When Do Stocks and Bonds Move Together, and Why Does it Matter?

Harvard University, Harvard Business School and Harris School of Public Policy of University of Chicago

The Issue:

For most of the past 20 years stock prices and bond prices tended to move in opposite directions. This made buying 10-year Treasury bonds a good hedge for investors seeking to protect their portfolio from declining stock prices. But when the Federal Reserve started raising interest rates to fight inflation in 2022, the prices of stocks and bonds fell simultaneously. This was more akin to the norm during the 1980s and 1990s when stock and bond prices tended to rise and fall in tandem. Recent research in economics has looked into the co-movement of stocks and bonds and what it indicates about the risk characteristics of US Treasury bonds — as well as market expectations of the U.S. macroeconomic outlook.

Long-term Treasury bonds have hedged portfolios against falling stock prices for the past 20 years. But stocks and bonds don't always move in opposite directions.

The Facts:

- While US Treasury bonds have very little risk of default, they are not risk-free assets. Changing interest rates have a substantial short-run impact on the prices of long-term US Treasury bonds, as many investors regularly experience. Rising interest rates drive down the price of existing bonds (and the inverse is true of falling interest rates). Even investors who hold their bonds to maturity can suffer losses in real terms if inflation is unexpectedly high.

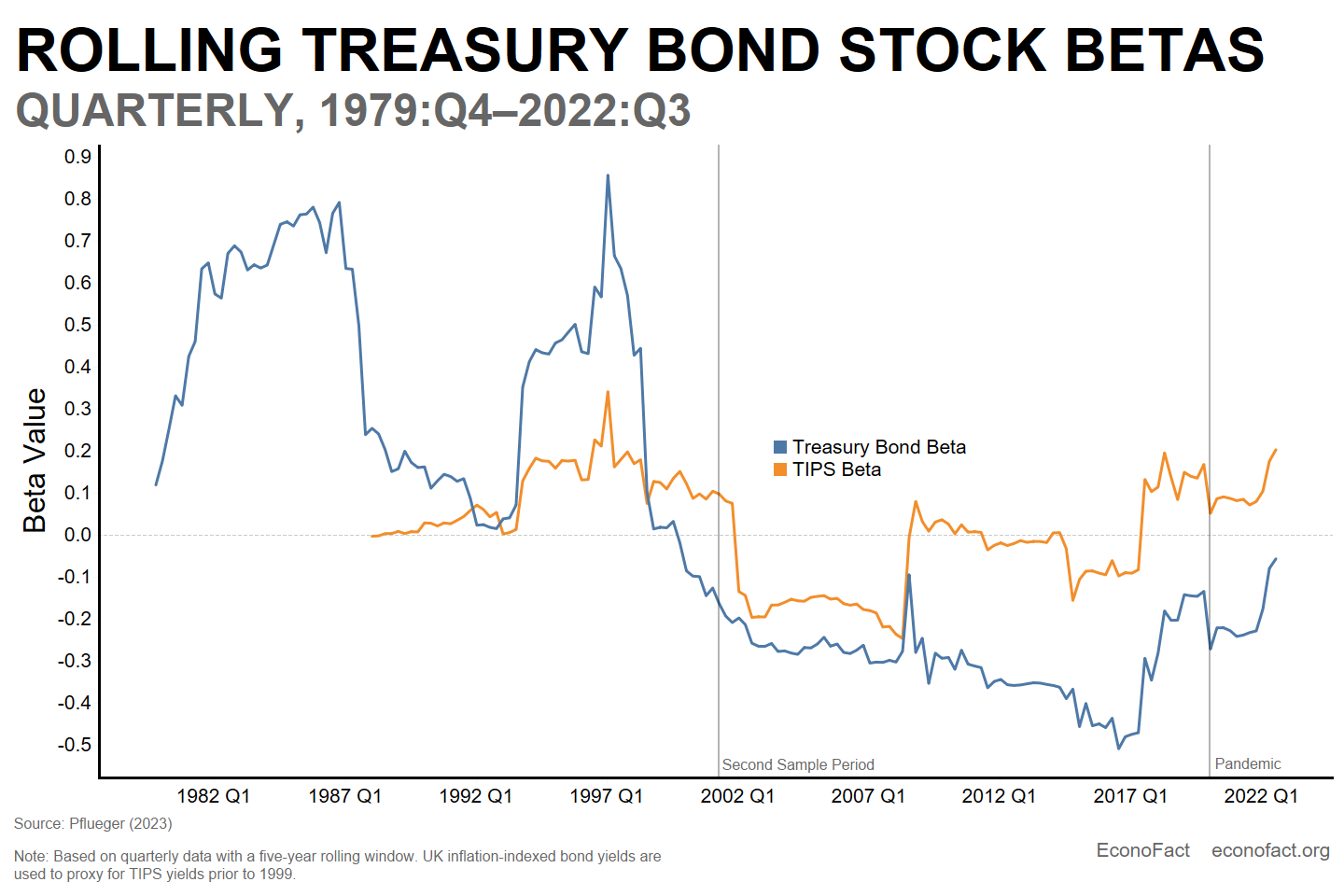

- An additional measure of the risk to holding bonds in a portfolio comes from comparing how they move relative to other assets. We can calculate Beta — the standard Capital Asset Pricing Model measure of systematic risk — for long-term Treasury bonds by comparing their return with the stock market as a whole. This measure gauges the extent to which Treasury bonds move like stocks over time – or not (see chart).

- The movement of Treasury bonds relative to stocks has shifted significantly over time. During the 1980s and 1990s, US Treasury bonds had a positive Beta with stocks — when stocks went down, bonds went down; when stocks went up, bonds went up. But, around the turn of the millennium, this co-movement switched sign and became negative: bonds moved opposite stocks and served to balance portfolios. (Note that each point in the chart reflects five years of quarterly data, capturing how much bonds moved with stocks over the previous five years).

- The shift in how bonds move with stocks is linked to the nature of inflation. The nominal interest rates that drive Treasury bond prices reflect both inflation expectations and real interest rates — when these are high, bond prices tend to be low. Stocks move with the strength of the economy — when the market expects weaker growth and decreasing company profits in the future, stock prices go down. Thus, a scenario in which high inflation and high real interest rates occur simultaneously with a recession is one in which Treasury bonds and stocks are likely to both go down. Campbell, Sunderam, and Viceira (2017)) link changes in bonds’ Betas to the changing nature of inflation in the economy, and formally model the implications for short- and long-term interest rates over time. Long-term interest rates are central in the economy, for example mortgage rates tend to rise when long-term bond rates are higher. When bonds are risky and move like stocks, investors will naturally charge a higher long-term interest rate.

- The changing nature of shocks hitting the economy and the Federal Reserve’s stance towards inflation offer a potential explanation for when stocks and bonds tend to move together. In the early 1980s, the Fed’s monetary policy prioritized fighting inflation at a time when inflation peaked at over 14% even though this led to disruptions in economic activity and higher unemployment. In situations like this, or if inflation rises because there's an energy crisis or a war, the Fed will choke off inflation by raising interest rates even if it causes a recession. That's bad for bonds and bad for stocks, and the prices of both will decline, resulting in a positive bond Beta. In this century, until very recently, it's been different. The Fed had good credibility regarding its commitment to fighting inflation and there were no major supply shocks moving inflation expectations. Under those conditions, if there's a recession, the Fed will cut interest rates to stimulate the economy. The recession is bad for stocks. Low interest rates are good for bonds. Bond and stock prices move opposite one another, resulting in a negative bond Beta. Pflueger (2023) provides a formal model showing that bonds’ Betas should be expected to be most strongly positive when supply shock-driven inflation is present and the Fed is anticipated to risk a recession in its efforts to stabilize inflation.

- The perception of bonds as “safe assets” can play a reinforcing role under conditions in which bonds are used as a hedge to stocks for market downturns. Campbell, Pflueger, and Viceira (2020) ask whether the appealing safety feature of Treasury bonds after the year 2000 arose because of changes in the cyclical behavior of inflation and real interest rates, or because investors tend to flee to the safety of bonds when there is bad news. The answer is both, and they are connected. Low and stable inflation in the early 21st Century made nominal bonds a safe haven, to which investors fled when there was bad news, driving up their prices and further improving the hedging value of bonds. But this amplification mechanism rings a cautionary note for investors today who are wondering about the continued safety of bonds since even a small change in the macroeconomic environment may be sufficient to drastically change bonds from safe-haven assets to risky assets.

- Do current conditions — high inflation, war in Ukraine, high and volatile energy prices — indicate that the U.S. economy is likely to move back to the regime of the 1980s and 1990s when stocks and bonds moved together? While it is likely too early to tell, the Betas of bonds suggest that while the current moment has some similarities with the 1980s and 1990s, there are also important differences. The recent data show a positive Beta for TIPS – bonds whose prices are linked to inflation and which, unlike regular Treasuries, do not suffer when inflation goes up. Moreover, the Beta of regular Treasuries (or nominal bonds) has remained below the Beta of TIPS. Both the nature of shocks – supply shocks as in the 1980s or demand shocks as in the 2000s – and the perceived monetary policy response play a role for the economy and the Betas of bonds. Pflueger (2023)’s model suggests that the recent empirical patterns can arise when the economy is subject to strong inflationary supply shocks, like those experienced in the 1980s, but in contrast to the 1980s, markets expect the Fed to achieve a “soft landing”. The most recent increase in both nominal and inflation-indexed bond Betas into positive territory occurred just as the monetary policy response strengthened, further underscoring the importance of monetary policy for bonds’ Betas.

What this Means:

The co-movement of Treasury bonds and stocks is an important indicator for both policy makers and for long-term investors. A positive co-movement between nominal Treasury bonds and stocks, as in the 1980s, means that nominal bonds amplify the volatility of stock investors’ portfolios. This pattern tends to arise when investors anticipate inflation that is accompanied by a recession, which often results from an adverse supply shock – driving up prices – and a quick and energetic interest rate hike – tipping the economy into a recession. The importance of Treasury bond-stock co-movement has been increasingly recognized in policy circles as an important policy indicator of supply-driven inflationary pressures and the risk of a monetary policy-induced stagflation (see for example the Economic Report of the President, March 2023, pp.61-62). Policy makers also recognize the importance of bond-stock co-movement for the appeal of Treasury bonds to investors and the term premia they demand to hold these bonds — the government would find it more expensive to borrow if long-duration Treasury bonds are no longer seen as useful hedges against equity risk. So far, the post-pandemic risks of Treasury bonds look markedly different from the 1980s despite disruptions to energy supply, suggesting that investors are pricing in a less aggressive Fed response and a softer landing. Going forward, the risks of nominal Treasury bonds will provide a useful tool to track market expectations of stagflation risk and its sources.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.