The Rising Burden of Elder Care in the United States

EconoFact

The Issue:

The rising burden of eldercare is a major strain in all wealthy countries, including the United States. Around one in four Americans aged 65 or over needs long-term care to assist with everyday activities. This eldercare can put a heavy time and psychological burden on close family and friends, while those with severe needs typically face a heavy financial burden to pay for care services, whether provided at home or in an institutional setting. Federal and state governments provide some financial support, particularly through Medicaid, but public funding is quite tightly constrained relative to peer countries, and the cost of long-term care is a major source of poverty for older people. Poor quality and lack of availability of eldercare also mean older people are less healthy and have greater medical needs. Moreover, these strains will only grow as the US population continues to age and the costs of providing eldercare are likely to escalate, especially if the supply of immigrant care workers is curtailed.

Around 1 in 4 Americans aged 65 and over need help with activities of daily life.

The Facts:

- Many elderly people need long-term help with daily activities such as getting dressed, using the bathroom, eating, and getting in and out of bed, as well as with other instrumental activities such as cooking, taking medications, and grocery shopping. About 29 percent of people 65 and over in the United States report at least some limitation with their ability to conduct daily activities in the Health and Retirement Study. Difficulty with these tasks increases with age: the share of those reporting at least some difficulty rises to 60 percent for those 85 and older.

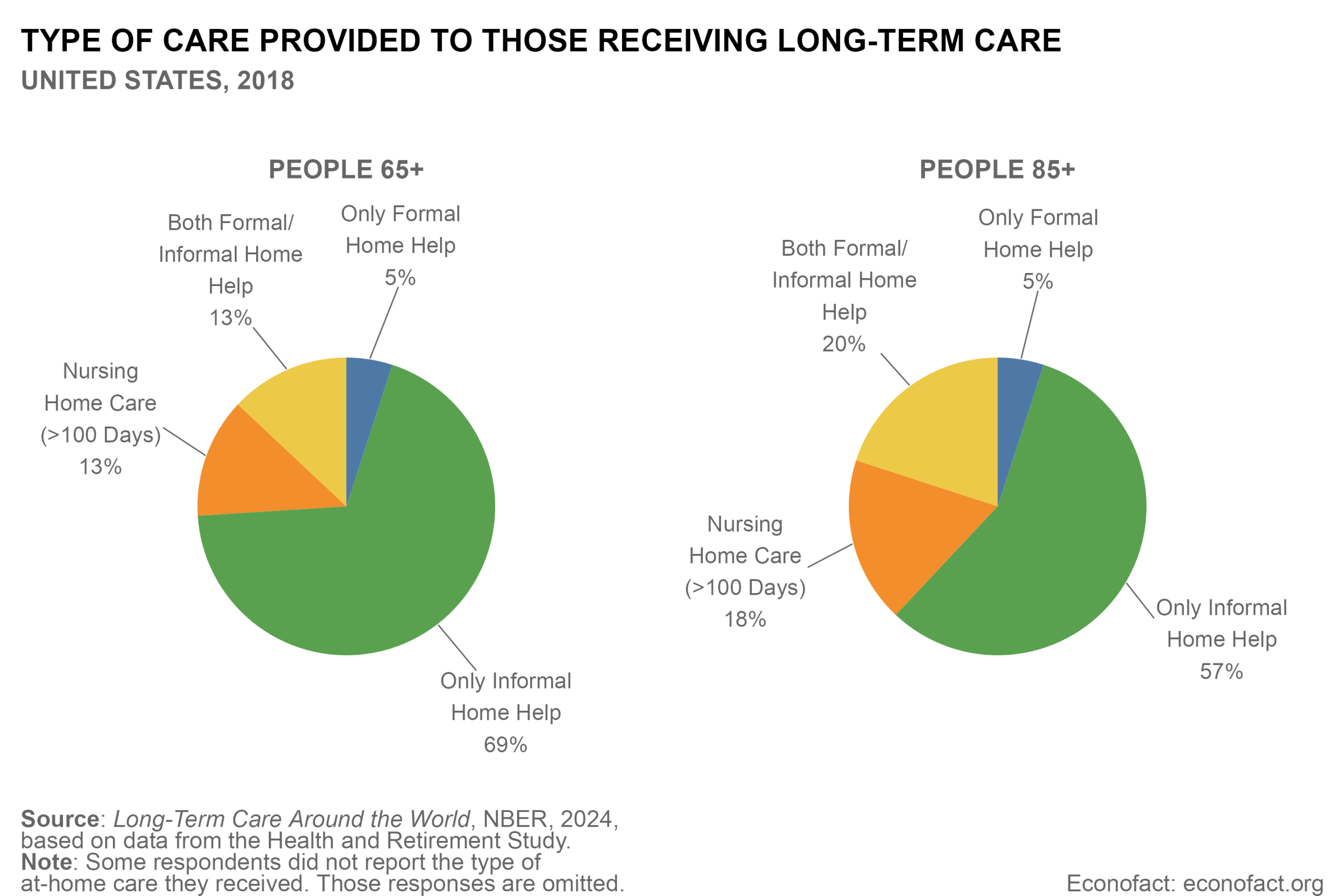

- The majority of elderly persons receiving long-term care receive unpaid, informal care at home; smaller shares receive formal care by paid caregivers at home or in institutional settings such as nursing homes. Around 17 percent of people 65 and over reported receiving some sort of care in 2018 in the Health and Retirement Study. Of those, 69 percent received only informal care provided at home, mainly by family members (see chart). The share of people receiving care rises to 41 percent among those 85 and over, who are more likely to have multiple limitations and to receive paid in-home care or nursing home care, although the majority still depend mainly on family. But 25 percent of elderly people with long term care needs are not receiving care, which raises risks of needing expensive medical treatment.

- The share of care provided in nursing homes has come down over time. In 2023, long-term care beds in institutions and hospitals amounted to 29 per 1000 people sixty five and over, down from close to 40 beds per 1,000 in 2013. People have typically preferred to remain in their own homes for as long as possible, although those most in need of intensive, round-the-clock care will typically need to be cared for in a nursing home. Public resources have been devoted to making the shift to home care possible, including more public support for paying for home care workers and for community services for the elderly. Formal home care is offered both by specialist care agencies and by independent self-employed care givers hired directly by care recipients. There is limited control over quality of care, both in the nursing home and for paid home care. This was highlighted during the COVID pandemic when nursing home populations had particularly high death rates.

- The formal workforce providing long-term care services to the elderly is poorly paid, faces shortages exacerbated by the COVID pandemic, and relies heavily on immigrant workers. In 2018, there were an estimated 1.9 million care workers providing formal help to those 65 and over, with almost half of these aiding those 85 and over (about 3.7 helpers per 100 people 65 and over and 12.6 per 100 people 85 and older). Employment in the long-term services and supports sector fell sharply in the beginning of the pandemic and remained 4 percent lower in January of 2024 than it was in February of 2020. All 50 states and the District of Columbia reported workforce shortages among home and community based service workers in a 2023 survey, with low pay-rates being one of the difficulties in attracting more workers. Some formal care workers are highly trained and quite well paid, such as licensed practical nurses or registered nurses who may be providing post-surgery care outside the hospital. But the majority of care workers are nursing aides or the equivalent with limited education or training receiving pay close to the poverty line. Immigrants make up a substantial share of the workforce that provides assistance with daily living for the elderly, making up nearly 40 percent of home health aides, 28 percent of personal care aides, and 21 percent of nurse assistants in 2021.

- A much larger group of people provide informal, largely unpaid, care to the elderly. An estimated 10.6 million people, usually family members who have no training in caring for the elderly, were providing long-term support to people 65 and over in 2018 according to the Health and Retirement Study. Three-quarters were over the age of 50, typically children helping parents or spouses helping each other. Indeed, almost 18 percent of the population aged 50 and above provide informal care. These care givers are often heavily burdened, especially when they have to juggle care responsibilities with their own paid work and when care eats into leisure time, implying a reduced work week and often early retirement. A recent study of informal support to aging parents in Europe finds that those who provide such informal care (typically women) reduce their paid working hours, with the economic costs of these reductions adding up to a loss of around 0.4 percent of GDP.

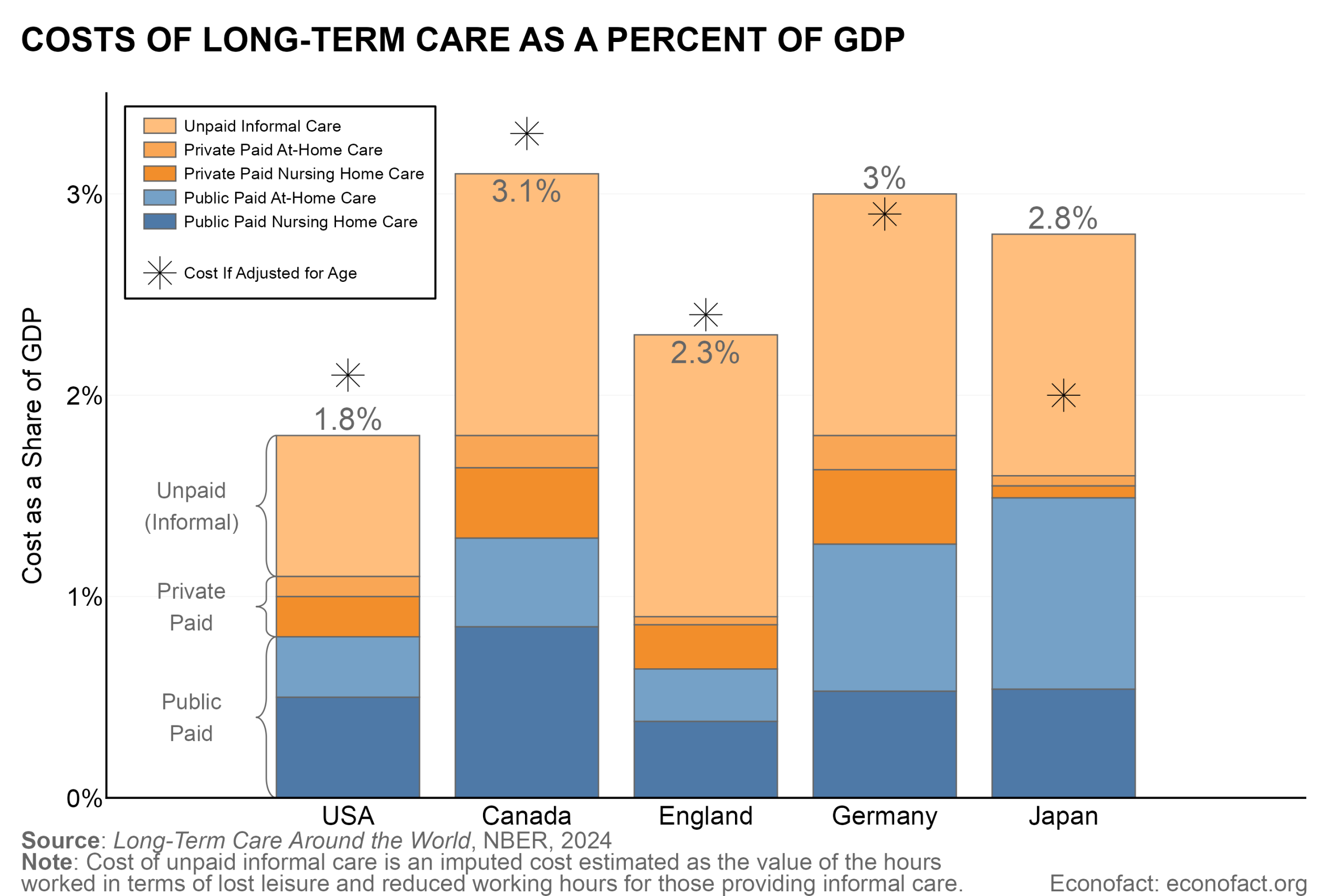

- Public funding for eldercare in the United States is limited. Government support for the costs of long-term care for the elderly is lower as a percentage of GDP in the United States than in most other wealthy countries (see chart). Although part of the difference is due to the relatively younger age profile of the U.S. population, even after adjusting for age composition the U.S. spends considerably less than other peer countries. Total spending on paid long-term care of those 65 and over in the United States amounted to 1.1 percent of GDP in 2023. Around three-quarters of this is from public support and the remainder is largely paid either by private individuals out of pocket or by private insurance. On top of this, one should add the value of the time provided by informal caregivers, which can be estimated as the imputed value of foregone wages and leisure time, estimated by NBER researchers in the range of 0.4 percent to 0.7 percent of GDP depending on assumptions used, giving a total cost of 1.5 to 1.8 percent of GDP.

- Medicaid is the largest public payer of long-term care for the elderly. Medicare, the Federal program for medical care for people 65 and over, provides funding only for acute and post-acute (mainly post-operative) care, both in a nursing home or at home, for up to 100 days. Public funding for longer-term elder care is largely channeled through Medicaid, a means-tested program funded jointly by federal and state governments. Programs are designed and implemented at the state level within broad federal guidelines and are largely restricted to those with very limited income and the most severe needs, usually after running down assets other than the primary residence. Medicaid guarantees nursing home care for those who qualify on health and income grounds, but home and community-based support is not guaranteed. Indeed, there are long waiting lists for many home and community-based services, as waiver programs allow states discretion to offer a wide range of benefits while limiting the number of people who receive them.

- With public funding constrained, many elderly have to devote a high share of income and run down wealth to meet long-term care costs. For those with serious long-term care needs, costs of care are typically very high relative to income levels and public support through Medicaid is only available after personal savings have been largely exhausted. The system of private insurance is very limited, and subject to problems of adverse selection, high costs, and lack of transparency. Only 15 percent of the persons 65 and over have purchased such insurance. Many elderly find that out-of-pocket costs of long-term care after public support absorb a high share of disposable income. OECD estimates suggest that such costs are as much as 60 percent of median income for those with moderate needs and 80 percent for those with severe needs (based on a detailed analysis of California; the figures for Illinois are even higher). As a result, 70 percent of elderly Californian residents with long-term care need to run down wealth to meet long-term care costs and basic living expenses.

- The social and fiscal strains of providing daily care to the elderly will only intensify over time as the US population continues to age. The share of the US population aged 65 and over is projected to rise from 17.7 percent to 22 percent by 2050; the share of those 80 and over will rise from 3.9 to 8.2 percent. While medical improvements and more healthy lifestyles may help to boost elderly health, it still seems likely that the share of the population needing help with moderate-to-severe long-term care needs will increase over the next few decades. At the same time, the availability of government coverage for long-term care is being further constrained as the One Big Beautiful Bill Act of 2025 is estimated to reduce federal spending on Medicaid by close to $1 trillion over a decade, and may leave states with difficult tradeoffs between finding new sources of revenue for long-term care programs or reducing services. Moreover, recent stepped up efforts to restrict immigration to the United States and to repatriate undocumented foreign workers are likely to have a significant negative impact on the availability of long-term care workers, reducing options and raising costs. Going forward, reduced public funding and a more costly and scarce supply of long-term care workers would increase the pressure on informal family support with all that implies in terms of foregone wages and productivity as well as emotional toll. This added pressure would be occurring at the same time as the availability of informal family support is expected to diminish, with fewer children and more single households, and the informal carers age and need care themselves.

What this Means:

With the pressures of eldercare likely to rise as the US population continues to age, what steps can be taken to meet eldercare needs and contain family burdens and poverty risks, within tight budgetary constraints? The gradual shift from care in nursing homes to home care in recent years has probably helped the well-being of older people with less intensive support and medical needs and to contain public spending too, but homecare still requires substantial spending on care workers and places heavy demands on informal carers. A multitude of approaches is likely to be needed, with countries learning from each other’s experience (see for example here and here). Potential areas of attention include: seeking more efficient ways of organizing eldercare at home and in the community rather than institutional settings; promoting healthier lifestyles, including through closer coordination between health and elder care support systems; actions to deepen the long-term care insurance market; steps to ensure adequate supply of paid carers with necessary professional training (which could include easing channels for foreign-born workers); and support for use of new technologies (robots, AI) to improve care and increase productivity.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.