SWIFT Sanction on Russia: How It Works and Likely Impacts

Johns Hopkins Carey Business School

The Issue:

The United States and the European Union moved quickly to impose economic sanctions against Russia and selected state-owned financial institutions following Russia’s February 21 invasion of Ukraine. One of the harshest measures promised to date was to remove select Russian banks from SWIFT, the Society for Worldwide Interbank Financial Telecommunication, a secure financial messaging service used to execute international transactions among banks. This sanction, one of the strongest financial penalties in the arsenal, will inflict tremendous damage to the Russian economy, at least temporarily, at manageable cost for the United States and its allies.

Banning Russian banks from the financial messaging system freezes their ability to transact with the rest of the world, imposing high costs.

The Facts:

- SWIFT provides secure financial messaging services for the execution of financial transactions and payments across borders. SWIFT is the leading method for the provision of financial messaging. It is member owned — neither the United States nor the European Union controls SWIFT directly, but each can exert influence on its governing body that is subject to Belgian law. Within the SWIFT network, the 11,000 member banks communicate with each other through a standard language — the SWIFT message. These SWIFT messages are used to initiate and execute transactions with unique bank identifiers called SWIFT codes. SWIFT itself does not settle payments, but it permits transaction-related communications from one bank to another that would otherwise have to go through error-prone emails or telex. SWIFT handles about 10 billion messages a year. The vast majority of any individual or corporate international transactions settled among banks relies on the SWIFT messaging system.

- SWIFT-related sanctions were imposed on Russian banks. On February 26th, the United States, the European Commission, the United Kingdom and Canada announced a commitment to ensure that selected Russian banks are removed from the SWIFT messaging system or have their access restricted to permitted transactions. On March 2, the European Union detailed that seven Russian banks would be excluded from the SWIFT messaging system in an action that would take effect March 12 and was coordinated with its international partners including the U.S. and the United Kingdom. Moreover, depending on Russia's actions, the Commission is prepared to add further Russian banks at short notice, thereby raising the uncertainty as to the future access to SWIFT of all other Russian banks.

- Banning a bank from SWIFT freezes, at least temporarily, its ability to transact with the rest of the world. It technically impedes the excluded bank from executing its and its customers’ financial transactions with foreigners, meeting obligations, receiving payment for exports, or providing short-term credit for imports. This can paralyze all sectors of the economy engaged in international trade and finance. Even a selective ban on Russian banks as the one enacted would have a major immediate economic impact on the Russian economy and its businesses. Indeed, reactions to the SWIFT announcement, combined with the actual freezing of the Russian Central Bank foreign assets on February 28, were immediate and attest to the severity of the penalties imposed. The ruble tumbled about 30 percent, the central bank doubled interest rates to 20 percent and imposed controls on payments abroad.

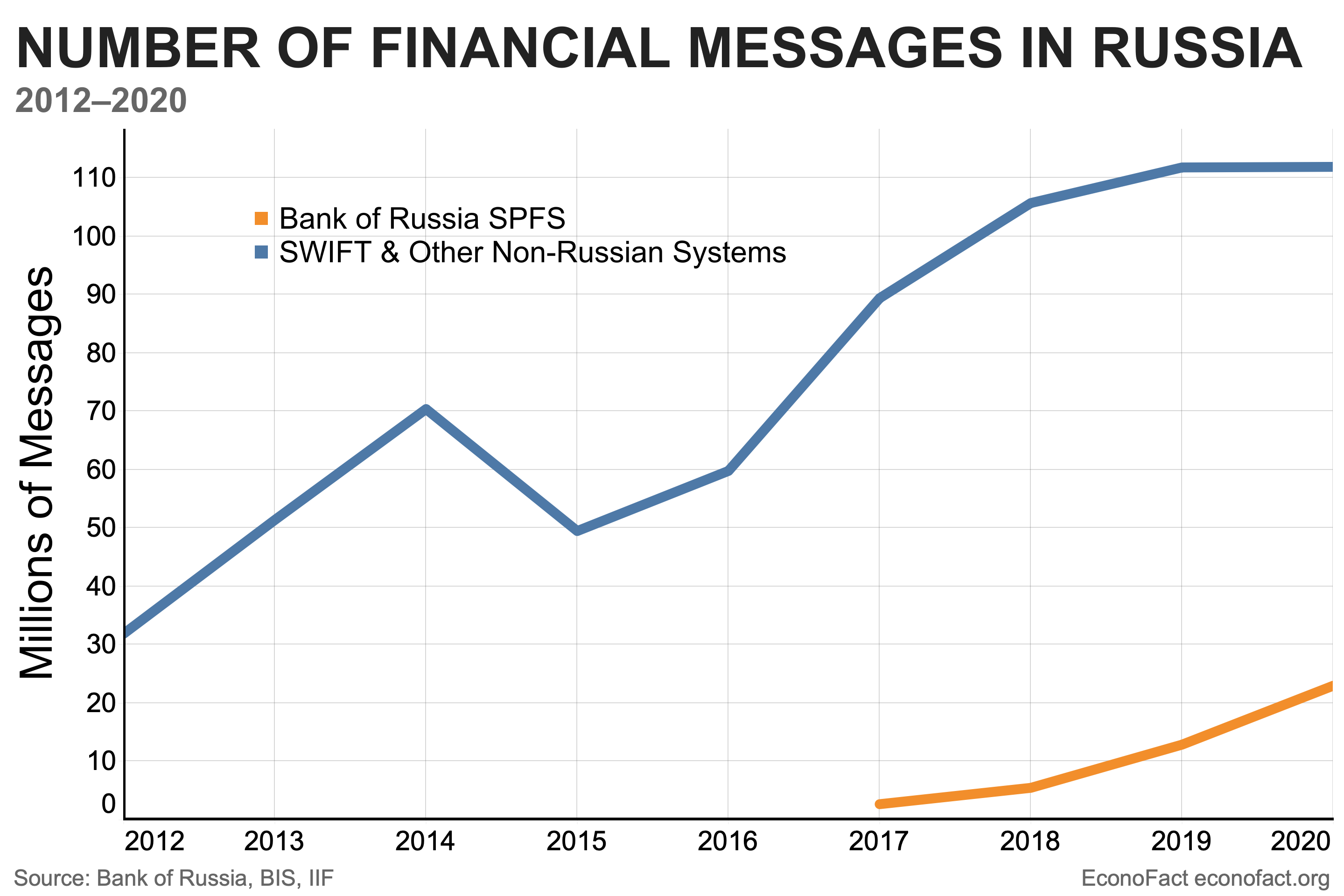

- Russia’s domestic payment system could also be disrupted to the extent that all transactions with any card issued by the major credit card networks (VISA, Mastercard, Amex, etc.) all operate through SWIFT. Russia has already developed its own transaction system known as the System for Transfer of Financial Messages (SPFS), currently used only for domestic transactions. SPFS was created after the United States attempted to impose a similar ban from SWIFT following Russia’s annexation of Crimea in 2014. The Institute of International Finance (IIF), however, estimates that only 20-25% of the domestic messaging and card transactions within Russia currently take place outside SWIFT (see chart). In addition, Russian citizens would find traveling abroad much more cumbersome without access to credit cards.

- The Russian public reacted to the sanctions with a run on banks. Amid fears that they may not be able to use credit cards for day-to-day purchases, Russian citizens dashed to the ATMs for rubles and dollars, and tried to buy durable goods on the shelves to protect their savings and purchasing power from the sanctions. People withdrew close to a trillion Rubles (representing 6.5% of the monetary base) when the SWIFT sanctions were announced – and this followed an even larger withdrawal on Friday, February 25th in response to other sanctions. The last time Russia witnessed such a large financial disruption was in 1998 when it defaulted on its foreign debt and plunged its domestic financial system into a deep crisis.

- The sanctions pose risks for those countries that have imposed them and the broader global economy. Disruptions to Russia's financial system could disrupt the energy supply to Europe, as well as commodity exports to global markets, triggering further increases in energy and food prices that were already elevated due to COVID-19, supply shortages, adverse weather shocks, and supply chain disruptions. The SWIFT sanctions, as well as other actions, could contribute to a default on Russian obligations abroad that could have repercussions on the foreign creditors and bring about a liquidity shock to the U.S. or European interbank market since Russian entities owe more the $100 billion next year alone according to market and IMF estimates. Large American and European corporations that are rushing to liquidate their stakes in Russian operations, as already announced by oil giants BP, Shell, and Exxon, would incur further losses on their holdings that may ultimately have to be written off. Indeed, dollar shortages in the global interbank market started to surface on Monday, February 28th, as American and other foreign counterparts to targeted Russian financial institutions rushed to cover their exposures. These repercussions are one reason why the SWIFT ban, like other U.S. financial sanctions already enacted, has been implemented in a selective manner.

- Excluding Russian banks from SWIFT, which has been called the “nuclear option,” risks permanent damage to international financial integration and the U.S. dollar hegemony. The success and efficiency of a payment network depends on its widespread adoption and use of its services. When lighter SWIFT sanctions were applied to Russia in 2014, the country was quick to develop its own messaging network to support the domestic payment system. Russia also changed the composition of its foreign reserves away from the U.S. dollar and strengthened ties with the Chinese Cross-Border Interbank Payment System (CIPS), which can settle international claims in yuan. Independently, China developed its own parallel international messaging system over the past few years as a precautionary measure against the increased likelihood of U.S.-imposed financial sanctions. Even the European Union, at the time of the breakdown of the Iran nuclear deal in 2018, started to develop its own financial messaging system, the Instrument in Support of Trade Exchanges (INSTEX), to avoid getting trapped in the web of U.S.-imposed sanctions on Iran. The ban from SWIFT could also encourage greater use of cryptocurrencies to evade financial sanctions, as reflected in their unusual appreciation amidst global turbulence on Monday, February 28. Nonetheless, the experience of the past several years suggests these concerns are overstated as the U.S. dollar remains the pillar of the international financial system.

What this Means:

North Korea and Iran have long been cut off from SWIFT, as has Venezuela since 2019. Russia’s economy is more complex and sophisticated than these countries, and the financial system is a more integral part of its operation, so the impact of exclusion from SWIFT could have a bigger impact. But countries tend to adapt and find ways around sanctions. Nonetheless, the short-term economic impact of even a partial, but extendable, ban from SWIFT on the targeted country, and the willingness by countries imposing the sanctions to bear some economic costs, sends a strong signal that can have a sharp economic cost to Russia.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.