What is the Fed Doing to Stabilize Financial Markets?

Williams College

The Issue:

The coronavirus pandemic, together with the related disruptions in oil markets and the policy responses by many different governments to the crisis — including restrictions, closures and quarantines, impacting a wide range of businesses in different sectors — have contributed to asset market volatility and threats to the smooth functioning of financial markets. The Federal Reserve has taken emergency measures to loosen monetary policy and to stabilize the market for U.S. Treasury securities following what has perhaps been the wildest week on Wall Street since the 2008 financial crisis. In a surprise move on Sunday March 15, the Federal Reserve cut the federal funds rate to between 0.0 percent and 0.25 percent and announced that over coming months the Committee will increase its holdings of Treasury securities by at least $500 billion, and its holdings of mortgage-backed securities by $200 billion. That move followed two prior announcements aimed at the market for U.S. Treasury securities in the preceding days. What prompted the Fed to take these steps? How will they help alleviate the effects on financial markets of the pandemic? Does this represent a bailout of banks, as some have alleged?

The Fed announced plans to lend $1.5 trillion to banks and financial institutions and increase its purchases of U.S. Treasury securities

The Facts:

- The coronavirus pandemic has very abruptly raised the odds of a slowdown for the U.S. economy, prompting the Federal Reserve to take emergency measures with respect to monetary policy. But, with already low interest rates, the Fed's options are somewhat limited in that respect. The Federal Reserve announced on Sunday, March 15, that it would cut its target interest rate near zero. This was the second emergency rate cut for the Fed in the span of two weeks: The Fed had cut the target range for the federal funds rate by 50 basis points (the equivalent of 0.5 percentage points) to 1-1.25 percent on March 3, during a meeting that occurred outside the normal six-week cycle of Federal Open Market Committee (FOMC) meetings.

- The surprise rate cut comes on the heels of a dramatic effort last week to stabilize the market for U.S. Treasury securities. A smoothly functioning market for U.S. Treasury securities is vital to the global financial system. U.S. Treasuries, the bonds that the U.S. government issues when it borrows money, are considered among the safest assets to hold because they offer a guaranteed interest rate for a specific maturity date with no risk of default — as they are guaranteed by the U.S. government. The $17 trillion worth of U.S. Treasury securities are held widely across the world, with $3 trillion held by U.S. banks and mutual funds and another $6 trillion held by foreign institutions and central banks. Aside from being a safe haven for investors at times of heightened uncertainty, these securities are vitally important for the functioning of a range of financial markets. They are widely used as collateral that back up repurchase agreements (“repos”), which are a major source of funding for investment banks. Furthermore, the pricing of many futures and options contracts are based on the interest rates of Treasury securities, and these futures and options contracts help reduce uncertainty for the prices that will be received by, for example, farmers and those purchasing agricultural goods, those buying and selling oil, and companies involved in exporting and importing. All of these markets and institutions rely on the ability to rapidly sell their holdings of Treasuries in order to make transactions and satisfy depositors’ and investors’ demands for cash.

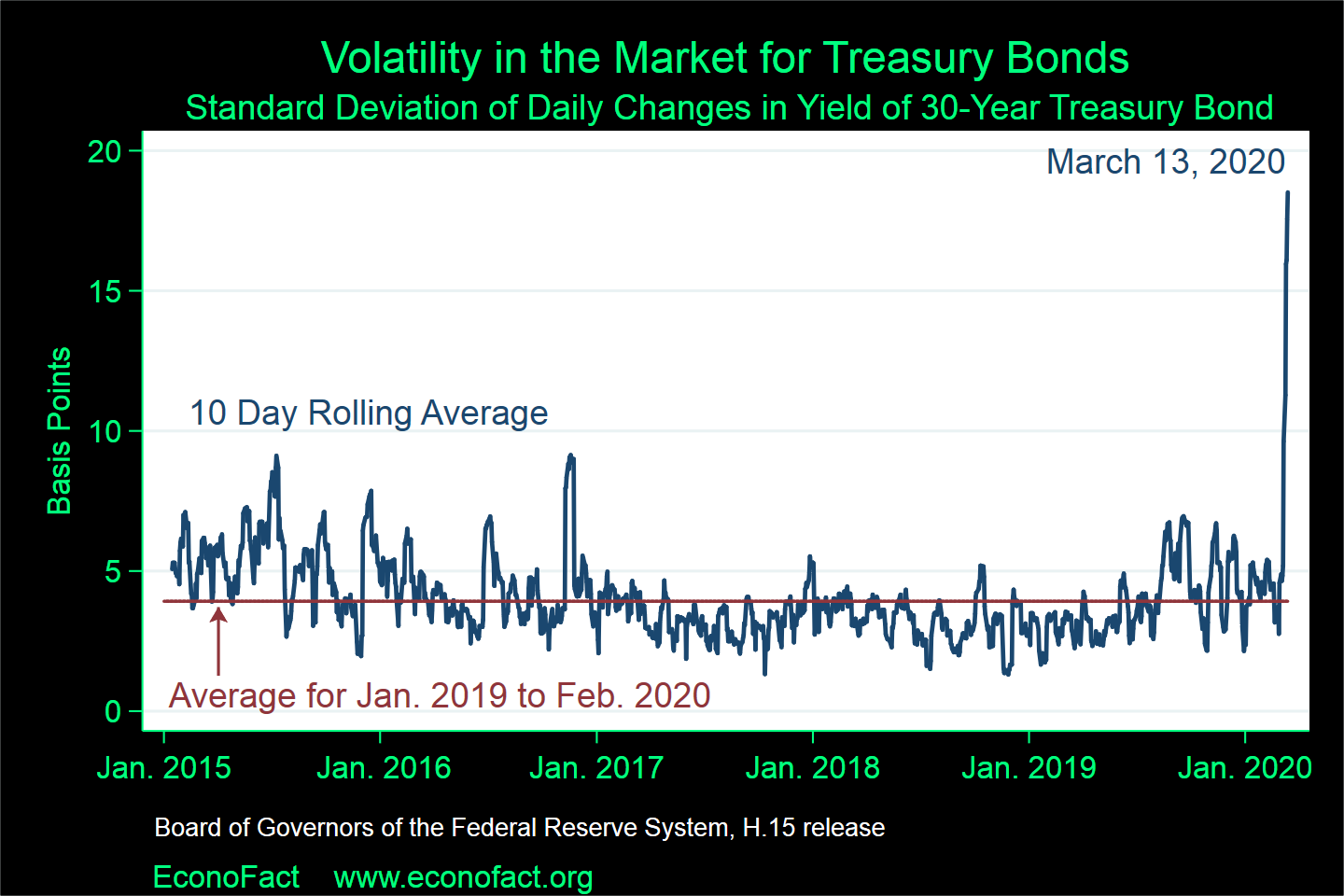

- The market for U.S. Treasury securities came close to the breaking point during the week of March 9-13. The market for U.S. Treasury securities is normally highly liquid, meaning they can be bought and sold at short notice without materially affecting the price. The high degree of liquidity is reflected in the very small difference between prices offered by buyers and those that sellers are willing to accept (the “bid-ask spread”), which is normally around 4 or 5 basis points (hundredths of a percentage point). On Thursday, however, traders reported spreads as high as 50 basis points. The unusually wide spread is symptomatic of a situation in which buyers are unable to find ready sellers, and vice versa. Several factors likely contributed to the disruption. The sheer volatility in the bonds’ prices is one. As shown in the graph, the standard deviation (a common measure of volatility) of the yield on 30-year Treasury bonds hit 18 basis points by the end of the week, compared with 4 basis points during normal periods; and since the price of a bond is inversely related to the yield, this implies a comparable jump in price volatility. The gyrations in the stock market also may have played a role, as they likely increased the demand for the most liquid Treasury securities. There are also anecdotal reports that by interfering with communication, work-at-home arrangements have inhibited traders’ activities.

- Last week's actions with respect to U.S. Treasury securities were narrowly focused on restoring normal market functioning. The Federal Reserve Bank of New York announced plans to lend $1.5 trillion to banks and financial institutions “to address highly unusual disruptions in Treasury financing markets associated with the coronavirus outbreak,” Thursday March 12. The next day it announced that it would purchase $37 billion in United States Treasury securities, again citing disruptions in the market for these bonds. The $1.5 trillion operation announced on March 12 allows banks to borrow from the Fed for periods as long as three months, using Treasury securities as collateral. This enables banks and other financial institutions to access needed funds without having to sell the Treasury securities outright, which could cause disruptions if a widespread sale flooded the market for these bonds. Similarly, the Fed’s purchases of $37 billion in United States Treasury securities announced on March 13 will allow owners of these bonds to sell them directly to the Fed rather than attempting to undertake transactions in the secondary market where, as indicated by ballooning bid-ask spreads, buyers are scarce.

- The actions are not in any sense a bailout of banks or financial institutions. Contrary to a recent tweet from Senator Bernie Sanders, the Fed is not simply “handing out” $1.5 trillion to Wall Street. The funds are short-term collateralized loans, made at competitive market-based rates, so there is no subsidy involved for those borrowing from the Fed. Nor do the loans represent a capital injection, as stated in some press reports since the cash received through this borrowing does not represent an increase in banks’ capital, that is, banks’ assets that help buffer their balance sheets against decreases in the value of their lending and securities. A capital injection would only occur if the Fed were taking an equity stake in a financial institution—which is not allowed under the Federal Reserve Act.

- Unlike the rate cut and asset purchases announced on March 15, the specific actions taken on March 12 and 13 are not monetary policy. They did not lead to a reduction in the federal funds rate, whose lower bound is determined by the interest rate paid on excess reserves. Nor were they a form of Quantitative Easing (QE), the unconventional tools that the Federal Reserve used to implement monetary policy during the financial crisis when the federal funds rate had been cut to virtually zero. If used to its full extent, the $1.5 trillion lending program would significantly enlarge the Fed’s $4 trillion balance sheet; but this would have been a temporary increase, not the long-term expansion that would be undertaken as part of QE. Similarly, the $37 billion in purchases entails bringing forward the previously scheduled asset purchases associated with its planned policy “normalization.” The policy move announced on March 15 was fundamentally different from the previous week’s actions, as its explicit intention was to reduce the federal funds rate, and it represents a return to re-deployment QE.

What this Means:

The covid-19 pandemic has created an unprecedented array of problems for the world economy. Those related to public health will surely require difficult and costly solutions. Aggressive fiscal policy and transfers will most likely be needed to address the macroeconomic fallout. With interest rates already so low and the effectiveness of Quantitative Easing uncertain, the Fed’s role in providing macroeconomic stimulus through monetary policy may be limited. But ensuring the smooth functioning of the market for U.S. Treasury securities is an important element of the collective policy response — and one the Federal Reserve is able to do with the tools it has on hand.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.