The Strong Dollar and the War in Ukraine

Fletcher School, Tufts University

The Issue:

The dollar has strengthened over the past year, with the most rapid rate of increase occurring since the Russian invasion of Ukraine. The DXY index, a weighted average of the dollar's value against six major currencies, reached a 20 year high in mid-May, having appreciated by 9 percent since February 24th. Many economists are predicting the dollar will reach parity with the euro by the end of the year, a value not seen since 2002. How has the war in Ukraine contributed to a stronger dollar, and what are the consequences of this appreciation?

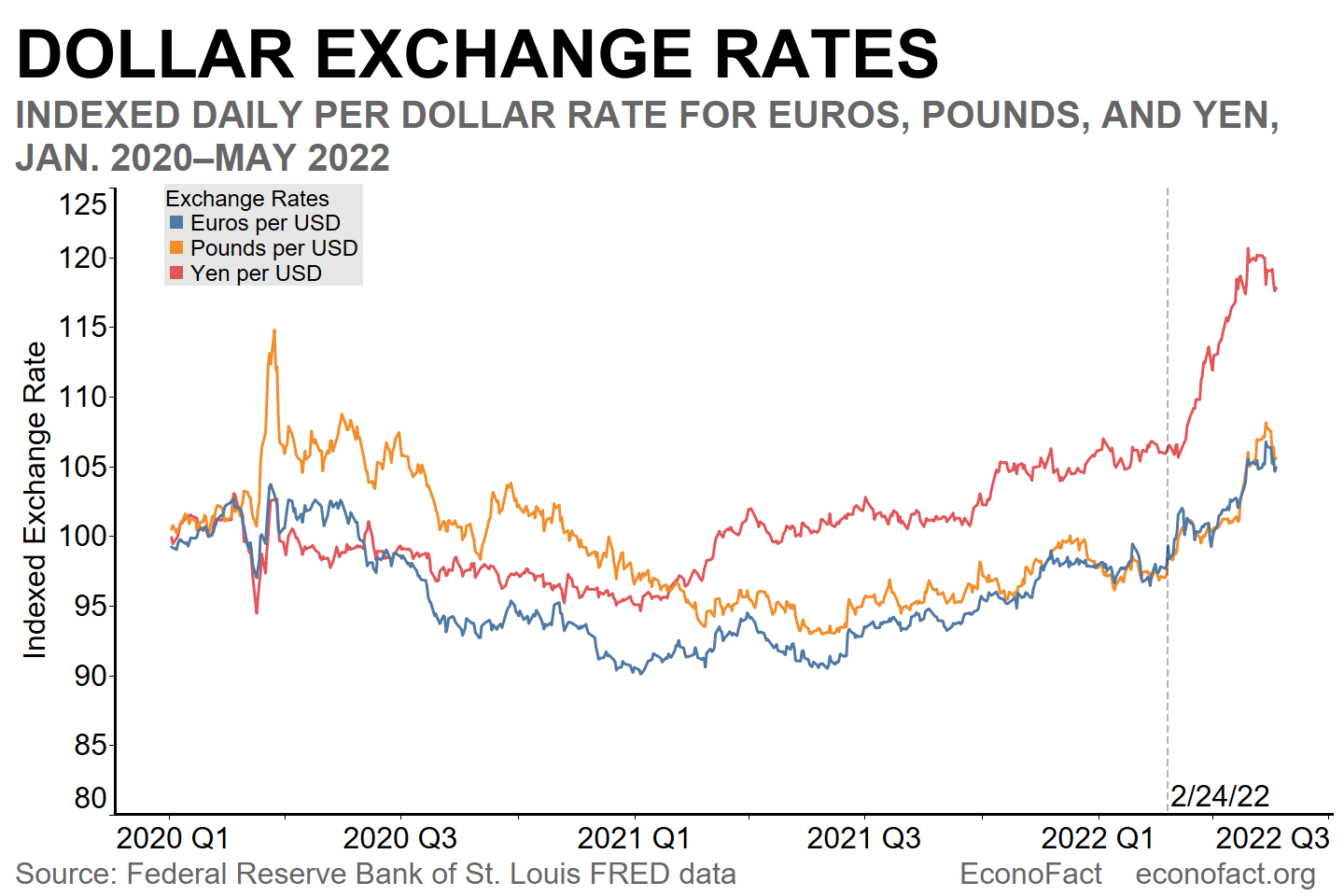

The dollar's value against six major currencies reached a 20 year high in mid-May.

The Facts:

- Over the past year, the dollar rose by 12 percent against the euro, 9 percent against the pound, and 16 percent against the yen. During the first year of the pandemic the dollar weakened with respect to the euro, the pound, and the yen (represented by lower values of the indexes). But the trend reversed in 2021 and the appreciation of the dollar with respect to these currencies gained steam after the Russian invasion of Ukraine on February 24, 2022. Just in the three months between the start of the invasion and the end of May, 2021, the dollar appreciated by 7.0 percent against the British pound, 5.6 percent against the Euro and 10.8 percent against the Japanese Yen (see chart). To put this in context, these three-month changes would result in annual rates of appreciation of 31 percent, 25 percent, and 50 percent, respectively, were they to continue for an entire year.

- Exchange rates reflect the relative demand for countries' assets and respond to both current economic conditions and expectations of future conditions. The attractiveness of any financial asset is linked to its expected future payout, its reliability, and the ease with which it can be bought or sold. An increase in the demand for a country's assets raises demand for that country's currency, which is needed to purchase those assets, causing that country's currency to appreciate (strengthen). An increase in the interest rates offered by a country's bonds, or the expected future return from a country's equities, increases the demand for that country's currency which leads to an appreciation. Likewise, a country's currency will appreciate if the demand for its assets increases because of a perception that those assets offer a "safe harbor" at times of heightened uncertainty. As a result, today's value of the exchange rate reflects investors' views of the future as well as current economic conditions.

- One reason for the strong dollar is that United States assets are seen as a safe haven. United States assets, especially Treasury bonds, are viewed as retaining value at times of market turbulence and are also valued because the markets for these assets are deep and reliable. This typically leads to a dollar appreciation at times of global turbulence as demand for these assets rises. The strengthening of the dollar in the wake of the invasion of Ukraine offers one example of this, but there are others as well. Perhaps most strikingly, the DXY dollar index appreciated by more than 10 percent in the two months after the onset of the Global Financial Crisis in September 2008 despite the fact that the crisis began with a seizing up of financial markets in the United States.

- Another reason for the run-up in the dollar is the perception that the war will have relatively less adverse effects on the U.S. economy as compared to those of the Euro area, the United Kingdom and Japan. While the increase in energy and food prices from the Russian invasion of Ukraine is expected to have detrimental effects throughout the world, Europe (including the United Kingdom) and Japan are expected to be harder hit than the United States. A relatively stronger economy in the United States increases the demand for U.S. assets, since these will be less adversely affected than assets from other countries, leading to a stronger dollar. An IMF blog from March 2022 lays out some reasons; Russia is a critical source of natural gas for Europe, the Japanese economy is relatively more vulnerable than the United States to higher commodity prices and weakening demand in its export markets, and the United States has few direct ties to Ukraine and Russia. The lower relative vulnerability of U.S. economy to the war in Ukraine is also reflected in revisions to forecasts in GDP growth. The Wall Street Journal's consensus forecast of 2022 Q4/Q4 growth was revised down from 3.3% in the January survey to 2.6% in the April survey. This 0.7 percentage point decline is smaller than the revision in growth rates for the Euro area, the United Kingdom and Japan; the European Commission revised its forecast for real GDP growth in 2022 from 4.0% in its Winter 2022 report to 2.7% in its Spring report, Price Waterhouse Coopers (PWC) revised its expectation of 2022 British economic growth from 4.5 percent to a range between 2.8 percent to 3.8 percent, and the International Monetary Fund lowered its forecast for Japan's economic growth for 2022 from 3.3 percent to 2.4 percent.

- The dollar's strength is also a result of the more aggressive response to higher inflation by the Federal Reserve as compared to the Bank of Japan, the European Central Bank and the Bank of England. Increased commodity and fuel prices due to the war in Ukraine have contributed to the higher inflation that had started as economies recovered from the initial pandemic lockdowns. Central banks combat higher inflation by raising interest rates which contributes to an appreciation of their currency. The Federal Funds Rate has risen from 0.08 percent in February to a current range between 0.75 percent and 1 percent. The Federal Reserve raised its target rate in each of its last two meetings with the 50 basis point rise in May 2022 being the biggest one-time increase since 2000. And, the expectation is that such increases are likely to continue. After the May 4th Meeting, Chairman Jerome Powell stated that "There is a broad sense on the committee that additional 50 basis point increases should be on the table at the next couple of meetings." In contrast, the British Bank Rate has risen 50 basis points since February but the Monetary Policy Committee seemed to temper its willingness to continue to aggressively raise interest rates in its May 5th, 2022 meeting amid concerns about a slowing British economy. European Central Bank President Christine Lagarde had stated, up until May, that the ECB would not start raising interest rates until July and that any further increases would be gradual. But facing rising inflation, she indicated in late May that the European Central Bank would raise interest rates from negative values, where they had been for eight years, to zero by the end of September and could continue raising rates after that, which strengthened the euro to its highest level for a month against the dollar. At the end of May, the Governor of the Bank of Japan, Haruhiko Kuroda, told a parliamentary committee that because the Japanese economy was still recovering from the pandemic, the Bank of Japan would “patiently continuing powerful monetary easing.”

- What does the appreciation of the dollar mean for U.S. consumers and U.S. producers? The exchange rate translates the price of goods denominated in one currency to a price in another country's currency. The strong dollar raises the price of U.S. goods abroad, which puts downward pressure on U.S. exports. At the same time, a stronger dollar lowers the price of imported goods in the United States, raising imports. In fact, the United States trade deficit hit a record $109.8 billion in March 2022, up more than 20 percent from its February value. While the strength of the dollar over the past year plays a role in this figure, it is important to note that there is not an immediate link between the exchange rate and the trade deficit. The exchange rate is one factor affecting the relative prices of goods across countries, but higher inflation in a country than its trading partners will also raise the relative price of its goods. Furthermore, because international trade contracts are signed months before delivery, exchange rate changes take time to feed through to the trade account. Finally, imports and exports depend on factors other than the exchange rate, such as the growth in the income of the domestic economy (for imports) or in the income of trading partners (for exports). Thus, while the recent strong run-up of the dollar may contribute to future trade deficits, the March figure is not likely directly linked to the immediate appreciation of the dollar after the invasion of Ukraine.

- The strong dollar has a range of effects on economies across the globe. Commodities like oil and wheat are priced in dollars. The effect of an increase in the dollar price of these commodities is exacerbated for countries that have had their currencies fall in value against the dollar. Low-income countries and emerging markets will be particularly hard hit by a strong dollar. Along with higher food and fuel prices, many of these countries have borrowed in dollars and paying back these loans becomes more expensive as the dollar strengthens. Mohammed El-Erian, former Chief Economist of Pimco, wrote in the Financial Times "For most [low-income countries], dollar appreciation translates into higher import prices, more costly external debt servicing and greater risk of financial instability. It puts further pressure on countries that already stretched in resources and policy responses by the fight against the ravages of Covid of their dollar-denominated debt."

What this Means:

Along with the more obvious economic effects of the Russian invasion of Ukraine, such as on energy prices and the prices of foods, there has also been a strengthening of the dollar. There have not yet been calls for government efforts to weaken the dollar, perhaps because these efforts often prove futile and represent an example of "the tail wagging the dog" in which the main variables of concern, like inflation and growth, are sidelined. Nonetheless, the dollar's strength will have important consequences.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.