Fed Policy: Is it Time to Take Away the Punch Bowl? (UPDATE)

Williams College

The Issue:

The Federal Reserve kept interest rates low (and took extraordinary expansionary actions) in response to the financial and economic crisis that began in the autumn of 2008. Beginning in December 2015, as the recovery gained traction, the Fed began gradually raising the federal funds rate, the interest rate banks charge for overnight lending of reserves. The tightening of monetary policy after a prolonged expansion is consistent with the notion that central banks should “take away the punch bowl just as the party is heating up,” an aphorism credited to William McChesney Martin who served as Chairman of the Federal Reserve in the 1950s and 1960s. But tightening monetary policy has incurred the wrath of President Trump who tweeted on July 22, 2019 that “The Fed raised & tightened far too much & too fast. In other words, they missed it (Big!). Don’t miss it again!” Is it, in fact, time to take away the punch bowl? And how spiked is it?

The federal funds rate remains below where it would normally be, given current economic conditions. But there is significant uncertainty in the assessment.

The Facts:

- The Federal Reserve has operated, since 1977, under the dual mandate from Congress. This dual mandate requires the Fed to “promote effectively the goals of maximum employment, stable prices, and moderate long term interest rates.” In practice, this has resulted in the Federal Reserve setting monetary policy to stabilize the economy, having it run neither too hot nor too cold. This “Goldilocks” goal typically involves the twelve members of the Federal Open Market Committee (FOMC), the policy-setting body of the Federal Reserve, deciding at one of its eight annual meetings to raise the federal funds rate when there are sufficient concerns about rising inflation and to lower the federal funds rate when there are sufficient concerns about rising unemployment and a slowing economy.

- While the FOMC comes to its decisions through deliberation, it turns out that the federal funds rate usually tracks a rule that estimates the behavior of the Federal Reserve. A monetary policy rule, such as the eponymous Taylor Rule, prescribes an interest rate that is higher when inflationary pressures are higher and lower when the economic performance is weaker. Policy rules typically include three elements: an interest rate consistent with the economy operating at full employment (the natural interest rate); a term reflecting the difference between actual inflation and the Fed’s target of 2 percent inflation; and a term reflecting the output gap between actual economic performance (as measured by Gross Domestic Product, GDP) and the level of potential GDP, that is, the GDP that would occur if the economy was running at full employment (but note that full employment does not mean unemployment is zero). Stronger GDP growth is associated with lower unemployment, and this is the link between the policy rule and the employment demand of the dual mandate.

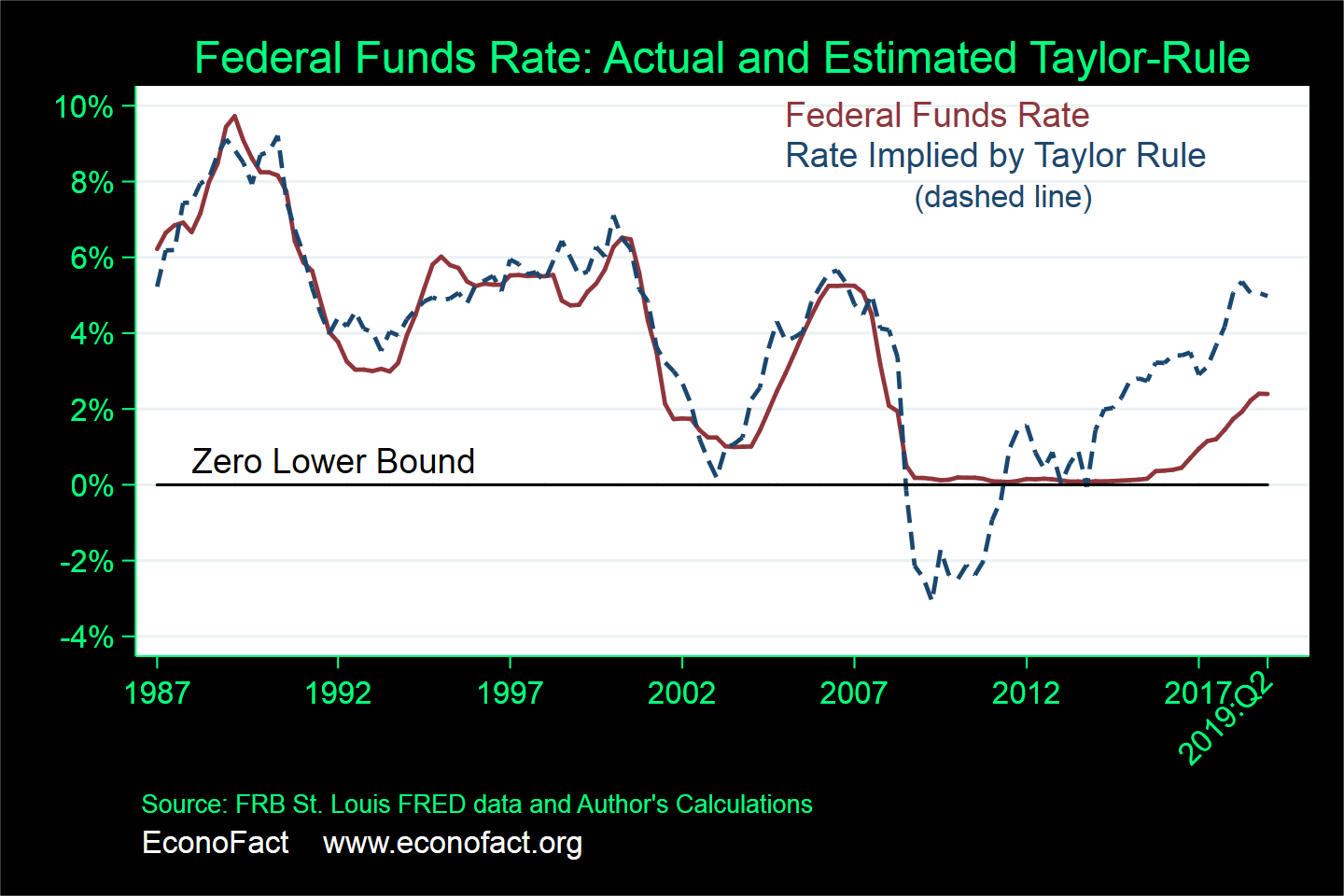

- The figure shows the policy rule that closely tracks the actual federal funds rate from the late-1980s until the financial crisis that began in the Autumn of 2008. The correlation between the actual federal funds rate and the policy rule estimate is 95 percent from 1987 through the summer of 2008. Once the crisis hit in September of 2008, however, the subsequent correlation was only 69 percent (using data from the third quarter of 2008 through the second quarter of 2019. The figure shows that one reason for the divergence since the onset of the Great Recession is that the federal funds rate cannot be negative (or at least cannot be more than a little bit negative), a condition known as the zero lower bound. (When a depositor faces negative interest rates, she is paying a bank to hold her money, and could avoid this cost by just holding cash). The weakness of the economy in the wake of the financial crisis that began in September 2008 was so profound that the interest rate consistent with the policy rule was negative. The Federal Reserve had to resort to Unconventional Monetary Policies at this time, including Quantitative Easing. The subsequent recovery of the economy saw the rule-implied interest rate moving into positive territory and, in fact, exceeding the actual federal funds rate in every quarter beginning with the last quarter of 2011. Since the beginning of 2015, the rule-implied rate has exceeded the federal funds rate by the largest amount seen over the past 30 years, showing the tilt towards expansionary monetary policy. As of the second quarter of 2019, the rule-implied rate is 2.6 percentage points above the current federal funds rate. The fact that the interest rate implied by the policy rule exceeds the actual federal funds rate indicates that monetary policy is currently expansionary, that the punch bowl has yet to be removed.

- The unwinding of Quantitative Easing policies may mean that monetary policy is slightly tighter than what is suggested by the difference between the federal funds rate and the rate implied by the policy rule. Quantitative easing refers to the policies undertaken by the Fed to stimulate the economy when the federal funds rate approached the zero lower bound. These policies included purchasing assets that had not typically been part of the central bank’s portfolio, such as Mortgage-Backed Securities, driving up the price of those assets and driving down the interest rates they offered. As these purchases are unwound, and the Federal Reserve reverses its earlier policies and sells its holdings of these assets, the interest rates on them will rise even with no change in the federal funds rate. Thus, the federal funds rate will understate the extent of monetary tightening. But the impact of this unwinding is hard to gauge due to the uncertainty associated with estimates of the effects of Quantitative Easing. A high-end estimate of the cumulative impact of Quantitative Easing is the equivalent of a 4.5 percentage point cut in the federal funds rate. Taking this at face value, a rough back-of-the-envelope calculation is that the $500 billion shrinkage in the Fed’s balance sheet thus far, representing a reversal of about one-eighth of the accumulated portfolio from Quantitative Easing, translates into a 0.6 percentage point increase in the funds rate. This would make the current 2.4 percent rate equivalent to 3.0 percent, but this is still below the rule-implied rate, suggesting that, even with this adjustment, monetary policy tilts toward easing.

- There are other sources of uncertainty about the policy rule as well. As mentioned above, the calculation requires an estimate of the natural interest rate. Some economists have hypothesized that the natural rate has declined in recent years, however. One widely cited econometric estimate puts it at 0.6 percent (as of the second quarter of 2019), 1.4 percentage points lower than the conventional 2 percent assumption. Assuming no change in the natural rate since then, the federal funds rate implied by the policy rule would be right in line with the current funds rate target. Views also differ regarding the size of the output gap used in the calculations. The figure uses estimates from the Congressional Budget Office, which puts the gap at 0.9 percent of GDP as of the second quarter of 2019. Other sources report larger gaps. For example, the same methodology that generates the natural rate of 0.6 percent in the second quarter of 2019 estimates a gap of 1.8 percent. This, along with the natural rate estimate of 0.6 percent, would prescribe a federal funds rate of 4.4 percent for that quarter, 2 percentage points greater than the actual federal funds rate of 2.4 percent.

- Monetary policy should anticipate future developments, of course, and not just respond to current conditions. One justification for the current loose monetary policy is the uncertainty and downside risks facing both the U.S. economy and economies of other countries. The International Monetary Fund (IMF), for example, anticipates sluggish global growth and softening inflation. Its July 2019 World Economic Outlook said that the risks “are mainly on the downside,” citing trade tensions and financial vulnerabilities, among other factors. Similarly, the forecasts for U.S. GDP growth from the Survey of Professional Forecasters (SPF) have been revised down for three successive quarters. Still, the SPF’s 2% growth forecast for the remainder of 2019 implies that a significant adverse “shock”—equivalent to at least a full percentage point of GDP — would be required for a conventional policy rule to be consistent with the current level of the federal funds rate.

What this Means:

No mechanistic formula will ever be able to determine definitively whether monetary policy is excessively tight, given the uncertainty associated with estimates of the natural rate of interest, potential output, and the effects of the unwinding of Quantitative Easing. These caveats notwithstanding, the policy rule commonly used to evaluate the stance of monetary policy indicates that the current federal funds rate is not out of line with historical experience; if anything, the funds rate remains below where it would normally be, given current economic conditions. Concerns about an overly restrictive policy are therefore overblown — although a significant deterioration in economic conditions could change that assessment.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.