When Should the Fed Stop Raising Interest Rates?

Former EVP and Director of Research, Federal Reserve Bank of Boston

The Issue:

Since March of 2022, the Federal Reserve has raised interest rates briskly, hoping to reverse a historic rise in inflation, moving the Federal Funds Rate from near-zero to the current 4.75-5%. At one-quarter percentage point, the ninth consecutive rate increase in March 2023 was less than what had been widely anticipated just a few weeks earlier, likely in recognition that the failures of Silicon Valley Bank and Signature Bank could lead to a retraction in bank credit. Nonetheless, the Fed’s policy statement after the March meeting still indicated that “…some additional policy firming may be appropriate”. But the Fed is also facing the very real risk that its efforts to lower inflation will cause a recession. Is the Fed overreacting with ongoing rate increases? Does reducing inflation require substantial increases in unemployment? To answer these questions, we need to understand what has caused inflation’s rise, what is causing its more recent decline, how restrictive is current and prospective Fed policy, and how much monetary policy tightening is needed to appropriately balance legitimate concerns about inflation against concerns about rising unemployment.

The risk of a hard landing has risen substantially, largely due to tighter Fed policy.

The Facts:

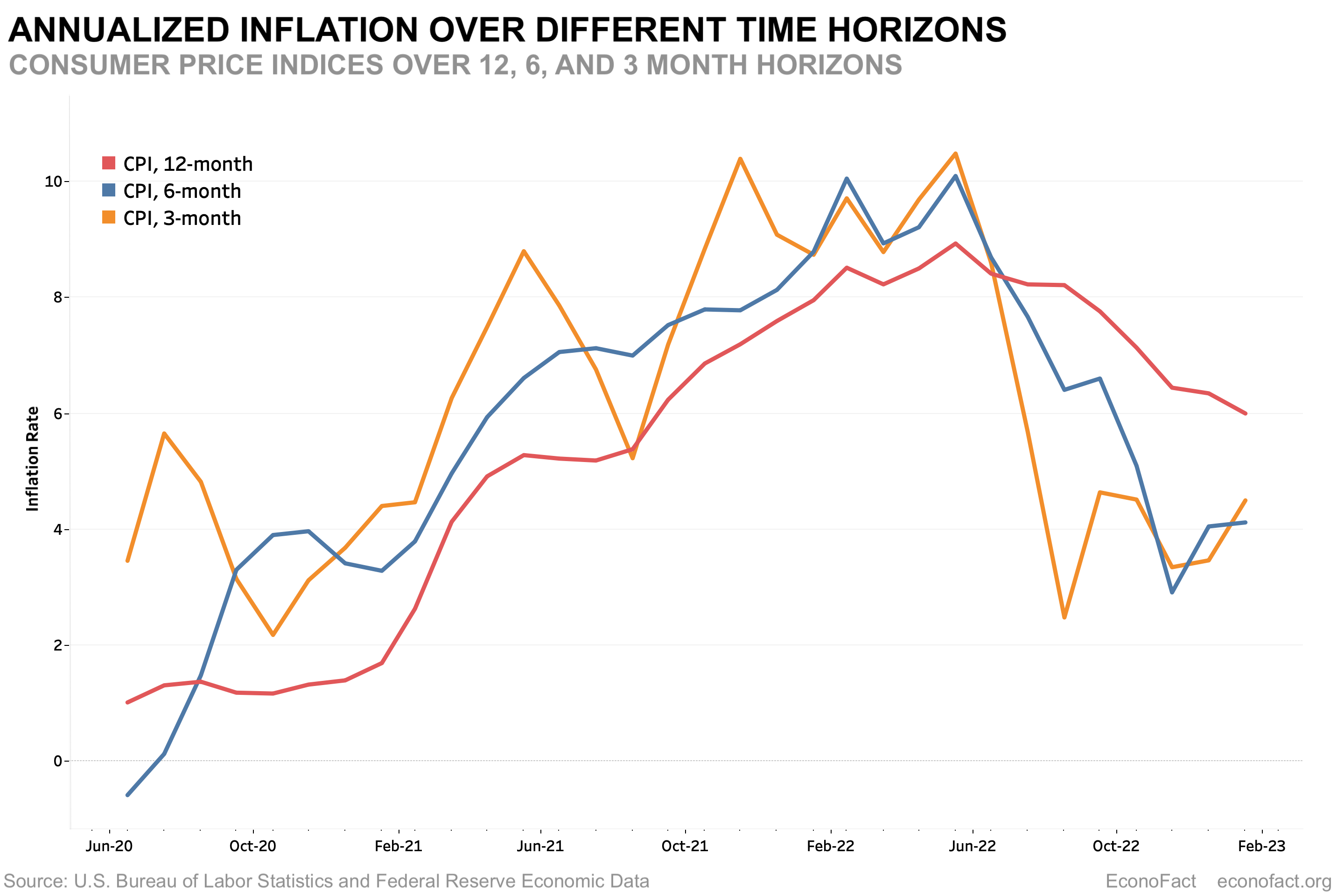

- After reaching the highest rates in decades, inflation has been on the retreat. Inflation over the past 12 months, as measured by the CPI, was more than 9 percent in the summer of 2022 – the highest rate since 1981. It has since retreated to about 6 percent (5 percent for the Fed’s preferred inflation measure, the personal consumption expenditures chain-type price index, or PCE) – lower, but still well above the Fed’s target rate of 2 percent. The twelve-month inflation rates compare current prices to those from one year ago and are thus arguably too backward-looking. Inflation over the past 3 to 6 months has declined to somewhere between 2.5 and 4.5 percent (at an annual rate), depending on the month (see chart above). These more recent readings probably better reflect the current underlying rate of inflation.

- Most agree that COVID shutdowns led to transitory supply constraints. In the first half of 2021 many people thought that inflation would come down fairly quickly with the easing of these constraints. But “transitory” inflation turned out to be longer-lived than many expected. By late-2021, the notion that inflation would ease within months was dubious — inflation by Dec. 2021 had been at or above 5 percent for six months. And it continued to rise from there. The main factors raising inflation may well have been transitory, but a cavalcade of global disruptions, including the war in Ukraine and more recent COVID responses in China, have caused more persistent increases in inflation.

- An alternative explanation is that the primary culprit behind elevated inflation is an excess of aggregate demand due to a recovered economy spurred in part by generous government support during the COVID pandemic. But we enjoyed similarly strong demand in late 2019, before the pandemic: the unemployment rate — a simple but fairly accurate indicator of demand strength — at that time was about 3.5 percent, yet the Fed’s challenge then was to raise stubbornly low inflation to its 2 percent target. A reasonable conclusion, therefore, is that as of early 2020, strong demand had at best a very modest effect on inflation, as long as supply conditions were normal. If the interpretation that inflation was caused mainly by supply constraints is correct, then that suggests that as this multitude of supply factors sort themselves out — and many already have, from autos to some building materials to airfares — the U.S. economy will be quite capable of absorbing the current level of demand without any significant inflation.

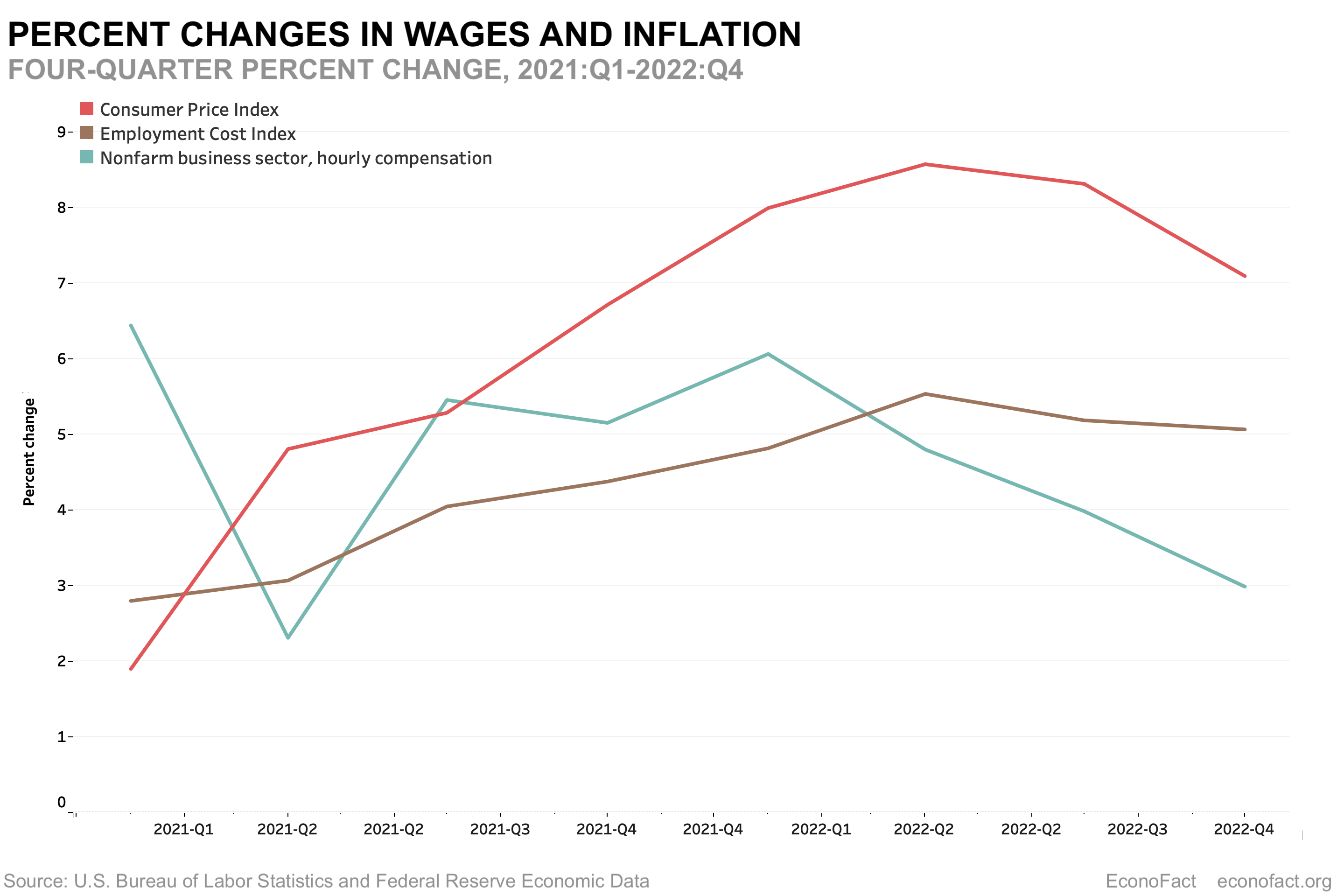

- Are rising wages and inflation expectations fueling inflation? Some suggest that rising wages will further increase inflation, possibly triggering a wage-price spiral in which higher wages drive prices higher, leading to even higher wages, and so on. Such a spiral could become even more entrenched if inflation expectations start to leap ahead of wage inflation. But to date wages have followed, not driven inflation. The chart below shows that, on average, wage gains have not matched inflation over the past few years. Instead, workers’ wages have lost ground to inflation. Thus wages have not been driving up inflation.

The situation so far contrasts with the 1970s when wage gains outpaced inflation for much of the decade. If people generally come to expect qualitatively higher inflation, even if inflation has been caused by temporary supply factors, an otherwise temporary bout of inflation could turn into something much more persistent, as it did in the 1970s. For example, if the norms for expected inflation were to shift from something low — around 2 percent — to something noticeably higher — say 4 to 5 percent — then wage earners might expect (or demand) much higher wage gains for a much longer time. In that case, wages could indeed drive inflation up. But there is little evidence to date that the prevailing norm for inflation has changed. Measures of longer-term inflation expectations — 5 or 10 years out — have remained quite stable, suggesting that people on average see this as a transitory period of elevated inflation.

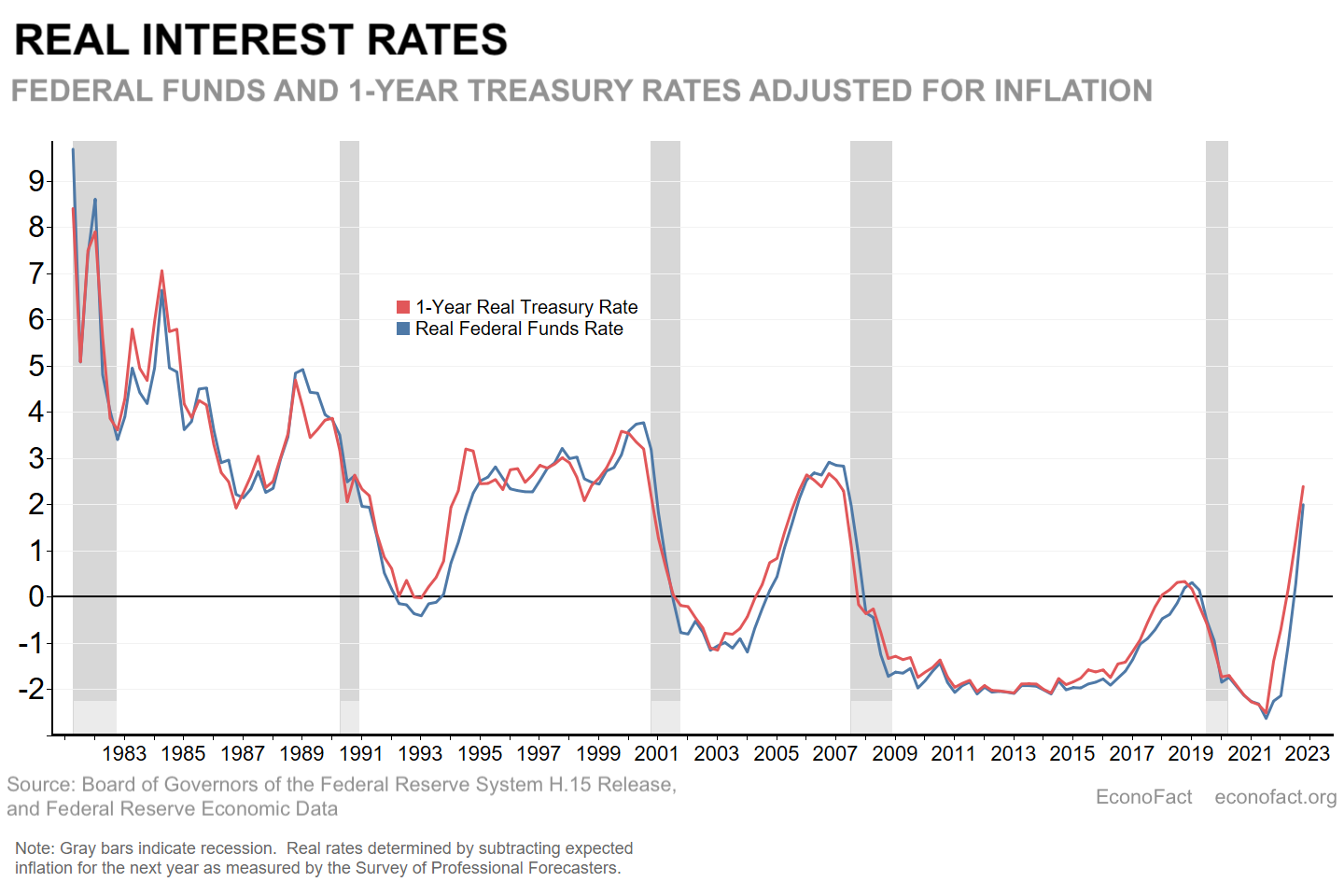

The situation so far contrasts with the 1970s when wage gains outpaced inflation for much of the decade. If people generally come to expect qualitatively higher inflation, even if inflation has been caused by temporary supply factors, an otherwise temporary bout of inflation could turn into something much more persistent, as it did in the 1970s. For example, if the norms for expected inflation were to shift from something low — around 2 percent — to something noticeably higher — say 4 to 5 percent — then wage earners might expect (or demand) much higher wage gains for a much longer time. In that case, wages could indeed drive inflation up. But there is little evidence to date that the prevailing norm for inflation has changed. Measures of longer-term inflation expectations — 5 or 10 years out — have remained quite stable, suggesting that people on average see this as a transitory period of elevated inflation. - To determine when the Fed has raised interest rates high enough to restrain the economy and inflation, one must consider inflation-adjusted or “real” interest rates. Real interest rates are the stated (so-called nominal) interest rates less the rate of inflation expected to prevail during a loan. A part of any nominal interest rate compensates lenders for the fact that repayment of the loan they extend will be made in dollars whose value has been eroded by inflation. The higher inflation is, the more of the interest rate will reflect such inflation compensation. Subtracting inflation from the nominal interest rate reveals the rate of interest earned by the lender in excess of inflation compensation. Other things equal, lenders would prefer to lend at higher real interest rates. Borrowers of course prefer lower real interest rates. Put differently, whether a particular nominal interest rate is “high” or “low,” restrictive or expansionary, depends on what rate of inflation is expected to prevail over the course of the loan. Monetary policy that sets interest rates below inflation — negative real interest rates — is stimulative because it serves as a strong inducement to borrow, spurring spending and employment. Policy that sets interest rates well above expected inflation—significantly positive real interest rates—is restrictive since it deters spending that relies on borrowing, other things equal.

- What impact have the Fed’s actions to date had on the economy and inflation? The following chart shows the history of the inflation-adjusted federal funds rate and the inflation-adjusted one-year Treasury yield, obtained by subtracting expected inflation for the next year as measured by the Survey of Professional Forecasters (SPF). As the chart indicates, real interest rates were negative well into 2022. But by mid-2021, apart from inflation concerns, the economy was doing quite well and no longer needed expansionary policy to support employment and spending. At that point the Fed was still holding short-term interest rates low and continuing to purchase Treasury and mortgage securities to keep longer-term rates low. Raising rates at that point — to 2.5 or 3%, would have served to reduce the amount of support they were providing to an already-healthy economy. As shown in the rightmost observations in the chart, with most forecasters now expecting inflation to be around 3 percent or lower by later this year, current interest rates are about two percentage points above expected inflation. By this simple measure, current Fed policy is already quite restrictive, and became about one-quarter percentage point more so after their March 22nd meeting (the data in the chart are quarterly, so the March 22nd rate increase is not reflected).

What this Means:

A year ago, the bigger risk may have been that the Fed would not do enough to contain inflation. The Fed was a bit late to the game, holding interest rates too low even as the real economy had mostly recovered from pandemic-induced shutdowns. As inflation rose to alarming levels, the Fed rapidly raised rates, exceeding three percent in late 2022, just as inflation was beginning to recede. Today, the risk of a hard landing has risen substantially, largely due to tighter Fed policy. The Fed’s movements into restrictive territory — significantly positive real rates — will affect employment and spending later this year, and inflation somewhat later. By that time, most forecasters expect inflation to have receded to three percent or below, clearly not due to the Fed’s actions. It’s time for the Fed to pause and gauge the effects of their moderately restrictive policy — or to consider reducing rates later this year, as financial market participants expect. (Futures contracts for the federal funds rate in coming months imply a high probability of rate declines later this year.) If inflation indeed normalizes as supply constraints ease, a pause or reduction would make it more likely that they achieve the “soft landing” we all desire — low inflation without a recession.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.