How Safe are Private-Credit Funds?

EconoFact

The Issue:

Private credit provides a source of corporate lending that is extended outside of the banking system and is not subject to the same level of regulatory controls imposed on banks. Private-credit funds have grown dramatically over the past decade, largely funded by institutional investors but increasingly also by individual investors. However, some private-credit funds have come under stress in recent months, especially those with significant exposure to software companies, and many continue to face substantial withdrawals. This experience has raised questions about whether the boom in private credit was overextended and underlines the risks that putting money with private-credit funds may pose to individual investors. It has also highlighted concerns about whether the surge in private credit in recent years may be a source of stress for the broader financial system comparable to the fallout from the collapse of the mortgage-backed securities market before the 2008 global financial crisis.

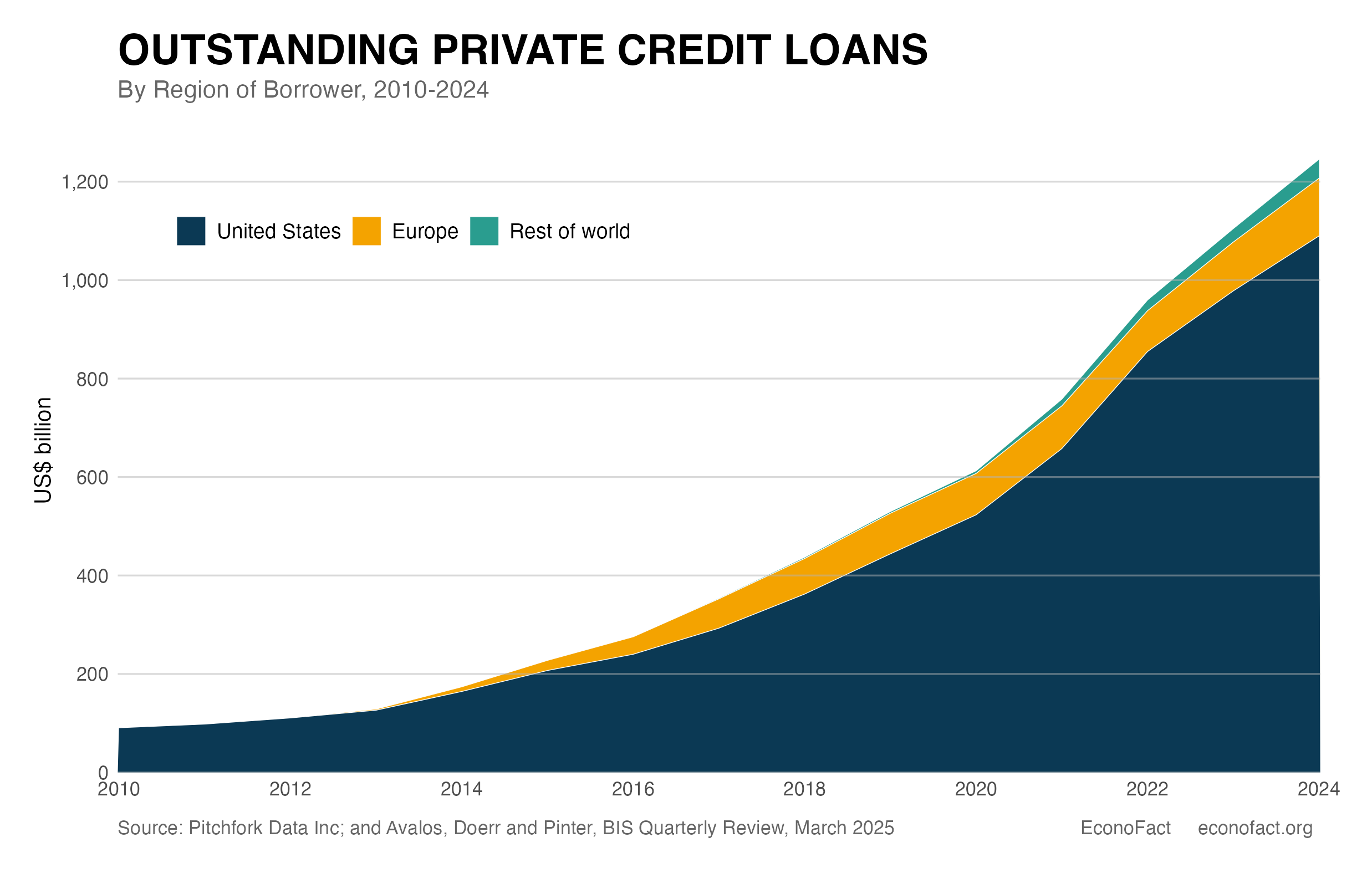

Private credit, which is not subject to the same oversight as banks, is approaching the scale of commercial and industrial loans from banks.

The Facts:

- Private credit helps to fill a particular niche in corporate finance by providing debt financing mainly to riskier middle-tier companies that have not gone public. Typically, it takes the form of medium-term floating rate loans (of 5-8 years duration) extended directly to businesses by asset management companies that are not subject to the strict capital and regulatory requirements facing commercial banks. The loans are extended at a relatively high interest rate to compensate for the greater risks involved, while also including covenants (e.g. restrictions on borrower leverage and dividend payments to other investors) to protect the lender against downside risk. For firms, private credit can provide access to debt financing that they would otherwise have difficulty obtaining, as well as a more tailored approach, including funding flexibility in times of stress to mitigate bankruptcy risk. Private credit may be particularly useful to meet borrowing needs of firms with limited physical infrastructure, heavy reliance on new but unproven ideas, and human capital that can walk out the door. In this way, such credit can support economic activity by bridging a financing gap for smaller, more innovative but riskier firms, especially since tightening regulations since the 2008 crisis has raised banks’ cost of capital and reduced their willingness to take risk onto their balance sheet.

- Private credit is typically funded by investors willing to lock up a portion of their resources for a number of years, to take advantage of higher expected returns and portfolio diversification benefits. Typically, the asset management company bundles together a package of such loans into a private-credit fund that can be sold onto investors. Most funding is obtained from institutional investors such as insurance companies and pension funds, which tend to have long-term investing horizons and the capacity to exercise due diligence on the quality of the private credit fund’s management and portfolio. Many funds also borrow from commercial banks through revolving lines of credit to enhance total fund returns through leverage and protect fund liquidity in case of a surge in withdrawals.

- Private credit increased dramatically in recent years driven by high and quite stable returns. Analyst estimates suggest that total private credit rose from around $0.2 billion in 2000 to around $1 trillion in 2019 to reach $1.5-2.0 trillion by the end of 2024. The largest share of this lending — around $1 trillion — is in the United States (see chart), where it is now approaching the scale of commercial and industrial loans from banks. Indeed, as the market segment began to access greater pools of capital, larger firms that had previously funded themselves through syndicated loans or corporate bonds also began to borrow in private credit markets to take advantage of the customized arrangements they can provide and to avoid the costs and disclosure requirements associated with public markets. The expanding market share of private credit has been supported by returns on private credit funds that have historically been high and quite stable compared to other forms of fixed-income investments. Measured using the Cliffwater Direct Credit Index, annualized returns from 2015 to 2025 averaged 9.4 percent per year, compared to 6.5 percent for high yield bonds and 2 percent for the US aggregate bond index. Moreover, losses reported at times of stress have generally been lower than on other forms of investment. The largest peak-to-trough decline since 2015 was during the COVID pandemic in 2020, when the CDLI declined almost 5 percent but much less than other bond indexes.

- Building on this performance, private credit funds have sought in recent years to attract a greater number of individual investors, including by offering greater liquidity during the lifetime of the fund. A significant share of funding for private credit in the U.S. has been channeled through business development companies (BDCs) which were authorized by Congress in the 1980s to support financing for small to mid-sized companies, including by individual investors. Before 2020, most BDCs were closed-end funds, which allowed for redemptions only at the fund’s fixed end date. Individual investors can buy and sell such funds on the market but prices are typically volatile. By contrast, much of the recent expansion of BDCs has used a non-traded, perpetual structure with “gates”, which is designed to offer liquidity to investors at a more stable valuation while protecting the fund from excessive withdrawals. Specifically, such funds provide a quarterly window for investors to request a share redemption at net asset value subject to an overall cap applied at the discretion of the fund manager to limit withdrawals to protect the fund since most of its assets are tied up in longer-term, non-liquid lending. Back-up bank lines of credit also offer the fund some protection from heavy investor withdrawals, but unlike commercial banks, investors in private credit funds are not protected by deposit insurance or a lender-of-last-resort facility from a central bank.

- Growth of private credit funds in the U.S. has been facilitated by the easing of regulatory limits on individual investor access in recent years. Individual participation in less regulated and less transparent private markets is generally limited to “accredited investors” that meet minimum net-worth and income limits, given the greater liquidity and valuation risks involved. However, these limits have not kept pace with rising asset valuations and inflation and recent SEC estimates suggest that 12.6 percent of the U.S. population now qualify under this standard. Retail investor access is being further opened up by regulatory actions. Since March 2025, the SEC has eased multiple constraints on BDCs offering non-traded funds, which has allowed them to broaden their retail base to a wider range of investors. Moreover, in March 2026, the US Labor Department circulated for comment a proposed rule to make it easier for individual investors to hold alternative assets — including private credit — in their 401(k) retirement accounts.

- Private credit has undergone significant stress in recent months. The soundness of some private credit loans began to be questioned after a couple of high-profile bankruptcies by borrowers in the fall of 2025, while overall returns in the sector began to seem less attractive as market interest rates came down. Concerns increased in early 2026 as investors worried that software companies, which borrowed heavily in the private credit market, were vulnerable to being eclipsed by rapid advances in artificial intelligence technology. J.P. Morgan analysts estimate that aggregate loans to software companies account for 21 percent of BDC investments and exposure rises to 40 percent including other tech and business services sectors. Total returns on the CDLI dipped to 1.1 percent in the first quarter of 2026 as many funds reported higher defaults, unrealized losses, and shifts to non-accrual status in their lending portfolios. In a market environment of increased uncertainty and greater press attention to the risks of private credit investments, new inflows into private credit funds dwindled and a rising share of investors sought to withdraw their funds. In the event, a number of funds applied gates to limit such withdrawals to at most 5 percent. Funds that are particularly exposed to the software sector like Blue Owl experienced the heaviest markdowns and withdrawals.

- Recent market stress has underlined concerns about the possibility that private credit involves risks that have not been fully tested and that a disruption in the market for private credit could pose significant risks to the broader financial system. The IMF, the FSB and the Group of 30 have recently issued reports highlighting vulnerabilities from the private credit sector. A common concern is that the opaqueness of the information on the sector makes it difficult to gauge the extent of leverage involved and to assess the interconnections with other parts of the financial system that could propagate local problems more widely. Nevertheless, the overall risks to the financial system seem broadly contained since private credit is still largely funded by long-term institutional investors rather than retail investors, use of leverage (especially in the form of short-term borrowing) is limited for most funds, and bank exposure is still assessed to be small relative to bank capital and limited to the fund’s most senior liabilities. Consequently, the risks thus far do not seem commensurate with those from the heavily leveraged mortgage-backed securities market that triggered the 2008 global financial crisis, when U.S. and European banks had to write down more than $1 trillion in toxic assets and bad loans, and several major banks failed or needed to be restructured. Nevertheless, the financial experts cautioned that the risks related to private credit are growing and need to be carefully priced and monitored to avoid further amplification of risk exposure of the financial system.

What this Means:

Private credit does not seem to be a systemic threat at this point, but individual investors do need to be cautious in investing in this market. Private credit funds are still facing stress as redemption requests have continued in the second quarter. So far, the episode seems relatively contained in terms of the scale of mark downs and withdrawals, and senior officials and market leaders (including Treasury Secretary Scott Bessent and J.P. Morgan chief Jamie Dimon) have offered reassurance that they do not anticipate systemic problems. Still, it is hard to assess whether this episode marks a temporary dip that prompts a useful correction of lending standards and heightening of investor scrutiny of assets within this class or a more permanent inflection point in the market pointing to lower future growth and returns. One particular concern is that the semiliquid gated structure has not been fully tested under stress, and that a continuing slow-motion run on private credit funds could exhaust liquidity buffers and expose investors to greater losses. Given the question marks still hovering over this sector, it will be important to consider carefully how far to open small retail investors’ access to private credit investments, balancing the potentially advantageous returns from such investments against the increased risks of loss involved for less sophisticated investors with lower wealth buffers and greater need to retain liquid access to their savings to deal with adverse shocks.

Topics:

Financial MarketsLike what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.