Why Has the Price of Gold Risen So Sharply?

EconoFact and The Fletcher School, Tufts University

The Issue:

The price of gold has jumped over 40 percent since the end of 2023, reaching $3,000 per ounce in mid-March 2025. This leap cannot be explained by a sudden increase in the demand for gold as jewelry or for its use in industrial production. Rather, it reflects the shifting demand for the yellow metal as a financial asset. Historically, gold has been held by private investors who see gold as a good way to protect wealth during inflationary periods or when there is substantial economic or political uncertainty as well as by central banks as part of their international reserves. Can shifts in these motivations explain the recent dramatic rise in the gold price?

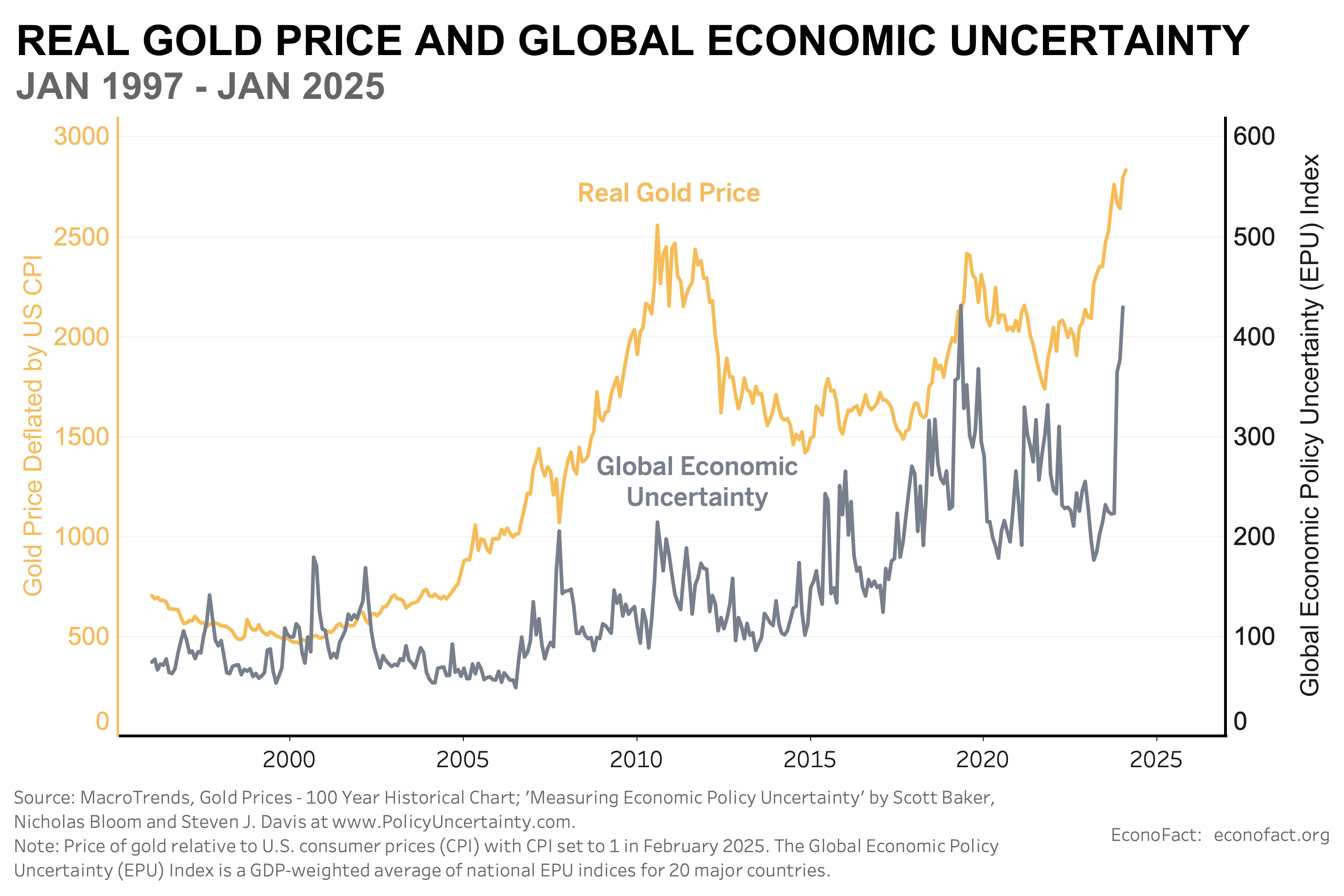

The recent spike in economic uncertainty has sent the gold price soaring.

The Facts:

- Large gold price fluctuations mainly reflect its role as a financial asset. As a commodity, gold is mined and used as an input for both industrial and consumer goods, which can imply some modest shifts in supply and demand, and hence the price of gold, over time. But gold also has a long history of being held by private investors and central banks, which can be the source of much larger shifts in gold demand. These shifts in the demand for gold as a financial asset have tended to dominate gold price movements.

- For private investors, gold offers no explicit yield, unlike bonds, which pay an annual interest rate or stocks that pay dividends. But holding gold can still provide benefits in an investment portfolio. People will purchase gold when they expect the price of gold to go up and to be able to cash it in at a higher price — although there is also a risk of capital losses in the face of a price decline. Current price swings reflect shifting beliefs about gold’s future price, and the difference between the current and future prices provides a source of speculative gain (or loss) and a possible hedge against losses from other assets. Gold-backed exchange-traded funds (ETFs), introduced in the early 2000s, substantially broadened the investor base for gold and allowed for more rapid shifts between gold and other assets in response to such shifting beliefs.

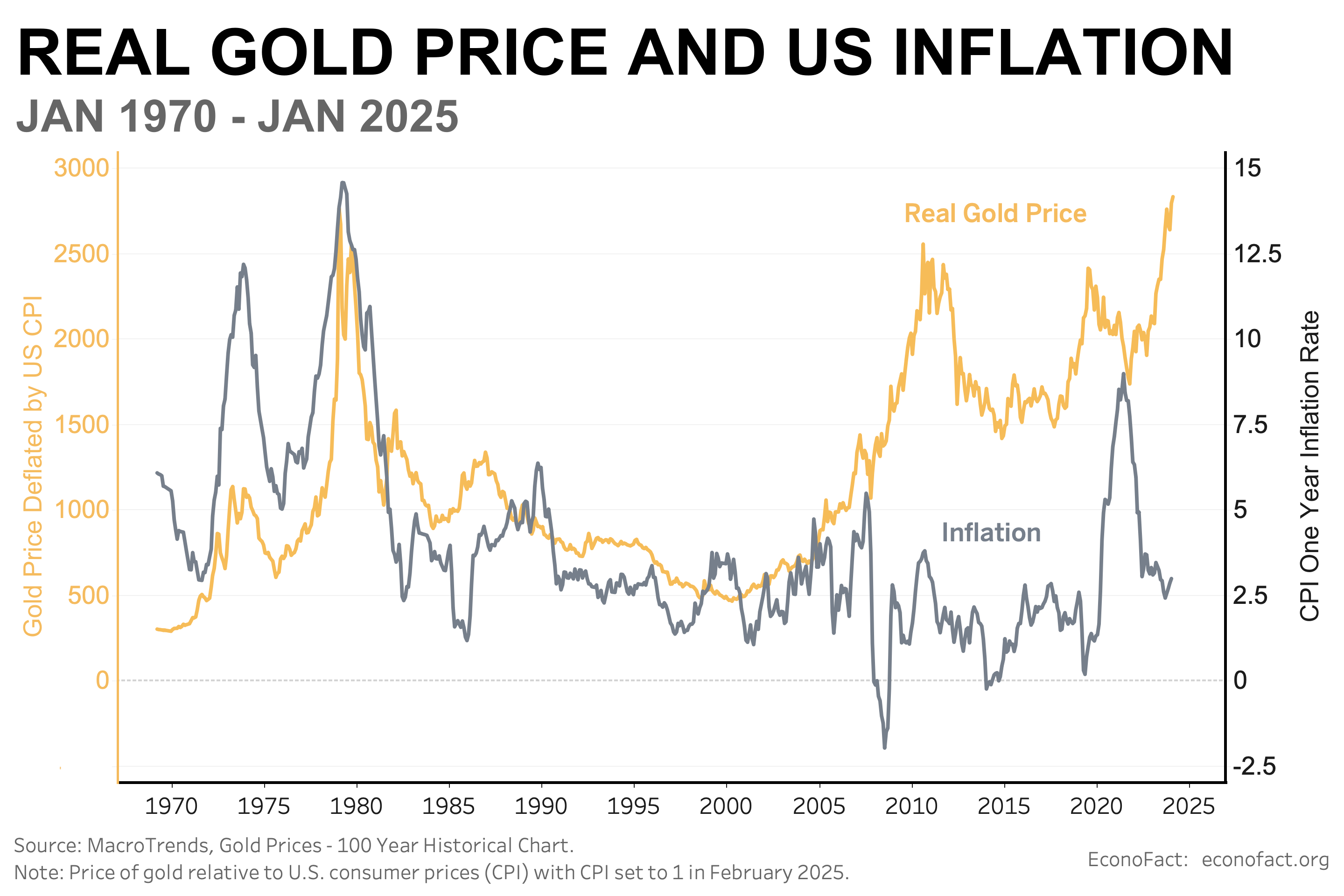

- Gold is often seen as a tool to protect against inflation. Rising inflation can undermine the value of cash and fixed-interest rate assets like treasury bonds. Holding gold protects against such capital losses in the face of rising inflation because the price of gold tends to rise as the real values of these other assets fall. This motivation is clearly visible in movements in the price of gold in the 1970s and early 1980s as inflation first surged in the wake of sharp oil price increases and then was brought back under control by monetary tightening (see chart below).

- Gold can also provide private investors with an effective hedge against other forms of risk, including uncertainty about economic prospects that can hurt the stock market. Gold is frequently viewed by investors as a “safe haven” in times of economic turmoil. A good example is the 22 percent jump in gold prices during the first six months of the COVID pandemic. At that time inflation remained below 1.5 percent but there was a major loss of economic confidence and an associated drop in equity prices. As an illustration, the figure at the top of this memo shows the price of gold and a global uncertainty index.

- While investors may value gold as a means of speculating or a hedge against risk, they must also consider the opportunity costs for holding gold as opposed to safe assets like government bonds that bear interest. When this interest yield is above the inflation rate, such bonds offer a positive real (inflation-adjusted) rate of return. In principle, the higher are real returns on government bonds, the more the sacrifice for holding gold as opposed to Treasuries and the lower will be the price of gold.

- An additional factor that may have affected the gold price is that central bank demand for gold has risen since the sanctions imposed on Russia after its invasion of Ukraine. Gold was a key component of central bank reserves from 1945 to 1973, under the fixed exchange rate system in which the prices of all major currencies were tied to the value of the U.S. dollar and the dollar was fully convertible into gold at $35/ounce. The fixed dollar price of gold was protected by large official United States reserve holdings. Other major central banks also held substantial gold reserves. The role of gold as a central bank reserve diminished after this system collapsed in March of 1973 but it did not disappear. Since 1973, major central banks continued to hold gold in their international reserves even though it was no longer required to back their currency, and in fact such holdings represented a rising share of the value of their international reserves as the gold price increased over this period. In addition, at least since 2010, the central banks of Russia and, to a somewhat lesser extent, China increased their physical holdings of gold, as part of a reserve diversification strategy out of US-dollar assets. Central bank purchases of gold dramatically accelerated after the February 2022 Russian invasion of Ukraine which led Western governments to impose sanctions on Russia, including to freeze dollar-based reserves. Since then, central banks from Poland, China, Turkey and India among others — substantially increased their gold purchases, raising aggregate central bank holdings of gold by over 1,000 tons each year, about twice the rate of central bank gold acquisitions over 2010-2021 (see here).

- Which of these factors has been driving the rapid increase in the price of gold over the past year? To disentangle these various effects, we conducted a systematic empirical analysis of the determinants of the gold price over the period 2003-early 2025 (see here for full details). This estimation essentially updates and extends an analysis published by the Federal Reserve Bank of Chicago for a sample that ended in 2021. As expected, the estimates show that the price of gold is higher when the real interest rate is lower, when inflation is higher (although this effect is not statistically significant), when uncertainty is higher, in the period after the introduction of gold-backed ETFs, and since the Russian invasion of Ukraine in February 2022.

- Based on these results, the main factor that has driven the recent surge in the price of gold is the increase in global economic uncertainty over the past year. The uncertainty index rose from fairly normal levels in early 2024 to much higher levels in November-December and has continued to rise in early 2025 to levels comparable to the peak of the COVID pandemic in 2020 (see top chart). Our results imply that this increase accounted for almost half (47 percent) of the rise in gold price over the year ending in January 2025. Some pick-up in inflation expectations from late 2024 also contributed modestly (6 percent) to the rise of gold prices in this period. We don’t see much impact from central bank purchases, which continued in 2024 and early 2025 at much the same pace as in 2022-2023.

What this Means:

Big run-ups in the price of gold have happened before. The present run-up seems most similar to that which occurred in the first half of 2020 related to the jump in economic uncertainty related to the COVID pandemic. In the present run-up, market commentary and news reporting suggests that the recent spike in global policy uncertainty is particularly reflected in the massive spike in trade policy uncertainty since November 2024. The increase in uncertainty is thus likely related to the threat of substantial tariff increases on the United States’ main trading partners and their potential impact on inflation, global supply chains, and geopolitical tensions.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.