The Resilience of State and Local Government Budgets in the Pandemic

University of California, San Diego

The Issue:

The resilience of state and local government budgets has been one of the great surprises of the COVID-19 pandemic. The spring of 2020 gave rise to warnings about the strains these budgets would face as the pandemic cut short important sources of revenue while creating new health spending and pandemic mitigation needs. Predictions from the pandemic’s early days were dire, with estimates of revenue shortfalls approaching as high as $1 trillion. By the spring of 2021, however, many states were awash with surplus cash. How did the predictions end up being so off target? And, are there any lessons for future downturns?

Predictions from the pandemic’s early days were dire. By the spring of 2021, however, many states were awash with surplus cash.

The Facts:

- State and local governments play an important role in the economic landscape of the United States during normal times and this was heightened during the pandemic. Roughly 20 million workers were employed by either a state or local government in 2019, just prior to the pandemic. Nationwide, their direct expenditures amounted, in total, to nearly $4 trillion, or just under 19 percent of Gross Domestic Product. State and local governments play crucial roles in the delivery and financing of education, the maintenance of transportation infrastructure, and the administration of the social safety net. As pertains more specifically to the COVID-19 pandemic, state governments have an important role through their participation in the Medicaid and CHIP programs, while both state and local governments were key players in the acquisition and/or the delivery of personal protective equipment, COVID-19 tests, and COVID-19 vaccines, as well as in the deployment of COVID mitigation measures in government offices and schools.

- Significant shortfalls in the budgets of state and local governments were projected at the pandemic’s outset. April 2020 revenue data painted a dire picture, with state tax receipts for the month coming in nearly $61 billion, or 49%, lower than in April 2019. Notably, however, the picture painted by April figures was misleading in that many states had, like the federal government, extended their tax filing deadlines; some of the missing revenues had not disappeared, but had been deferred to future collections. Amidst these early uncertainties, some analysts projected budget shortfalls approaching $1 trillion for state and local governments combined or $555 billion for states alone over fiscal years 2020-2022. These estimates were based on unemployment forecasts from the Congressional Budget Office and the historical relationship between budget outcomes and state unemployment rates. States themselves forecast considerable stress in their FY 2021 budgets. An arcane feature of state budget procedures is that in 46 of the 50 states, the fiscal year begins on July 1st. Consequently, the revenue forecasts underlying states’ budgets must be finalized by early spring, in time for state legislatures to complete their deliberations. This meant that revenue forecasters had to do their work during a period of tremendous uncertainty. A July 2020 analysis of state revenue forecasts projected that state governments alone would see $200 billion lower revenues across the 2020 and 2021 fiscal years as compared with their pre-pandemic forecasts.

- The possibility of state and local government shortfalls during a pandemic-induced economic downturn posed a considerable policy concern. The fact that U.S. states, along with many local governments, operate under balanced budget requirements is a perennial concern during recessions because the threat of deficits creates a need for tax increases and reductions in service provision at the worst time, namely when economic conditions are fragile. Indeed, research has found that federal aid to state and local governments saved jobs at relatively low cost during the Great Recession. Despite the 2009 American Recovery and Reinvestment Act’s more than $200 billion in aid to state and local governments, however, neither state nor local government employment returned to its 2008 level until 2019. Threats to service provision were all the more worrisome during the pandemic due to the role of state and local governments in delivering vital public health services, including vaccine distribution and administration.

- In response to concerns about the budgets of state and local governments, the federal government legislated nearly $900 billion in fiscal assistance across four major pieces of relief legislation. These included the March 2020 CARES Act, the March 2020 Families First Coronavirus Response Act (FFCRA), the December 2020 Coronavirus Response and Relief Supplemental Appropriations Act (CRRSAA), and the March 2021 American Rescue Plan Act (ARPA) (for analysis of how fiscal relief was distributed, see here). In terms of fiscal assistance, the last of these pieces of legislation, namely the ARPA, was by far the largest with its $500 billion in aid for state and local governments including school districts.

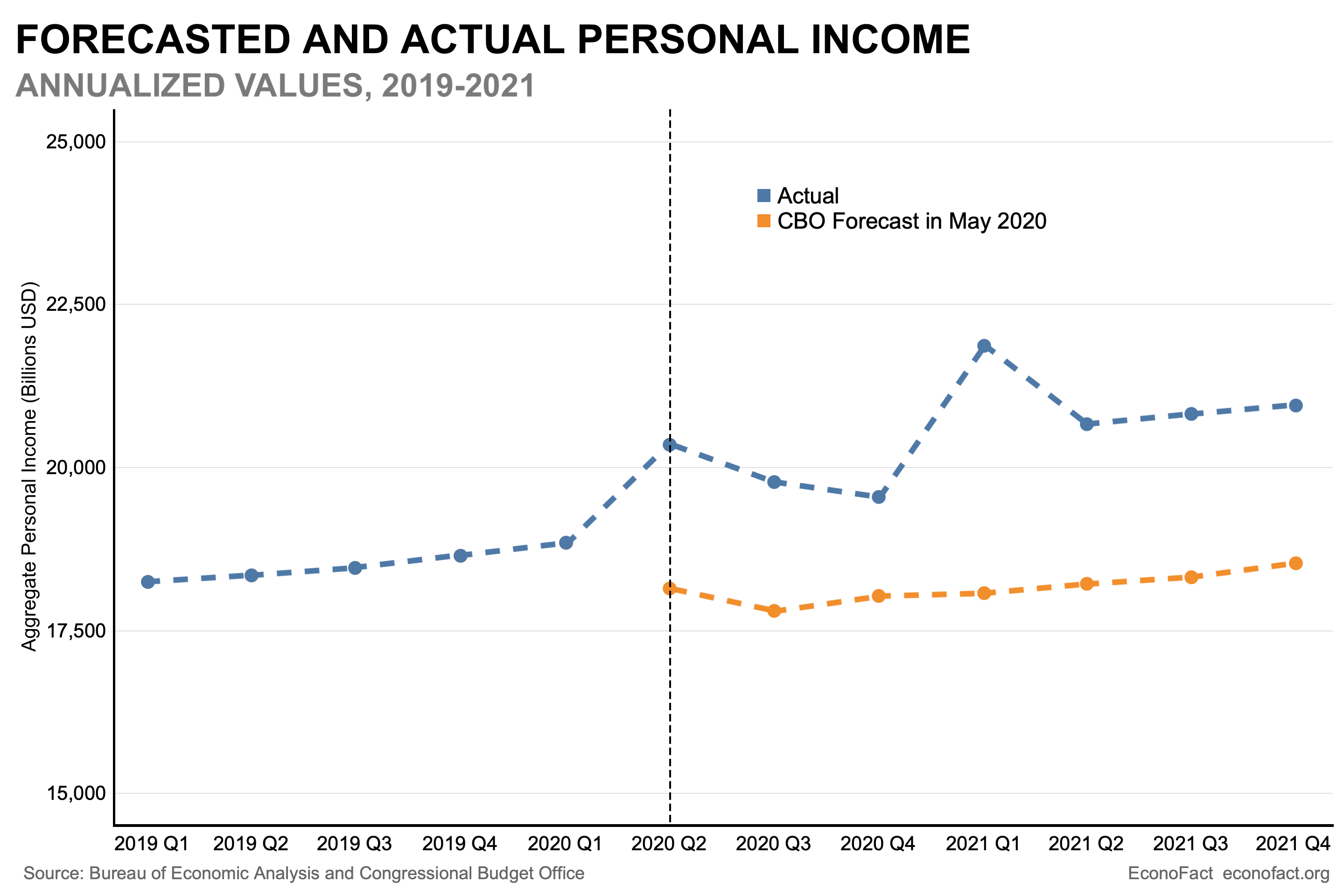

- How much did state and local governments actually need? This is hard to say, though the answer proved to be far less than the early projections. A first factor behind this development lies in the fact that the economy performed better than the Congressional Budget Office and other forecasters initially expected. In May 2020, the Congressional Budget Office forecast that the unemployment rate would average 9.3 percent in 2021. The reality for 2021 was, surprisingly, an average unemployment rate of 5.3 percent. Similarly, CBO initially thought the pandemic would lower economy-wide income by roughly 5 percent relative to its pre-pandemic trend. In fact, stimulus payments, enhanced unemployment insurance benefits, and an unexpectedly resilient economy led incomes to rise, on average across the pandemic’s first year, relative to pre-pandemic forecasts (see chart below).

- Early forecasts of state budget shortfalls suffered from several conceptual issues. Employment proved to be a less reliable predictor of tax revenues during the pandemic than during more typical recessions. This was due in large part to the fact that the pandemic’s effects on employment were concentrated in low-paying sectors whereas more typical recessions have negative impacts on industries and occupations across the entire earnings distribution. As a result, a 1-percentage point increase in the unemployment rate translated into a smaller decline in states’ tax bases than it typically would. Estimates of revenue shortfalls that focused on forecasts of the tax bases themselves thus produced smaller, and ultimately more accurate, estimates than forecasts based on the unemployment rate (see here, here, here, and here). A second issue is that the fiscal needs of the states and aid directed towards households are intertwined. More specifically, federal aid to households and businesses translated, in some cases, into higher taxable incomes. Further, by supporting household’s expenditures, the federal government’s broader pandemic relief packages supported states’ sales tax collections. Aid to households and aid to governments thus served an overlapping purpose, such that generous aid to households made less fiscal assistance to state and local governments necessary. A third issue relates to sales taxes. The industries hit hardest by the pandemic tend to involve services that are not included in many states’ sales tax bases, while consumer durables, towards which spending shifted, are central to states’ sales tax bases. (For a summary of these issues see page 45).

- Heavy reliance on property taxes protected local governments from extreme revenue shortfalls. A unique feature of local governments is the extent of their reliance on property taxation. In 2019, for example, property tax revenues accounted for 72 percent of local governments’ tax revenues and 46 percent of their total own-source general revenues (see here). By contrast, property taxes make up less than 2 percent of own-source revenues of any kind for state governments. The property tax has historically been more stable than other revenue sources, including during the Great Recession and its associated housing crisis. Local governments thus had less reason to fear the pandemic’s effects, at least in the short term, than did state governments. Despite initial fears of a wave of evictions, which were forestalled by a federal eviction moratorium, housing prices were resilient. Indeed, house prices rose substantially during the pandemic, thus buoying rather than contracting local property tax bases to the extent that assessments have been updated.

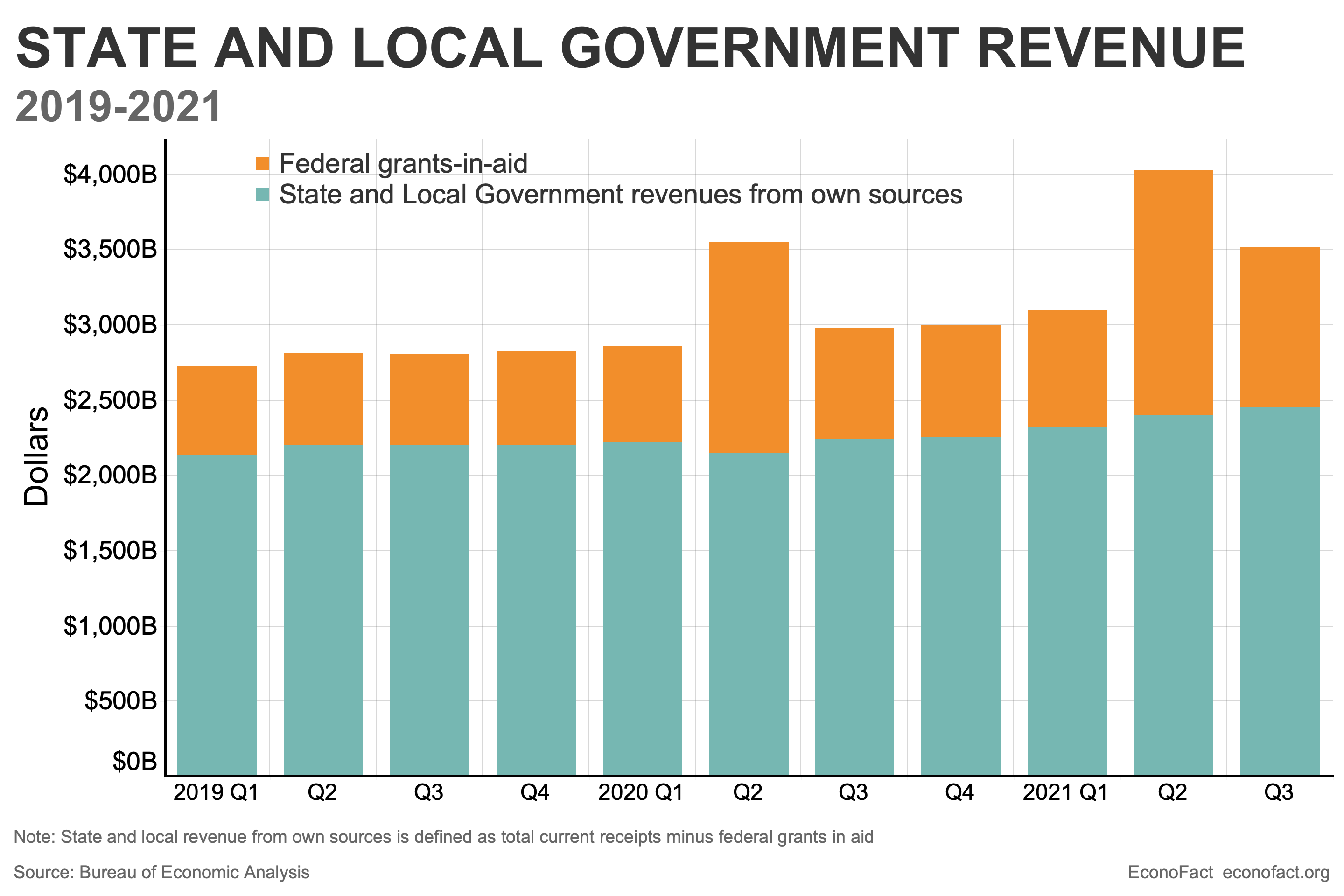

- The fiscal condition of state and local governments proved far less dire than initially forecast. In spite of the pandemic shutdown and historic rise in unemployment in March of 2020, revenue for state and local governments did not crater (see top chart). Remarkably, a fall 2022 report from the National Association of State Budget Officers found that combining the 2020 and 2021 fiscal years, total general fund revenues ultimately came in 2.2 percent higher than pre-pandemic forecasts. Importantly, this estimate does not include the revenues states receive as transfers from the federal government. While revenues proved resilient, state and local governments also faced unanticipated expenditures stemming from the pandemic. The scale of these expenditures remains difficult to estimate. Taken together, any increases in expenditures, an unexpected increase in revenues, and nearly $900 billion in federal fiscal assistance have left state and local governments with considerable surpluses. These unexpected surpluses allowed some states, which include California, Florida, Georgia, and Michigan, to enact a 4th round of stimulus checks. Additionally, around one-third of the states enacted tax cuts last year and just over half enacted either a tax cut or an expansion of tax credits (see here). A substantial share of federal assistance dollars are earmarked towards schools and transportation systems, but there are many possible ways for governments to take advantage of these funds and the ultimate uses of these dollars are not yet known on a nationwide basis. The uses and effectiveness of pandemic fiscal assistance dollars will be an important object of research over the coming years.

What this Means:

The nature of the pandemic recession introduced unprecedented uncertainty into the process of estimating both revenue inflows and expenditure needs for states and local governments. The federal government provided state and local governments with unprecedented flows of aid that, in the end, substantially exceeded states’ needs. This dynamic helps explain why, despite initial fears of fiscal distress, states have more recently contemplated issuing fourth stimulus checks, reductions in tax rates, and gas tax holidays. The overshooting of federal fiscal assistance may reflect a hazard of relying primarily on ad hoc relief packages in response to crises. Had the American Rescue Plan’s assistance package reflected the resilience of household incomes or the unemployment rate’s rapid improvement, total federal aid would have overshot state and local needs far less. This points to a potential benefit of tying aid to economic conditions through formulas, ideally legislated in advance of a given crisis, so that aid adapts automatically to conditions on the ground. An automatic stabilizer of this sort would have the benefit of easing the strains on Congress’s bandwidth as it responds to other pressing dimensions of complex crises, like the need to erect testing infrastructure and spur vaccine production in the context of pandemics. Automatic stabilizers have the further benefit that they are responsive to changes in need even in the face of Congressional inaction.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.