Is Taking on More Student Debt Bad for Students?

Columbia University, Brigham Young University, U.S. Federal Reserve, and Vanderbilt University

The Issue:

Much of the recent public discussion surrounding student borrowing has focused on the potentially harmful effects of student debt. For example, there are important questions about the financial vulnerability of student borrowers and whether a large student loan payment burden might diminish or delay borrowers’ ability to purchase a home or finance other investments. However, there are also potential benefits of borrowing. In particular, access to student loans could allow financially constrained students to finance investments in education that they could not otherwise afford. This tension raises the question of whether students are better off when they can borrow more money to finance their college attendance, despite ending up with more student debt.

Raising federal student loan limits substantially increased borrowing — but it also raised graduation rates and led to increased earnings.

The Facts:

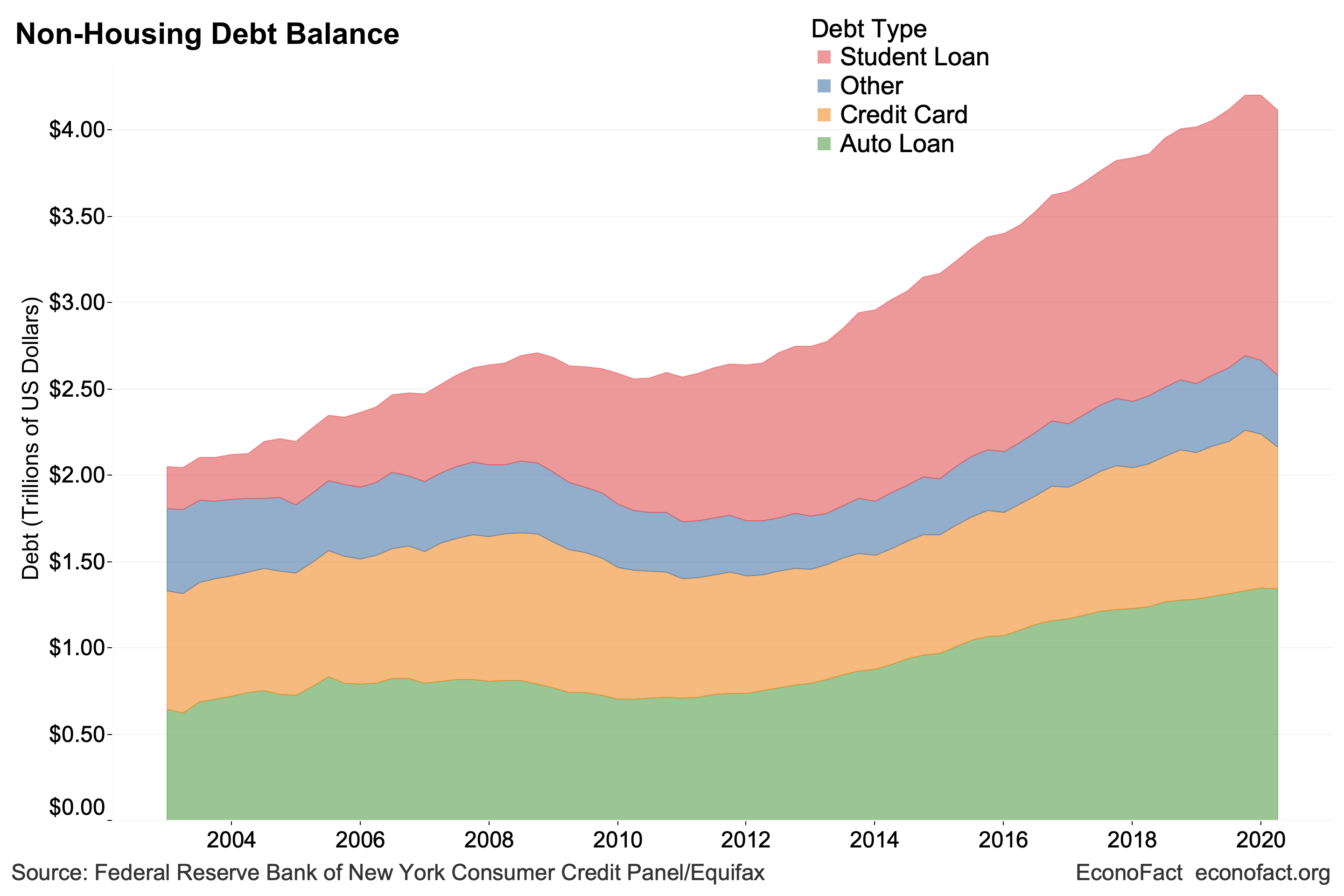

- Outstanding student loan debt has more than tripled since 2007 in the United States and now exceeds $1.5 trillion — surpassing credit card debt and auto loans to make up the most significant source of non-mortgage debt for American households (see chart). The growing share of student debt on household balance sheets reflects rising postsecondary enrollment as well as increasing college costs. More than half of U.S. undergraduates rely on federal student loans to finance college, according to our calculations using College Scorecard data.

- Concerns that growing student loan burdens may harm borrowers' post-college financial wellbeing, and even present a potential threat to the broader economy, have risen along with the level of outstanding debt. In recent years, policymakers and the popular press have voiced concerns about a student loan crisis that could be causing young Americans to delay purchasing a home and reach other life milestones. All else being equal, higher levels of student debt will increase a person's debt-to-income ratio and, thus, could reduce that individual's ability or desire to borrow to finance other investments. The growth of student loan debt could potentially also impact the broader economy — if student loan burdens dampen consumption and reduce economic growth, or if waves of defaults on the debt impair the financial system.

- However, these concerns must be weighed against the financial benefits of a college education made possible through borrowing. The gap in earnings between college and high school graduates grew in the 1980s and has remained high since — making postsecondary education important for economic wellbeing and mobility. The gap in earnings between high school and college graduates implies that if the alternative to borrowing for college is not only forgoing borrowing but also forgoing a college education, potential borrowers may be worse off without access to loans. Higher education also has much higher returns than many other investments, such as housing or stocks. If, on net, student loans tend to lead to increased educational attainment and, as a result to higher-paying jobs, student loans may actually have an overall positive effect on borrowers’ economic well-being and ability to meet financial obligations and bolster economic growth.

- Federal student loan limits constrain how much many students can borrow. Studying changes in outcomes of these constrained students when loan limits increase can provide evidence on the impact of allowing students to borrow more on their lives and financial outcomes. Our recent research provides the first evidence on the short‐ and long‐run effects of increased student loan limits for a broad population. Specifically, we examine the effects of loan limit‐driven increases in student borrowing —holding constant changes in college prices, grant aid, and other sources of financing for college — on students’ educational attainment, earnings, and financial well-being. We use two sources of administrative data. The first includes education and earnings records for students who entered a public, four-year higher education institution in Texas between 2000-01 and 2007-08, which allows us to measure effects of student borrowing on educational attainment and earnings outcomes. Among states, Texas provides a near‐ideal setting to study the effects of student loans because of the large size of the higher‐education sector, the diversity of its institutions of higher education, and similarities in student and school characteristics to national averages. The second dataset includes the credit records of a large, nationally representative sample of young student borrowers who first borrowed for college between 2003-04 and 2007-08. We use this data to provide insight into student loan repayment behaviors, access to and management of other sources of debt, and home purchases.

- Increasing borrowing limits leads to more borrowing. Federal undergraduate loan limits vary by academic level and are set by Congress. The most recent increases in federal undergraduate loan limits occurred in academic years 2007-08 and 2008-09. These increases resulted in variation in the maximum amount a student could borrow depending on when they started college. Comparing students in different cohorts based on how constrained they were at entry allows us to estimate the impact of higher limits. We find that access to additional student loans substantially increases borrowing, holding constant all other factors, including tuition costs and grants.

- Loan limit increases led to a lasting increase in graduation rather than simply a retiming of degree receipt. A major concern about student debt is its burden on students who never graduate from college. One might expect that borrowing more money simply allows students to graduate more quickly but does not alter a student’s likelihood of graduating overall. However, among the borrowers who first enroll in a four-year public college or university in Texas, higher federal loan limits increased the probability of earning a degree within six years by around 5 percentage points. This represents a 10 percent increase compared to the average graduation rate of 48 percent for all borrowers who attend four-year public institutions in Texas during this period. In short, students who would have been constrained by the previous (lower) loan limits are more likely to graduate when they can borrow more.

- Increased access to student loans for these students means they do not have to rely on other types of financing for college, like credit cards, and also do not have to work as much while in college. Access to additional student loans reduces four-year public college students’ reliance on credit cards, which tend to have substantially higher interest rates and fees than student loans. These students are also significantly less likely to have any earnings in their first two years of college, suggesting that additional student loans may allow them to spend less time working while enrolled. Less time spent in paid employment likely allows students more time studying and may partially explain why they are more likely to graduate. Taken together, the reduction in the reliance on credit cards and the lower need for earnings from employment indicates that greater student loan availability reduces students’ reliance on other—often more costly—sources of funding for school.

- Higher loan limits increase annual earnings for students after they leave college. This likely occurs because these students graduated at higher rates. The increase in earnings is substantial, ranging from four to six percent six to eight years after college entry.

- Although higher loan limits lead students to accumulate more debt, these students are less likely to default on their loans. Effects of higher loan limits range from an 18 percent reduction in default rates four years after these students likely started college, to a 10 percent reduction eight years later. The finding that borrowing reduces student loan delinquency and default would appear to be counterintuitive unless one also takes into account the effects of borrowing on college completion and subsequent earnings. In other words, the significant reductions in defaults suggest that even with higher student debt, increased earnings offsets increased student loan payment burdens.

- Students who borrow more when the loan limit is higher experience no detrimental effects on their ability to repay other loans or reductions in having a mortgage or auto loan. Although increased student debt could make it less desirable or harder to access or repay other types of debt, our findings do not support these possibilities. In particular, the lack of an effect on homeownership stands in contrast to concerns raised in recent years by policymakers and the popular press that rising student debt was making it difficult for young adults to become homeowners. Holding constant tuition costs and other sources of aid, increased student borrowing has no effect on constrained students’ homeownership.

What this Means:

Despite concerns that students are “overborrowing,” our findings are more consistent with some students being constrained by federal loan limits and therefore underborrowing for college. Altogether, an additional dollar of student loan debt can, on net, improve educational attainment, earnings, and financial well‐being for these traditional-aged students. These findings directly inform policy debates concerning future changes in federal loan limits, particularly for dependent students at four-year colleges that are the focus of our study. Raising federal borrowing limits for such students would likely increase their future earnings and improve their credit market outcomes. However, it is important to note that data limitations prevent us from testing whether older, non-traditional students experience similar benefits.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.