Can the Fed Taper Without a Market Tantrum?

Harvard Kennedy School

The Issue:

Between the beginning of the COVID-19 crisis and November 2021, the Federal Reserve has purchased a bit over $4 trillion of Treasury and mortgage-backed securities in an effort to stabilize financial markets and stimulate the economy. As the economy recovers, the need for these monthly large-scale purchases to continue at the same rate diminishes. But slowing down the rate of these securities purchases presents challenges. In the recovery from the Great Recession, the announcement that the Fed was considering tapering its security purchases sent the markets into a "tantrum" that saw a spike in interest rates on Treasury bonds. Will history repeat itself?

The need for monthly large-scale purchases of Treasury and mortgage-backed securities by the Fed diminishes in the recovery. But slowing the rate of these purchases presents challenges.

The Facts:

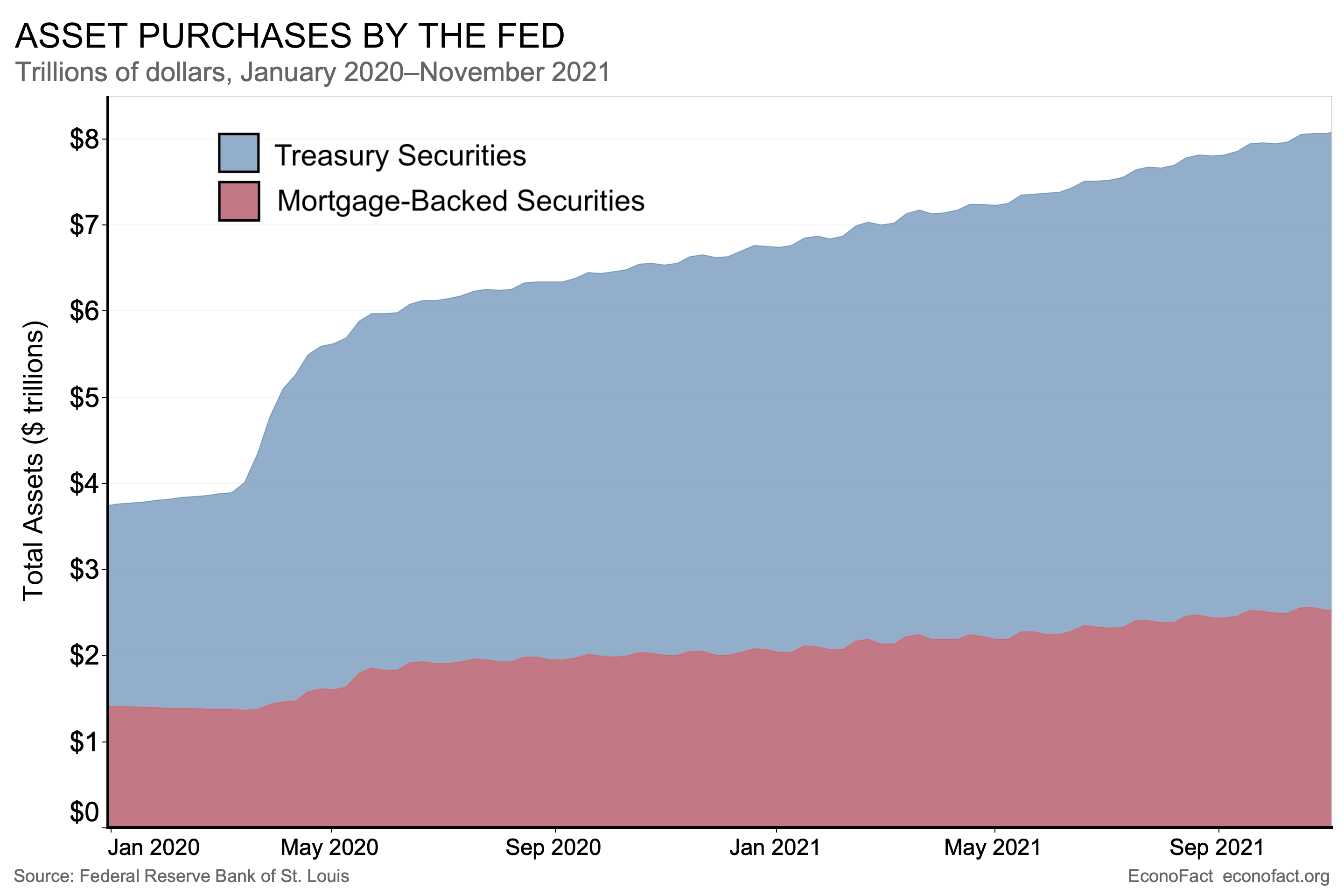

- The Federal Reserve initially began large-scale purchases of Treasury securities in March of 2020 to stabilize financial markets facing atypical turbulence in the COVID-19 pandemic. With the realization that the shutdowns necessitated by the COVID-19 pandemic would plunge the U.S. economy into recession, and facing uncertainty about how deep the contraction might be and for how long, key financial markets pulled into their shells, turtle-like, in the spring of 2020. At first there was a significant decline in both bond yields and in stock market values — the expected response for both in the face of incipient economic turbulence as investors seek the safety and liquidity of Treasuries. But between March 9 and March 18 stresses in the markets for Treasury securities led to a surprising 0.64 percentage point increase in the 10-year Treasury yield from 0.54 percent to 1.18 percent even as the stock market continued to fall. This sudden spike in Treasury yields has been attributed in part to large sales of Treasury securities by investors facing immediate liquidity needs (see here). In response to the crisis, the Federal Reserve quickly mobilized programs, both tested and novel, to restore financial market function and make sure that the supply of credit continued to flow to businesses. The Fed’s purchase of $1 trillion of Treasury securities by the end of the first quarter of 2020 met the goal of restoring financial market function for the stressed Treasury market.

- Long after financial markets had stabilized, the Federal Reserve continued with massive purchases of longer-term Treasury securities and U.S. government-insured mortgage-backed securities, which also served the purpose of stimulating the macroeconomy. Purchases of Treasuries and mortgage-backed securities (MBS) are intended to keep longer-term interest rates low, so that businesses that continue to borrow can do so at favorable rates. When the Fed purchases Treasuries and MBS that are in high demand by private markets, they of course become scarce, leading investors to accept even lower interest rates as inducement to purchase. Other things equal, those low long-term rates kept the economy from sinking even deeper into recession, leading to even greater loss of employment. For this reason, the rapid buildup of purchases of Treasury and mortgage-backed securities at the onset of the crisis was followed with a continued steady pace of security purchases since the summer of 2020 (see chart). The Federal Reserve made the pace of these purchases explicit in December 2020 when it announced that it would be purchasing Treasury and mortgage-backed securities at a pace of $80B and $40B respectively each month. (Prior to that, it had stated that it was purchasing these securities “in the amounts needed to support smooth market functioning” (April 29, 2020), and “at least at the current pace” from June through November 2020).

- As the economy showed signs of recovery, the Federal Reserve signaled that it would shift towards a gradual reduction in the pace of asset purchases or "tapering". While the contraction in economic activity in the spring of 2020 was extremely rapid, so too was the rebound: Just one year after the downturn, real GDP had more than regained its pre-pandemic level. As is common in downturns, the unemployment rate has taken somewhat longer to recover. But one year after a nearly 15 percent decline in employment and ten percentage point rise in unemployment, the unemployment rate had recovered smartly, dipping to 4.2 percent in November of 2021. The rapid rebound in demand, coupled with some key supply shortages — in labor as well as in key inputs to production — has led to a surge in inflation that is larger than we have seen in thirty years. In recognition of the recovery in economic conditions, the Committee in its September 22, 2021 statement suggested that an “adjustment [in its asset purchases] may soon be warranted.” At its November 2021 meeting, the Committee announced that it would slow the pace of purchases to $70B and $35B per month, respectively, and expects to slow the pace further to $60B and $30B in December, further tapering purchases by $10 and $5B respectively in each of the ensuing months. This gradual slowing in the pace of purchases is precisely the taper that markets have expected and discussed for some months.

- While this tapering will decrease the size of monthly purchases, it will leave most of the rather large stock of Treasuries and MBS that the Fed now holds on its balance sheet. So, why taper? Reducing the pace of purchases should, other things equal, provide a bit less stimulus to the economy, by exerting less downward pressure on long-term interest rates. This modest adjustment to the Fed’s policy stance is unlikely to have dramatic effects on business sales and employment, but it will take a little steam out of the economy.

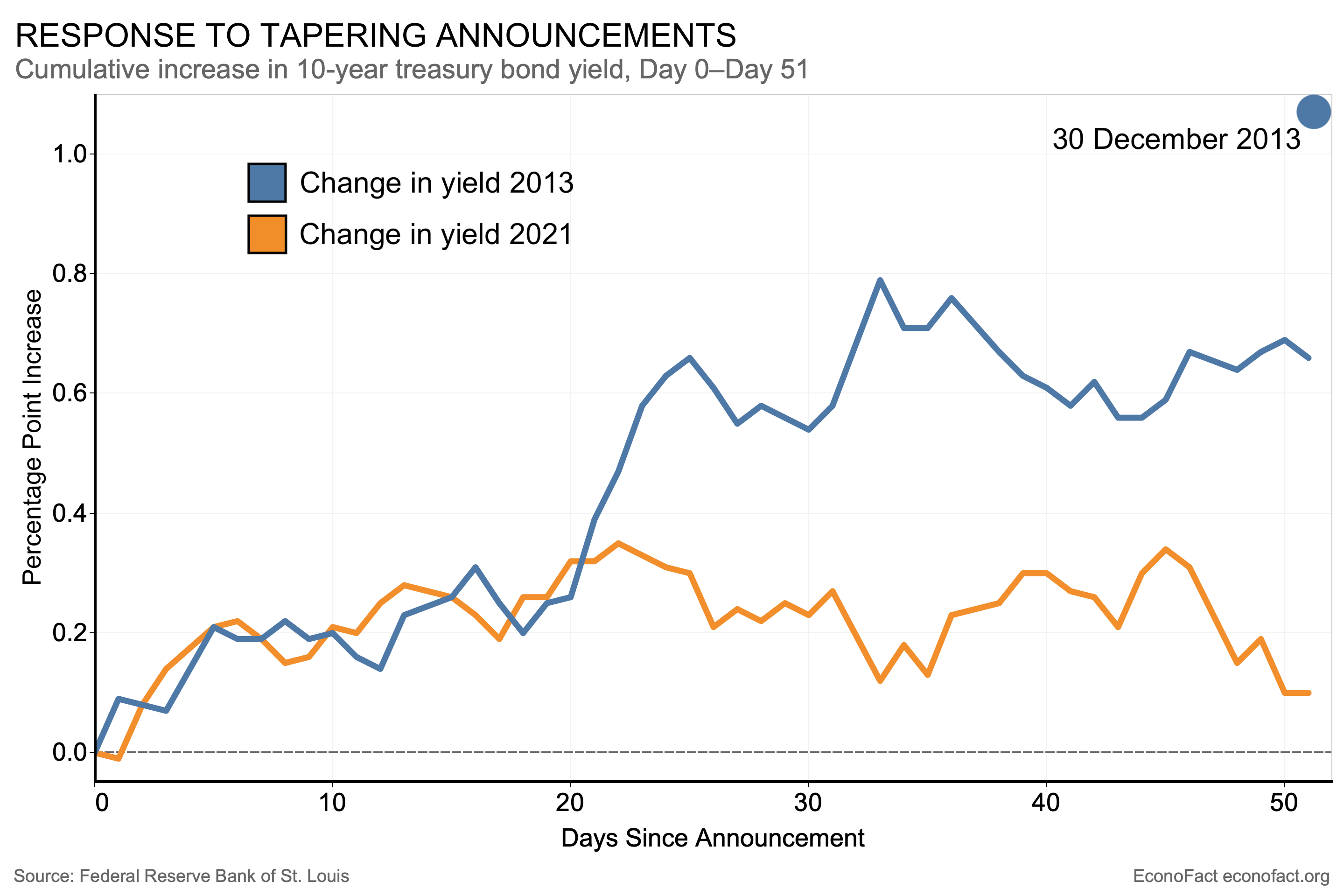

- Why did this seemingly simple and small adjustment to the Fed’s asset purchase garner so much attention in financial markets? To understand this, we have to roll back a few years to a parallel period in U.S. economic history, during the recovery from the Great Recession and Financial Crisis. The Fed during that earlier episode had purchased a similar total amount of Treasuries and MBS, albeit spread over a much longer period. As unemployment fell in late 2012 and early 2013, it looked like it might soon be time to pull back a bit on the stimulus that asset purchases provided. While then-Chairman Bernanke had attempted some earlier signals, on May 22, 2013 he announced that the Fed would begin tapering its asset purchases at some future date. The suggestion that they were considering ending those purchases sent Treasury markets into the so-called "taper tantrum". On that day, the yield on 10-year Treasury constant-maturity bonds began to rise, ultimately increasing by more than one percentage point over the next seven months. That was the “tantrum”: At the announcement of what seemed a relatively uncontroversial and gradual adjustment to monetary policy, markets both immediately and over the ensuing months priced in considerably higher interest rates.

- Does the initial market reaction to tapering in the recovery from the COVID recession resemble the reactions to tapering following the Great Recession? If we look at the most recent period, dating the announcement of the intent to taper at the September 22 FOMC statement, we can see that at first, this episode closely mirrored its cousin in 2013. But the episodes now differ in important ways. In the current case, the Fed began tapering its purchases just six weeks after announcing their intent, eliciting little or no response from Treasury rates, which have moved more-or-less sideways since a few days after the September announcement. In the 2013 episode, the 10-year rate continued to rise to 3 percent by year-end (the blue dot in the chart) — more than a percentage point higher than pre-announcement — even though purchases continued well into 2014 and actual tapering came much later than in the current episode.

What this Means:

Given the recovery and apparent ongoing strength of demand in the economy, and no doubt with a nod towards elevated inflation and the (as yet incomplete) stimulative fiscal packages that are in train, the tapering that the Fed initiated seems a prudent policy action. A high degree of uncertainty remains, especially given the inherent unpredictability of the public health situation. I hesitate to predict the future course of the 10-year Treasury yield, as we are relatively early on in this tapering episode. But since the announcement was quickly followed by actual tapering in this case, and the response thus far has been fairly muted, it seems less likely that the market will react too much more to the continued, gradual reduction in purchases. Time will tell.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.