What Drives Rising Inflation? (Updated)

Robert M. La Follette School of Public Affairs and Department of Economics, University of Wisconsin

The Issue:

There are concerns about persistent – perhaps even accelerating – inflation, fueled by an overheating economy as a consequence of large fiscal stimulus, the Federal Reserve’s easy monetary policy to counter the pandemic downturn, and the combination of supply chain bottlenecks and a tightening labor market. The last bout of high and rising inflation, in the 1970s, was during a time of economic distress and only ended with a painful recession engineered by the Federal Reserve in the early 1980s. Are we in for a similar episode today? Whether inflation is likely to continue increasing depends on different factors that contribute to a generalized rise in prices.

Inflation was 6.8% in November 2021. Whether it is likely to continue increasing depends on different factors that contribute to a generalized rise in prices.

The Facts:

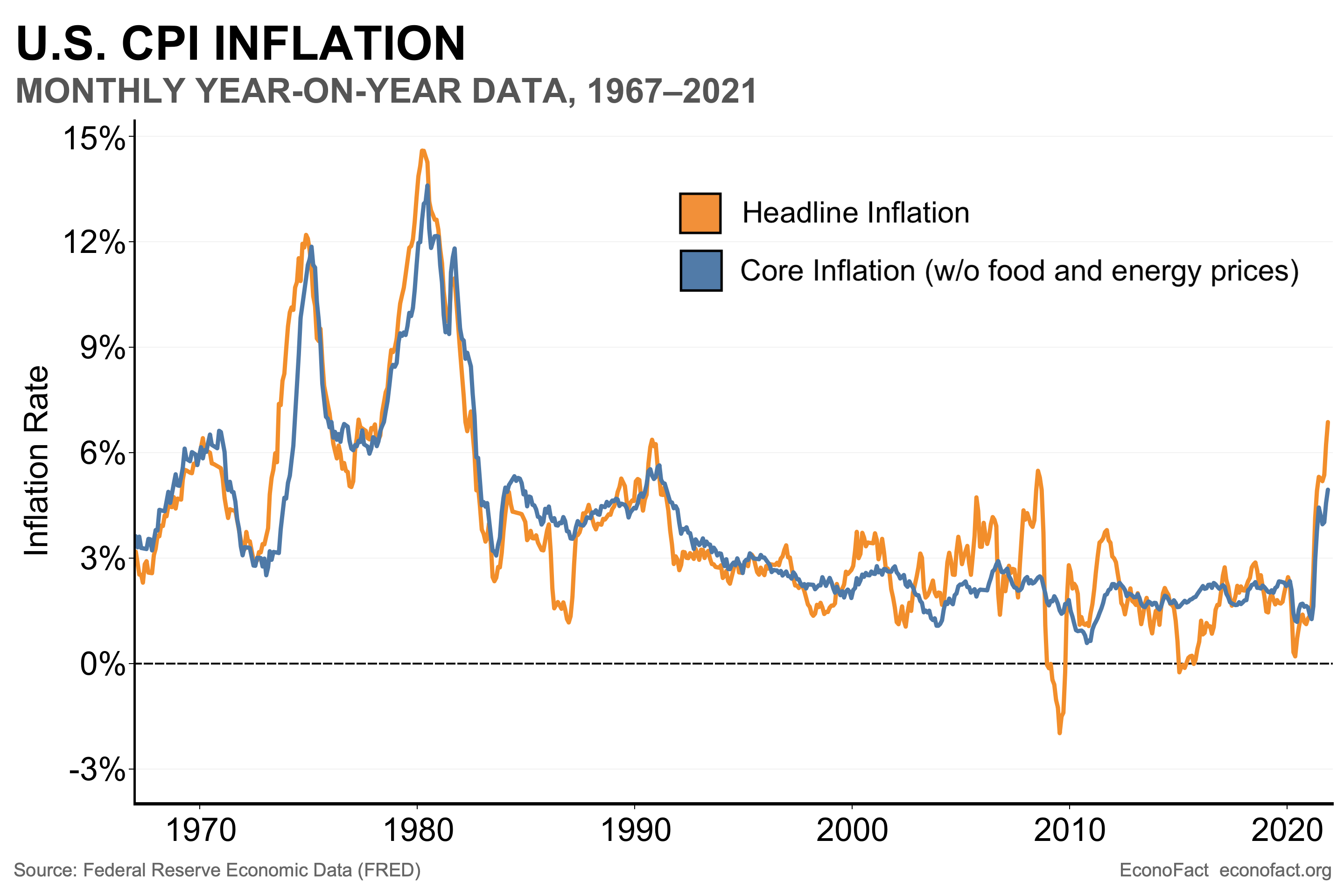

- Prior to the pandemic, inflation had been relatively low for about three decades, and especially quiescent over the past decade. Inflation is the rate of change of overall prices in the economy. The “headline” inflation rate is the rate of change of a basket of goods for a “typical” urban consumer. An alternative is the “core” inflation rate that strips out the prices of foods and fuels since these tend to be more volatile than other prices and, also, they can reflect factors other than the strength of the economy and the extent to which the economy is “overheating." One striking aspect of inflation trends over the past 50 years in the U.S. is that inflation has been much lower since the mid-1980s and, even more so, since the onset of the Great Recession — to the point of raising concerns that inflation was too low. Over the last decade, inflation has averaged only 1.7%. Contrast this with the 1970s when headline inflation averaged 7.5%, or even the period from 2000 to 2008 when inflation averaged 2.6% (see chart).

- Inflation has been rising over the past year, but this comes after especially low inflation in the immediate wake of the onset of the pandemic. The inflation rate for the 12 months ending in November 2021 was 6.8%. At the start of the pandemic the economy actually experienced price decreases, so the increase in prices seen since April 2020 was initially, to some extent, a catch-up in prices as the economy recovered from the pandemic. However, the price level has now overshot the trend previously set.

- In order to consider whether inflation is likely to continue at high rates, it is important to look at the different factors that contribute to a generalized rise in prices. Economists' preferred explanation for inflation, sometimes called the "expectations augmented Phillips curve", looks to some combination of three factors. The first is the degree of slack in the economy, which gauges to what extent the economy's resources are being utilized. When firms use labor and capital very intensively, production costs tend to rise and firms have more room to raise the price of their products to cover the costs. A second factor involves long-term expected inflation — businesses and people take into account the expected rate of inflation when making economic decisions, such as setting wage contracts or planning for product prices. These decisions, in turn, feed into the actual rate of increase in prices. Finally, increases in the costs of inputs to the production process, including wage costs can also drive inflation. The rise in oil prices in the 1970s, which fed into more widespread price increases, is a clear example of inflation driven by input costs.

- How much slack is there in the economy? The extent to which the economy is overheating is measured by the output gap, the difference between actual national income (GDP) and potential GDP. Potential GDP is a counterfactual measure of what the economy could produce if land, labor and capital were utilized at their normal rates. With the $1.9 trillion American Rescue Plan, the $1.2 trillion Infrastructure Investment and Jobs Act, and the $4 trillion spending during the previous administration, the Federal Reserve committing to low interest rates, and recovered consumer spending, the output gap is expected to shift from an economy that is currently producing below potential to one in which production exceeds its normal rate. (I think that the economy is likely to shift from a negative output gap (-1.7% in 2021Q3) to positive by 2022Q3, using CBO estimates of potential GDP and the November Survey of Professional Forecasters). This could fuel inflation – however, the relationship between a strong economy and inflation, the Phillips Curve, has been very flat in recent years and inflation seems to be insensitive to both a strong and a weak economy.

- Economists and households are marking up their expectations of inflation over the next year – although there is a divergence in views between the two groups. While in the relatively longer-term, financial markets project only a slight acceleration in inflation over the next five years. The Survey of Professional Forecasters in November 2021 implied an expected inflation rate of 2.7% in 2022. A combination of financial market information and survey data indicates 2.6% over the next year to December. Households expect higher inflation – at about 4.9% -- but on average households typically expect higher inflation than economists (by about a percentage point) and have consistently overpredicted inflation over the past two decades. Longer-term inflation expectations have been relatively stable. Anticipated inflation rates inferred from financial markets – namely the gap between yields on Treasury bonds and Treasury inflation-protected securities (TIPS) — have risen substantially since the 2020 election, and this spread stands at 2.76%, about 1.1 percentage points above where it stood at the beginning of 2020. However, when accounting for risk and liquidity premia, the implied increase has been much smaller, at least through the end of October.

- Is the cost of inputs likely to continue rising? Production difficulties, from the shortage of semiconductor chips and heightened demand for certain products like lumber, have raised concerns that bottlenecks in the supply chain could drive up critical input prices, feeding through into overall prices. Such price changes have been particularly noticeable in specific sectors, such as autos and construction. Oil prices nearly doubled, from their lows in April 2020 to November’s levels. Some commodities such as copper have also seen marked increases— with consequences for prices down the line in construction and other sectors. But for these factors to have a persistent effect on inflation, prices would need to keep rising at these rapid rates.

- Will labor costs continue to rise? Wages for workers in certain sectors – including those in previously hard-hit industries like leisure and hospitality – have surged, exceeding the rate of inflation. This has occurred as some workers have exited the labor market, either due to public health concerns or the availability of child care, or other reasons.

- Will too much money chasing too few goods cause inflation? There is also a so-called "Monetarist Approach" in which inflation is thought of as “always and everywhere a monetary phenomenon.” Under this view the rate of inflation corresponds to the rate of growth of the money supply minus the growth rate of the economy. The Fed has increased the broad measure of money supply, defined as the sum of currency and checking and savings deposits, by 37.5% since January of 2020. The evidence has not been supportive of this explanation of inflation, however. Even before the Great Recession of 2007-09, the relationship between the money supply to GDP and changes in the price level had proven highly erratic, so much so as to prove an unreliable guide to inflation.

What this Means:

Inflation — both actual and expected — matters. Inflation makes it harder for consumers and workers and firms to distinguish between relative and general price changes. It also makes it more difficult to make plans for saving and investment. And, higher expected inflation raises borrowing costs for the government (although higher actual inflation erodes the real value of government debt). Finally, the Fed tends to respond to higher inflation by tightening monetary policy, which depresses economic activity. Hence, the stakes are high for avoiding a sustained acceleration in inflation. So far, inflation has risen in a halting fashion, but remaining more persistently high than previously anticipated. Near term expectations of inflation have risen, but remain relatively muted – particularly amongst economists -- either because the anticipated output gap or the responsiveness of inflation to the output gap are thought to be small, longer term inflation expectations remain well-anchored, or all three.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.