Is the Rise in U.S. Corporate Debt Cause for Concern?

Brandeis University

The Issue:

Corporate debt has been growing at a rapid pace since the recovery from the Great Recession, and the total value of nonfinancial corporate debt in the United States now stands at or near all-time highs. This has been the source of some concern since excessive debt can lead companies to face financial distress, and this distress could spread to the larger economy. People are especially sensitive to this because of the role debt played in past crises, such as the financial crisis that peaked in the autumn of 2008. There is also concern because loans account for a large proportion of corporate debt. Unlike bonds, whose terms are relatively transparent and therefore have risks that can be more readily gauged, loans are private contracts between two parties and their terms and risks may be less well understood. Should the growth of debt, or its composition, be a source of concern?

It is important to pay attention not just to the amount of debt, but also different facets of its composition.

The Facts:

- Companies have a variety of ways to finance their operations, including using their own earnings, issuing new equity, issuing bonds, or taking out loans. The composition of financing options that a company chooses matters, particularly during economic downturns. Unlike with equities, where the dividends paid to investors will vary with the company’s fortunes, loans and bonds promise creditors a pre-specified payment that does not generally depend on the borrower’s fortunes unless there is a default. For this reason, a firm that has issued equity will not experience the same level of financial distress in a downturn as firms that have financed their operations with debt will since the dividend payments to equity holders can vary while bond and loan repayments cannot.

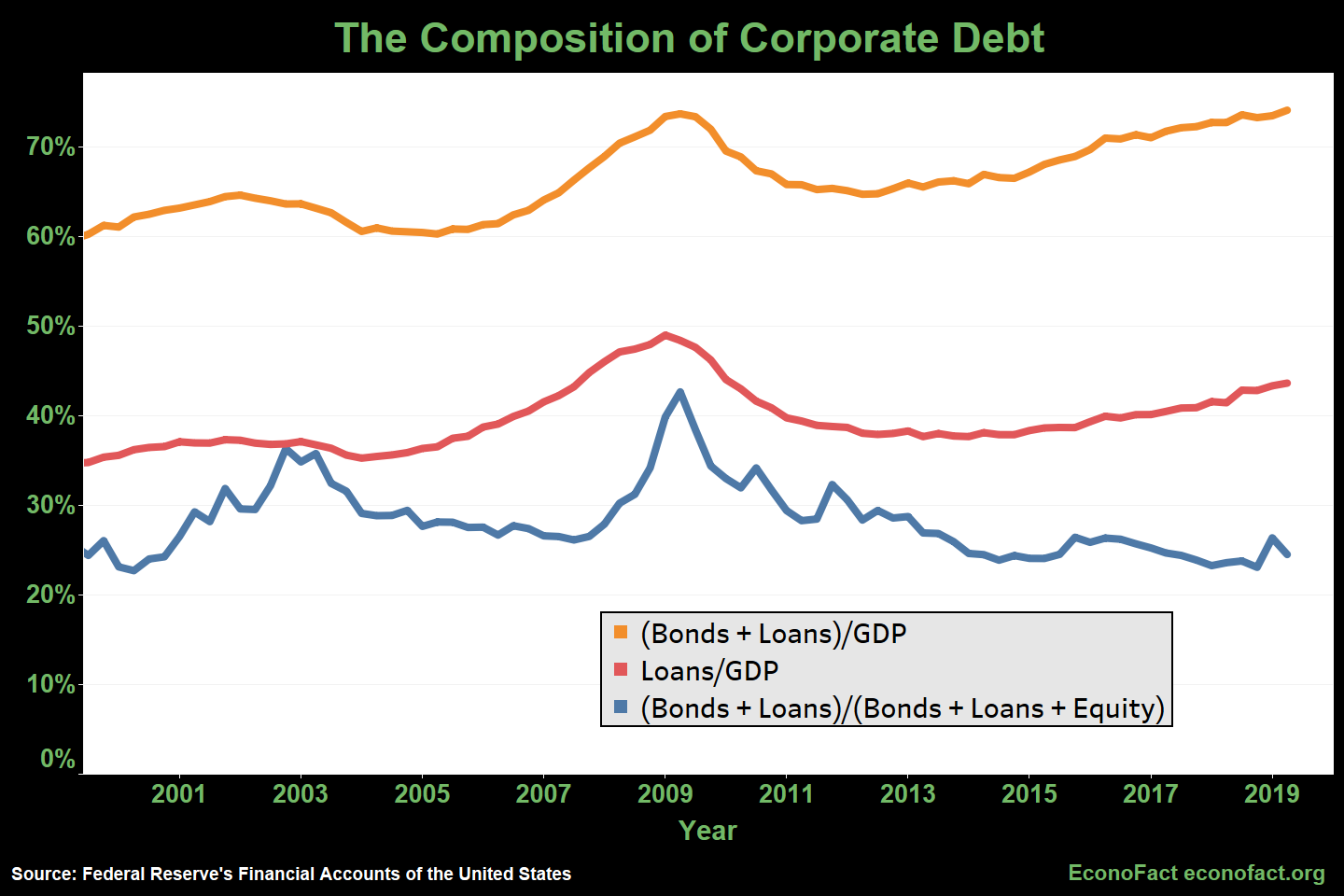

- One major reason why the value of corporate debt is at all-time highs is just that the economy has grown over time. The economy’s output, as measured by Gross Domestic Product (GDP) is about 50 percent higher than it was immediately in the wake of the 2008 financial crisis. Whether recent trends in debt appear unusual depends critically on how the value of debt is scaled. Both the absolute amount of nonfinancial corporate debt and corporate debt as a share of GDP have risen since the financial crisis, rising from 65 percent of GDP in 2013 to 74 percent of GDP in the most recently available data, close to levels that prevailed just before the crisis. But this growth in debt over time appears also to reflect growing firm profits and firm values. With corporate earnings remaining strong and with equity market capitalizations growing faster than the amount of debt outstanding, aggregate debt burdens scaled relative to the market value of corporate equity or as a share of corporate profits or cash flow are currently not particularly high in the United States. Moreover, the degree to which companies are relying on debt and bonds to finance their operations versus equity has actually been declining. Corporate debt as a share of the total financing mix, measured using the market values of these financial instruments, appears to be falling over time, with a slight uptick in the past several quarters that is dwarfed by the longer-horizon decline (see chart). Debt as a share of the total financing mix was over 50 percent from the 1970s to the early 1990s but is under 25 percent today.

- Despite what appears to be a benign situation with respect to the level of debt (as compared to the total value of firms), there is concern with the form debt is taking. Lenders who offer loans typically protect their interests with “covenants” which tie borrowers’ hands and – when well-designed – can reduce a lender’s risk. A standard example of a covenant might be a requirement that a borrower maintain a particular ratio of earnings to required interest payments, and a covenant like this would prevent a borrower from taking on additional and potentially unmanageable debts. In part because loans are privately-negotiated contracts, unambiguous measures and public data on the “quality” of covenants are less readily available than data on raw debt amounts. Credit rating agencies do, however, closely follow covenants on the loans that they rate. The Moody’s rating agency has been measuring and recently publishing commentary about deteriorating covenant quality in the highest-risk parts of the corporate loan market. A trend that points toward willingness on the parts of at least some investors to accept minimal covenant protection when they lend to corporate borrowers. Given the protective role that covenants play for investors, this pattern is worth continuing to watch and highlights the importance of paying attention not to just the amount of debt but also different facets of its composition.

- There is also concern that some debt may not be financing productive investment. There is evidence that a large share of the borrowing that companies are currently doing is not being used to invest in growing their own productive capacity. The use of funds raised through debt for both acquisitions and stock buybacks are each currently about four times larger than the use of funds for purchasing capital expenditures or for intangible assets, according to this research note by the Federal Reserve Bank of New York. Using loans or bonds to finance capital expenditures and intangible assets like ownership of intellectual property can help companies grow in the future. In contrast, stock buybacks—which are used to return wealth to stockholders — have a less-direct benefit for the future prospects of a company (although, as I discuss here, one company’s stock buyback can free up funds that enable investment in other companies).

- While interest rates are currently low by historical standards, firms that depend upon rolling over short-term debt may face challenges if interest rates were to rise. Interest rates are currently low, and there is even the somewhat unusual inversion of the yield curve, where some longer-maturity rates are lower than otherwise comparable shorter-maturity rates (a situation that some see as portending a downturn). An increase in interest rates will raise the debt burden for companies that have to issue new bonds, and, if a recession does, in fact, materialize, this debt will be all the more burdensome because of the weakness of the economy. So-called leveraged loans that have variable interest rates that can rise as other interest rates rise also pose a risk for companies that may face larger debt repayment costs.

- The pattern of those who hold debt may also matter for overall financial stability. The average leverage (amount of borrowing relative to the earnings of a firm) for the economy as a whole can mask very different levels of leveraging across firms – as pointed out by the FRBNY research note, a 50 percent average leverage rate can imply either all firms have this rate or half the firms are not at all leveraged while the other half have 100 percent leverage – two situations that differ quite a bit in their implications for overall financial stability. Financial instability can also arise through the channel of those who make loans. If loans are held by investors and institutions that are themselves highly levered (that is, that have a lot of borrowing relative to their assets), this can cause a cascading of financial failures. This was an important source of the crisis in 2008 when highly-levered structured investment vehicles held investments that failed, leading to cascading problems and systemic instability. Federal Reserve Board chairman Jay Powell has noted this in recent remarks, but he also noted that the structured investment vehicles in use today are sounder than those that were in use before the mortgage credit crisis.

What this Means:

The amount of corporate debt has been growing since the recovery from the Great Recession, but this aggregate growth in the amount of debt appears mostly consistent with the robust growth in corporate profits. Debt as a share of the total firm financing mix is much lower today than it was during the 1980s and early 1990s. The mix of debt tilts in the direction of loans versus publicly-traded bonds, and because well-crafted covenants are an important tool for protecting against loss, it is important to continue to pay attention to changes in covenant quality over time. Finally, rising interest rates could quickly erode the profitability of firms that have borrowed at floating rates or using short-term debt.