What is Modern Monetary Theory?

The Fletcher School, Tufts University and Williams College

The Issue:

Modern Monetary Theory (MMT) has attracted attention, especially among many who see in it a support for greater government spending. Representative Alexandria Ocasio-Cortez (D-NY) says MMT should be “a larger part of the conversation” and Senator Bernie Sanders (I-VT) has drawn on the advice of Professor Stephanie Kelton (Stony Brook), a prominent advocate of MMT. However, there is confusion about the ideas underlying MMT and controversy about its proposed policies. While some have taken MMT to say that government budget deficits do not matter, its proponents say there are situations when deficits are a source of concern. How does MMT differ from more conventional macroeconomics and what are its main policy prescriptions?

There is confusion about the ideas underlying MMT and controversy about its proposed policies.

The Facts:

- Proponents of Modern Monetary Theory emphasize that a country that controls its own currency and borrows in its own currency, like the United States, cannot default on its debt. This is because the central bank can, if necessary, “print” the money needed to pay the government’s creditors, a process called monetization. MMT proponents argue that a high level of debt, relative to GDP, should not by itself constitute a constraint on deficit spending. As Stephanie Kelton puts it: "The only potential risk with the national debt increasing over time is inflation" (see here for Kelton's explanation of MMT). Proponents argue that the government can, and should, use deficit spending aggressively to boost employment. As MMT proponent Phil Armstrong wrote in 2015 “The existence of unemployment is clear de facto evidence that net government spending is too small to move the economy to full employment. … [The government] must use its position as a monopoly issuer of the currency to ensure full employment.”

- Sustained deficit monetization is inflationary. Consequently, governments have used it only as a last resort, when there is no other way to finance the budget deficit. It is true that in normal circumstances inflation results from a number of factors other than the issuance of money, such as wage pressures from low unemployment and from sharp increases in the prices of commodities like oil. While these short-run influences on inflation can obscure the underlying long-run link between money and prices, there is little doubt that “too much money chasing too few goods” will eventually raise inflation.

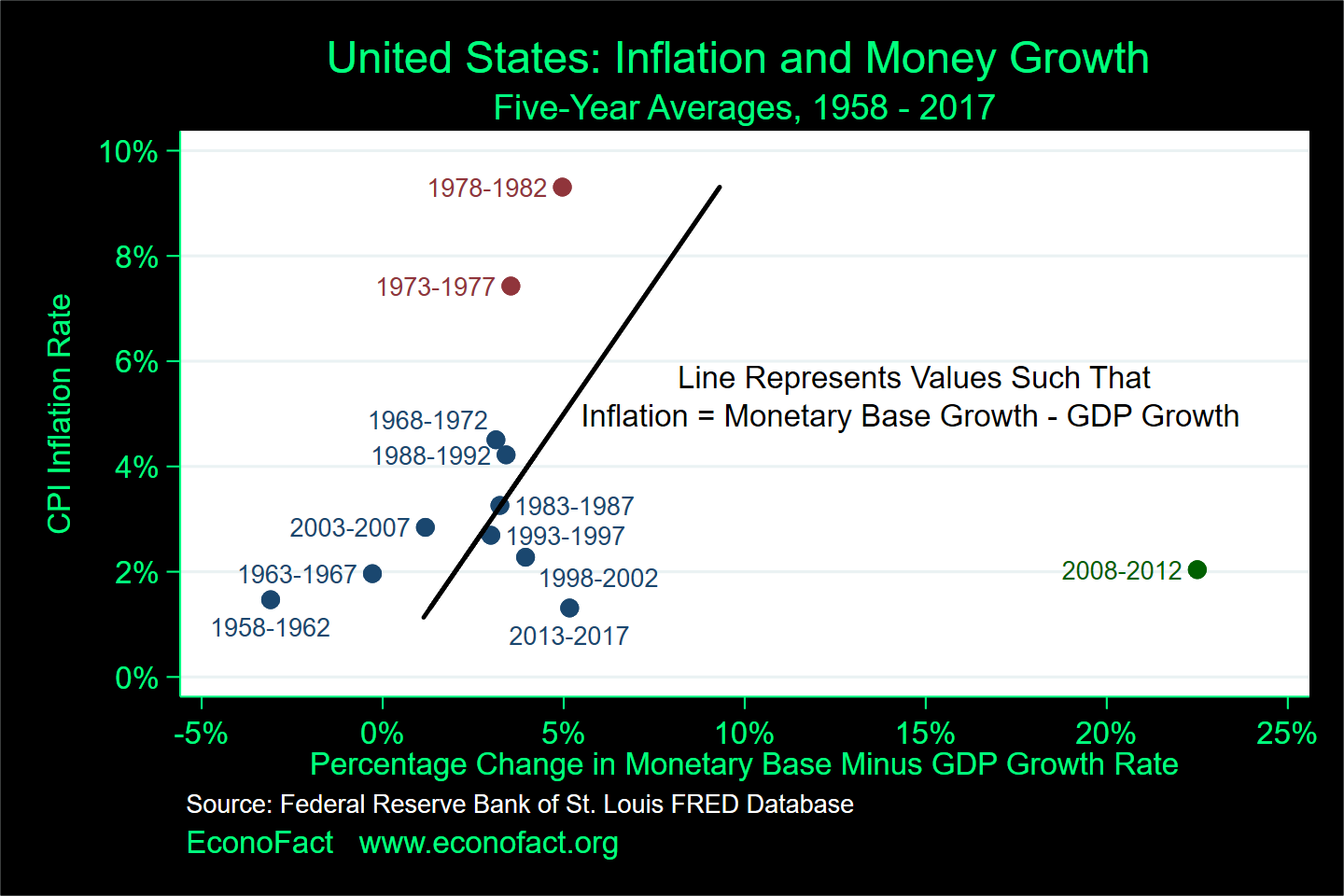

- The evidence supports the view that money growth in excess of GDP growth causes inflation. This relationship for the United States is evident in the scatterplot of the inflation rate of the Consumer Price Index over five-year periods (measured on the vertical axis) and the difference between the growth rate of the monetary base (that is, the rate of growth of currency and bank reserves, which are directly controlled by the Federal Reserve) and the rate of growth of GDP over those same five year periods. The black line represents values for which the rate of inflation equals the rate of growth of the monetary base minus the GDP growth rate. The figure shows that these five-year averages cluster around the dashed line for the period 1963 through the period just before the onset of the Great Recession in 2008. In general, the rate of inflation has been equivalent to the difference between the growth in the monetary base and economic growth. There are exceptions. Inflation was greater than what you would have expected just from the difference between growth in the monetary base and the growth of the economy during the period of the oil shocks. The observations from 1973 to 1982 (denoted by red dots) represent a surge in inflation in the wake of the spike in oil prices in 1973 and rising expectations of ongoing inflation by the public. One conspicuous outlier is the 2008 – 2012 period (green dot) when inflation remained low despite rapid growth in the monetary base through Quantitative Easing (QE). During that time, the rise in bank reserves, which is one component of the overall money supply, was not matched by a commensurate rise in bank lending due to the weakness of the economy during the Great Recession.

- MMT gives the President and Congress a greater role than the Federal Reserve for maintaining price stability. MMT proponents, such as Stephanie Kelton, argue that inflation results from an overheating economy (for instance, in this podcast she says that at some future point the debt can get to be so large that interest payments on the debt — on top of normal government spending — can end up meaning that there is too much income chasing too few goods). It follows from this that "too much income" can be controlled by either tax increases or reducing government spending. This manner of managing inflation is the opposite of the current arrangement, in which the Fed has the dual mandate of maintaining price stability and full employment. There are two reasons why independent central banks are traditionally given this responsibility. First, elected officials have a temptation to cut taxes and increase spending in advance of an election. Consequently, it is implausible to assume that they will be willing to do either to restrain inflation before elections. Independent central banks are relatively immune to political pressure that would lead to this kind of short-sighted or opportunistic policy and, in fact, this is why they are given this insulation from the political sphere. Second, monetary policy can react more nimbly than fiscal policy to changing economic conditions. (The Fed’s FOMC meets eight times a year to decide on interest rate adjustments.) But since the government usually adjusts taxes and spending only during the annual budget cycle, fiscal policy cannot react nearly as quickly as monetary policy to inflationary pressures.

- MMT’s downplaying of debt sustainability is problematic. Deficit spending, plus the interest paid on what it already owes, increases the government’s outstanding debt. The debt burden is said to be sustainable when the ratio of debt to GDP is stable. Sustainability does not require the government deficit to be zero, or that the government needs to run budget surpluses; rather, it requires that the debt increase at the same rate, or more slowly than, GDP growth. There is a legitimate debate among economists regarding the maximum sustainable level of debt and the appropriate debt-to-GDP ratio. For example, Olivier Blanchard, a former Chief Economist of the International Monetary Fund, has argued that debt sustainability is less of a pressing problem in the current climate of low interest rates. Nonetheless, there is a limit to the deficit that can be sustained without leading to an explosion in the debt-to-GDP ratio. The ratio for the United States has, until relatively recently, remained below 70 percent of GDP. But as William Gale (Brookings) has pointed out, government debt, which is currently 78 percent of GDP and expected to rise, may already on an unsustainable path, even assuming low interest rates and in the absence of the spending envisioned by MMT proponents, given the expected increases in government outlays due to the aging of the population.

- MMT also ignores the distributional effects of paying for government borrowing. Debt has distributional implications. MMT advocates argue that debt payments are just a transfer from one set of people in an economy to another set of people in that same economy. This ignores the fact that for the United States, as well as many other countries, a large share government debt is owned by overseas investors. (It is estimated that about one-third of US debt was held by foreigners as of Dec 2018.) Interest payments to those investors reduce the income flowing to U.S. residents, making Americans less well off. And to the extent that the debt service will be borne by our descendants, it represents a redistribution from future generations to those alive today. This would be justifiable if today’s spending raised income and living standards in the future, as would be the case with infrastructure or climate change reduction/mitigation; but this transfer from our children and grandchildren to the present generation is less defensible for spending with only short-term benefits.

What this Means:

MMT’s prescription for the aggressive use of fiscal policy to promote full employment is not inconsistent with conventional macroeconomic analysis, which supports the robust use of countercyclical deficit spending to buffer downturns, especially when monetary policy is constrained by the zero lower bound on the nominal interest rate. However, contrary to MMT doctrine, there are very real constraints on the government’s use of deficit spending. First, using sustained monetization (“printing money”) to finance deficits, a core principle of MMT, invariably creates inflation. Second, the reliance on tax hikes or spending cuts to quell inflation is highly unrealistic, given politicians’ extreme aversion to fiscal austerity, not to mention the lags inherent in the budgeting process. And third, MMT ignores the fact, that above a certain level, deficit spending will contribute to an ever-rising ratio of debt to GDP, whose costs will eventually be borne by future generations.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.