China’s Export Dominance: A Sign of Both Economic Strength and Weakness

22V Research

The Issue:

China finished 2025 with a world record trade surplus of $1.19 trillion. This surplus reflects China’s remarkable dominance as an exporter of manufactured goods. But it is also a result of weak spending by Chinese households, which limits China’s appetite for imports from the rest of the world and increases the Chinese economy’s dependence on foreign buyers for its domestic production. Pushback to China’s surplus from trade partners is rising, highlighted by the Trump administration’s efforts to raise tariffs against China’s exports to the United States. There is also growing acknowledgement within Chinese policy circles that the economy’s reliance on manufacturing investment and exports is politically and economically unsustainable. China’s leadership is targeting stronger household consumption as one goal of its forthcoming Five-Year Plan, but shifting the economy to a more balanced pattern of growth will require a major redirection of policy efforts.

China’s reliance on manufacturing investment and exports is increasingly seen as politically and economically unsustainable.

The Facts:

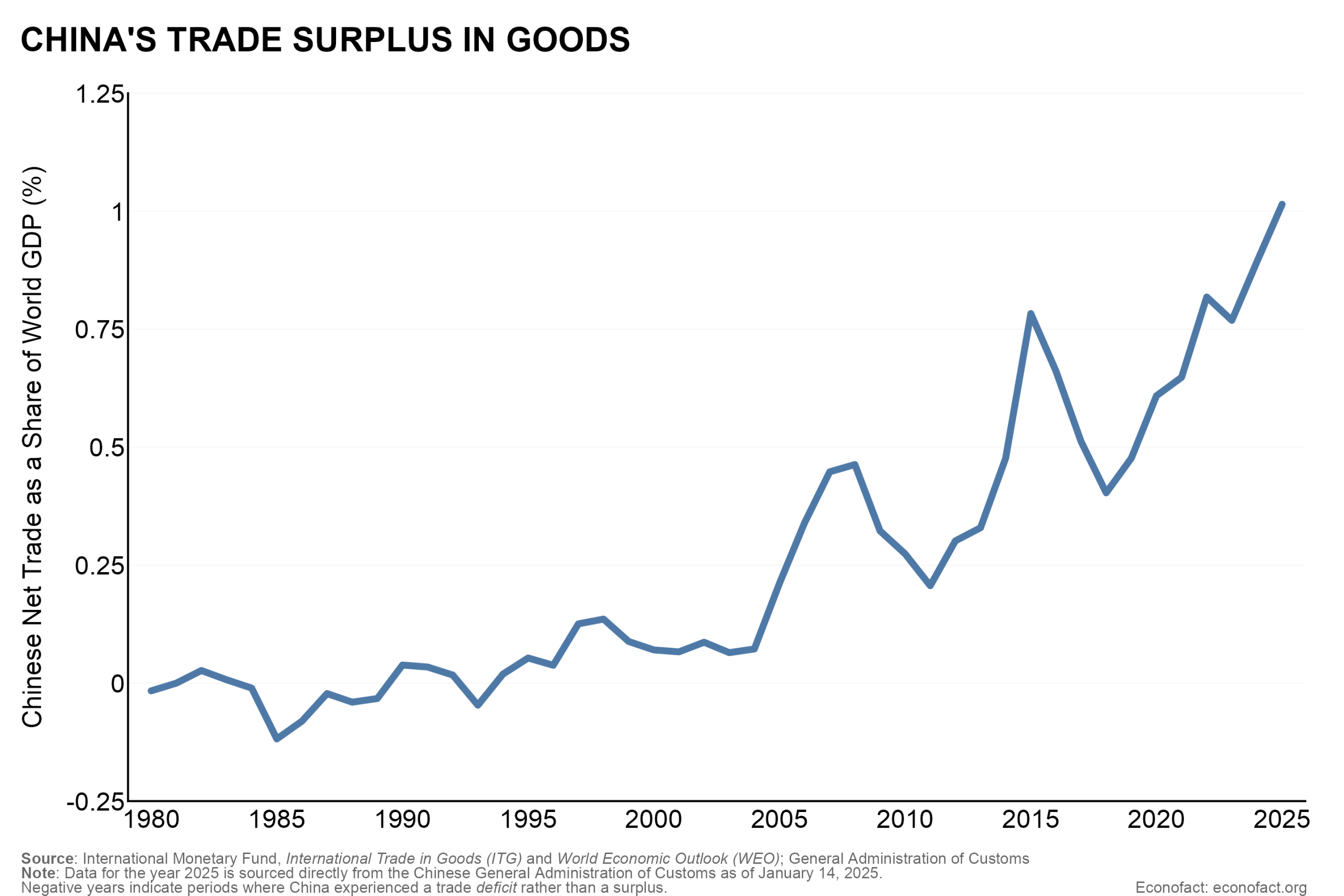

- China’s record trade surplus is driven by its increasingly powerful manufacturing sector, which accounts for around 30% of global manufacturing measured by value-added, a level of dominance unmatched except by the United States in the years after the economic destruction of World War II. The country has consistently had a trade surplus — exporting more than it imports — since the mid-1990s, with exports concentrated in machinery and transport equipment, manufactured goods, textiles, chemicals and food products. In fact, at an estimated 6.13% of GDP in 2025, China’s trade surplus in goods is below its historical peak when measured as a share of China’s economy. However, with China’s increased size, the surplus is at a new peak when measured as a share of the global economy (1.01% in 2025) (see chart).

- China’s prominence as an export giant has been long in the making. In the 1980s, China’s leadership emerged from the chaos of the Mao years with a priority of growing the economy. Beijing followed the path of Japan, South Korea and Taiwan in pursuing a development strategy of mobilizing domestic resources to build a manufacturing sector focused on export markets. Local government officials reinforced the impetus promoting manufacturing investment, using tools such as tax breaks, low-cost bank loans, and subsidized use of state-owned land. Factory activity is easier to tax and to measure for statistical purposes than services, making it attractive for local officials seeking to meet growth targets handed down by leaders in Beijing.

- China’s emergence as “the World’s Workshop” accelerated after the country joined the World Trade Organization in 2001, as China cut its own import tariffs and the United States and other trade partners reduced tariffs on imports from China. Multinational companies shifted production to China, initially to take advantage of low labor costs, and then increasingly to tap high-quality infrastructure and logistics. China’s exports grew an annual average of 30% in 2001-2006 (double the previous rate), and China surpassed Germany to become the world’s largest exporter of goods in 2009.

- In the last ten years, China’s central leadership — and local officials following their political cue — have been particularly focused on high-tech manufacturing. They have used policy preferences and generous financial support to promote industries such as clean energy (electric vehicles, batteries, and solar power), advanced materials, semiconductors, and pharmaceuticals. At the outset, a key goal of this policy push — often referred to as the “Made in China 2025” program that began in 2015 — was to reduce the country’s dependence on imports in strategically important sectors, in many cases with considerable success. China is now largely self-sufficient in the equipment and technologies used in power generation and in rail, and has reduced a high level of import dependency in advanced electronics. The rise in US-China trade and geopolitical tensions since 2016, and growing use of U.S. export controls to deprive China of access to high-tech products such as semiconductors, has reinforced Beijing’s drive to achieve technological self-sufficiency.

- China’s trade surplus has surged again since 2020, as policy choices have compounded the economic effects of the Covid-19 pandemic and a severe real estate downturn. During the Covid-19 pandemic, global demand for goods surged due to restrictions on contact-based consumption of services. China’s manufacturing sector was well-placed to meet this demand, and exports surged. However, China’s own strict containment measures cratered the domestic service sector, a key source of employment. In contrast to many other economies, China’s government provided little in the way of financial support to households to cushion this employment shock. Even in 2025, employment in the service sector — which accounts for 50% more of total labor compensation than does the manufacturing sector — has yet to return to the pre-pandemic trend. The weak labor market has depressed growth in household income and consumption, and in turn China’s demand for imports.

- Next came an unprecedented real estate contraction, initially triggered by a clampdown on risky financial practices by property developers. Housing and related activities, which accounted for as much as 30% of China’s economy at its peak, have contracted sharply since 2021, with no signs of a bottom in sight. To maintain economic growth in the wake of the property sector collapse, China’s central and local governments ramped up support for manufacturing investment. A key tool was to encourage banks, for whom housing had been a key source of demand for loans, to shift their lending to manufacturing firms.

- China’s manufacturing firms — sitting on surplus production capacity and faced with weak demand at home — have turned to foreign markets to generate sales. Since 2020, the volume of China’s exports has increased by 43 percent — well above China’s pre-pandemic trend — while import volumes are up by only 10 percent. China’s exports have surged the most in sectors where domestic demand has been weakest — in particular, consumption goods. China has also been increasingly successful in raising exports in the high-tech sectors, particularly in areas where it is now pushing the technology frontier like solar panels, batteries, electric vehicles, and robotics.

- Many of the policy tools that Chinese central and local governments use to promote exports discourage Chinese imports, especially by constraining growth in household consumption. Examples of these tools include: extended periods of keeping China’s currency undervalued (making imports more expensive for China’s consumers); providing low-cost bank loans to manufacturing firms (which required lowering the rates of return on household bank deposits); and directing government subsidies to industry (which reduces the resources available for spending in areas directly benefitting households, such as social programs).

- Other countries have raised concerns about China’s persistently large trade surplus and its trade practices. While it is natural that individual countries run bilateral trade surpluses or deficits with each other, China’s large total trade surplus means that other countries are correspondingly importing more, an imbalance that puts pressure on their own local producers and strains the global economy. Over the past two decades, imports from China effectively lowered the overall prices of goods in the United States, benefitting consumers, but also contributing to declines in U.S. employment in manufacturing — a “China Shock” that was particularly painful for geographic areas in the United States that depended heavily on employment in industries, such as furniture-making, that were suddenly exposed to competition from low-cost imports from China. More recently, China’s growing prowess in high-tech manufacturing is leading to rising alarm — especially in highly developed economies such as the United States, Germany, and Japan — about a “Second China Shock” that disrupts even highly innovative sectors such as biotechnology and pharmaceuticals.

- While the Trump administration is employing tariffs against China, these are an imperfect tool to rebalance trade with China. Over the course of 2025, President Trump raised the average U.S. tariff rate on imports from China from 21 percent to as high as 127 percent, settling at 48 percent in November after a truce on tit-for-tat trade measures between President Trump and Chinese President Xi Jinping. While those tariffs helped reduce U.S. imports from China by 27 percent and cut the goods trade deficit by 28 percent (measured January through October 2026 compared to the same period in the previous year), they have come with their own costs and shortcomings. First, U.S. exports to China also fell sharply over the same period (by 23 percent) as Beijing launched its own retaliatory trade measures. Second, U.S. tariffs on imports from China and other countries raised costs for U.S. consumers and firms in 2025. Third, some portion of U.S. imports previously sourced directly from China have been re-routed through third countries, such as Vietnam, to avoid tariffs but are still mainly produced in China. Finally, at the global level, Chinese exporters have turned to other markets to sell their goods, contributing to rising trade tensions between China and other trade partners and adding to strains in the global trading system.

- The surge in Chinese manufacturing capacity is also causing rising concerns in China about deflation and brutal price wars. Even with the outlet to foreign markets, China’s manufacturers are showing clear signs of an imbalance between booming supply and weak demand. China’s industrial utilization rate in manufacturing — a measure of how much of production capacity firms are using — peaked in late 2021 at 79% in mid-2021 and has since drifted down to 75%. The share of loss-making industrial firms has increased from 20% in 2019 to 29% in 2024-2025, the highest level in two decades. These trends span a broad range of different sectors, from traditional “smokestack” sectors linked to construction (such as cement), to high-tech sectors that have seen a surge in investment (such as solar panels), to consumer-oriented sectors such as food products. While consumer prices have recently shown a modest rise, China’s economy will finish 2025 with the eleventh straight quarter of broad deflation — the longest for China on record.

What this Means:

The COVID-19 pandemic and a severe real estate downturn have increased the dependence of the Chinese economy on manufacturing exports as an engine of growth — at a time of growing resistance from foreign countries to Chinese imports and stubbornly low capacity to absorb domestic production within China. While China’s leadership is increasingly acknowledging problems associated with excessive manufacturing investment, the policy prescriptions remain modest relative to the scale of the issue. In June 2025, Beijing signaled new efforts to combat “involution,” a term that refers to brutal price wars, especially in sectors with excess capacity. The campaign mostly focuses on disciplining local governments against promoting further investment in sectors at risk of excess capacity, such as by restraining their use of tax incentives. However, the campaign does not acknowledge that efforts to boost domestic demand are also needed. China’s Fifteenth Five-Year Plan, which was previewed in October 2025 and will come out in March 2026 to guide economic policy in 2026-2030, does seem likely to propose incremental and gradual efforts to boost domestic demand and especially household consumption. Yet the principal focus for the plan continues to be to advance China’s industrial modernization, with the service sector remaining a secondary priority. A more comprehensive approach that would boost domestic consumption and expand the services sector, among other elements, is likely needed to reduce China’s external and internal imbalances. Until that more decisive shift in policy takes place, China’s dependence on foreign demand will remain a point of contention with its trade partners and risk the sustainability of China’s own economic growth.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.