep older adults out of even more costly, publicly-funded institutional care. And investments in high-quality child care produce lasting social and economic returns — enabling more parents to work, benefiting employers, boosting the economy, and leading to long-term benefits for the next generation. The federal CDCTC is a policy lever that aims to reduce care costs and promote these outcomes, but it is hindered by major flaws in its design — namely, its lack of generosity and failure to reach the lowest-income families for whom child care presents the largest cost burden. A temporary CDCTC expansion during the Covid-19 pandemic, which made the tax credit refundable and increased the credit’s value, provides a blueprint for a credit that is generous enough to make a difference to family budgets. While the CDCTC alone is not a comprehensive solution to the financial challenges that come with taking care of children or dependent adults, the federal government and states can make it a more effective tool for reducing financial strain and filling gaps in the meager patchwork of supports available to families with care responsibilities.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.