The Need for Increasing Private Sector Funding of Climate Solutions

University of California, Santa Cruz

The Issue:

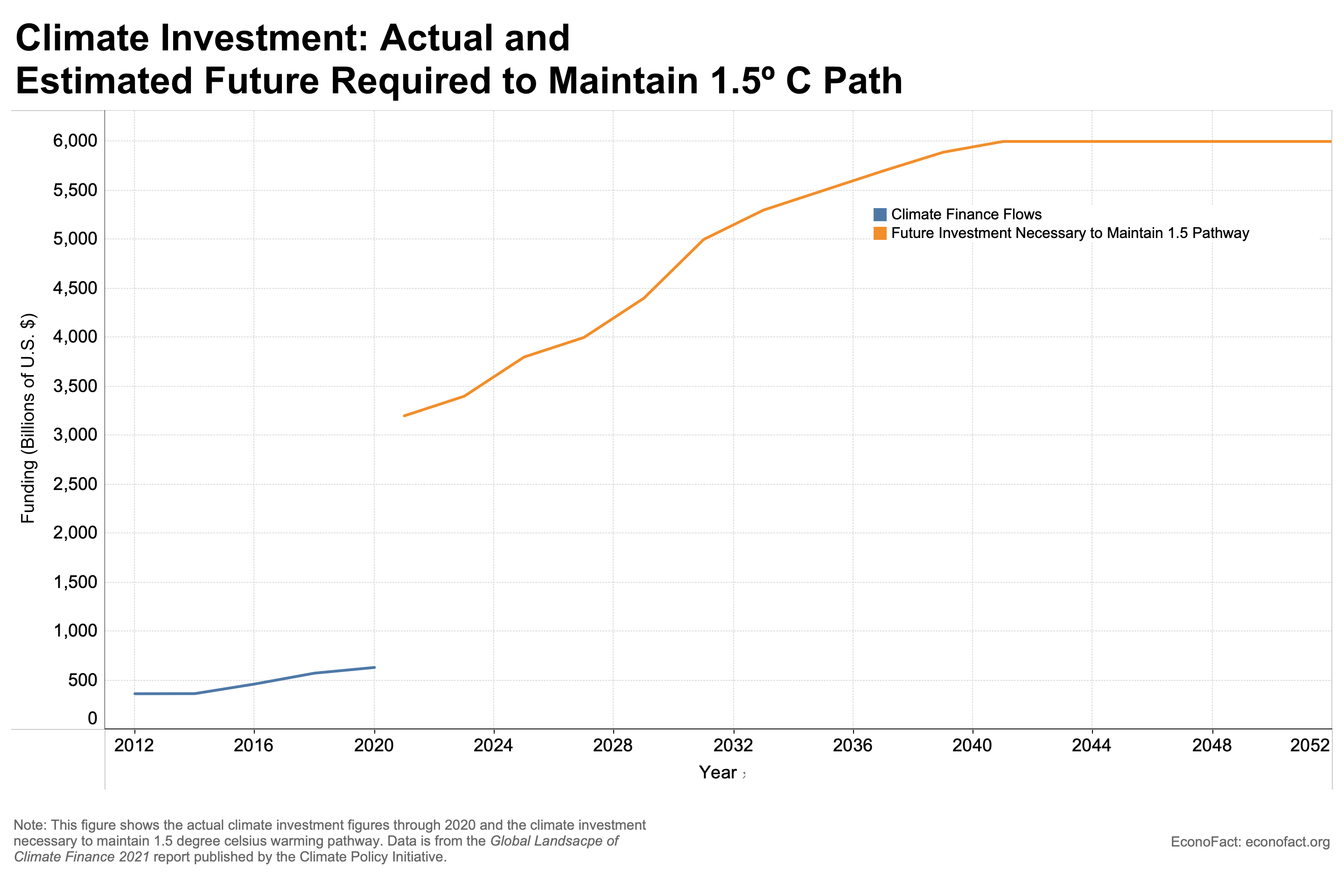

Many of the mitigation solutions needed to limit further climate change by reducing greenhouse gas emissions already exist. There are also many existing strategies to protect people, property, and nature from the damages that are already occurring and are likely to get worse, so-called “adaptation solutions” — such as fire and flood abatement strategies. However, the widespread implementation of both of these types of solutions needs a substantial amount of funding: about 4.35 trillion dollars annually by 2030, according to estimates from the Climate Policy Initiative. This is a 7-fold increase compared to the current worldwide level of spending. It is unrealistic to expect that governments and charities can increase their climate spending this much, thus increasing participation of the private financial sector is necessary.

Global financial markets could finance a much higher share of climate solutions, but barriers need to be overcome.

The Facts:

- The most up-to-date estimates agree that current climate spending is insufficient to achieve the goals of limiting climate change and protecting people, property, and nature from climate change effects. The Climate Policy Initiative estimates that annual global spending on climate solutions needs to range between 3 and 6 trillion USD in the next 20 years. Yet In 2021, global spending on climate mitigation was $632 billion (see chart).

- Current climate mitigation and adaptation funding comes from multiple sources: national governments, international development agencies, local governments, private corporations, households, and non-profit organizations. A little over half of the funding for climate solutions comes from public sources (an estimated $321 billion US in 2019/2020), with the largest share from national and international organizations, which are funded by national governments. The expansion of these public sources is limited, with government budgets stretched over multiple goals and depleted by the pandemic-related expenses of the past years.

- Private sector participation in funding for climate solutions made up 49% of total climate finance in 2019/2020, according to estimates from the Climate Policy Initiative. During 2019 and 2020, corporations, banks, institutional investors, households, and other private actors taken together provided an average of USD 310 billion per year. Corporations and commercial financial institutions together accounted for 80 percent of private climate spending —which was largely targeted towards clean and renewable energy sectors and low-carbon transport. Households made up the third largest share of private sector contributions, primarily with investments in battery electric vehicles and in the deployment of small-scale solar panels. Private sector financing is especially small in adaptation investments providing only about 2% of funding (see page 26).

- Overall, investment from the financial sector in climate solutions is very limited. Global financial markets have great potential to make a dent on the financing of climate solutions given their size: they are large, with assets under management of financial institutions exceeding $100 trillion. To meet climate finance goals only about 5% of the global assets under management would need to be directed to these goals. While some progress has been made in divesting from sectors that contribute to greenhouse gas emissions through various global initiatives, divestment from greenhouse gas exposures is not the same as investment into climate solutions. In 2019-2020 funding from commercial financial institutions was only $122 billion, or less than 20% of the total spending.

- There are barriers to financial sector investment in climate solutions that have to do with the nature of climate solutions. In the case of climate mitigation funding, these can be summarized as “tragedy of the commons” and “tragedy of horizons.” Tragedy of the commons describes a situation in which a common resource (such as clean air) is depleted because each individual only takes their own interests into account. Investors are more likely to fund projects that increase greenhouse gas emissions when they do not have to directly bear the cost of the resulting pollution. When applied to the financing of climate solutions, the tragedy of the commons occurs because while investment in climate solutions provides benefits to society overall, private investors only directly receive a portion of the benefits. The problem results in insufficient investments by individuals and companies in reducing greenhouse gas emissions because the benefits of such actions are global. Tragedy of horizons reflects the fact that the investment in climate solutions needs to be made as soon as possible, but the benefits of such investments will only pay off in the distant future. Moreover, benefits of climate investment take the form of avoided losses rather than cash flow. As former Governor of the Bank of England, Mark Carney, put it “The catastrophic impacts of climate change will be felt beyond the traditional horizons of most actors – imposing a cost on future generations that the current generation has no direct incentive to fix. That means beyond the business cycle, the political cycle, and the horizon of technocratic authorities.”

- In the case of climate adaptation solutions an important barrier is the very localized nature of needed investments. Adaptation includes measures such as safeguarding agriculture to adjust to changing local conditions, making infrastructure resilient to the particular risks in a given area, and managing the local impacts from rising seas. Those facing the highest climate risks are often those with the fewest means to tackle the daunting costs: there is a disproportionate need for adaptation funding in lower-income countries and in lower-income communities in advanced economies (see here).

- These barriers can be overcome. Markets for carbon offsets and cap-and-trade schemes (such as the Emissions Trading Scheme in the European Union) help overcome the tragedy of the commons problem by making polluters pay for their emissions. Government loans and guarantees, such as those provided in the U.S. Inflation Reduction Act (IRA) for reducing methane emissions, can help firms working on reducing greenhouse gas emissions to access conventional loans. Other approaches include financial instruments that combine government and private funding (public-private partnerships), such as debt-for-nature swaps which help highly indebted countries reduce their debt burden in return for committing to invest more in nature conservation. Finally, new financial technologies simplify crowdfunding of climate finance so that even small investors can contribute to high-value projects.

- Investment in adaptation is especially needed for the Global South. The United Nations (UN) Environmental Program finds that international adaptation funding directed to developing countries, which are disproportionately exposed to climate change hazards, was just $29 billion in 2020, well under the estimated need of $71 billion annually (see here). Nearly all these funds come from public organizations which limits the potential growth in these investments. Given that many adaptation projects protect private property and business interests (such as tourist attractions and facilities and commercial properties, often owned by multinational companies with substantial amounts of funds), it should be possible to find ways for the multinationals that benefit from adaptation projects to contribute their fair share.

- Private financial flows to lower-income economies could be risky, but these risks are less applicable to climate finance and could be mitigated. A long history of “North-South” financial flows teaches us that they come with risks of sudden reversals, so should we worry about such risks for private climate funding? “Sudden stops’’ in private capital flows were historically driven by dollar-denominated short-term debt funding such as bank loans and bonds. In recent years, we have observed more equity inflows to developing countries that are denominated in the currency of the country and are less likely to experience sudden stops. Climate investments, for reasons discussed, need to be longer term, more “patient” investments and therefore are less likely to contribute to such reversals. That said, any complex financial instruments designed to fund climate solutions need to include provisions to reduce such risks.

What this Means:

The impacts of climate change are already felt in many regions of the world in the form of floods, droughts, extreme storms, and rising summer temperatures. These pose risks to the lives and livelihoods of people worldwide, especially to vulnerable low-income communities that lack physical or financial protection from such events. Given the limited sources of public funds, increasing the participation of private funds in climate finance offers an important avenue for meaningfully addressing issues raised by climate change. Because of their size, this is particularly true for financial institutions. The goal of financial institutions is to maximize returns on their investments, so what can be done to incentivize them to invest in climate solutions? Government policies such as loan guarantees in the Inflation Reduction Act are an example of how government finances can be leveraged to help companies that work towards climate change mitigation obtain commercial loans. Consumers and individual investors can also demand that their financial institutions disclose not only their exposure to high-emission companies but also their loans to and investments in climate solutions.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.