Federal Debt and the Risk of a Fiscal Crisis

Harvard University

Executive Summary

High and rising federal debt, combined with concerns about policymakers’ willingness and ability to manage the government’s finances, increase the risk of a fiscal crisis in which investors demand sharply higher interest rates to hold US Treasury securities. A fiscal crisis would disrupt financial markets, raise borrowing costs and reduce credit access across the economy, and weaken output and employment — which would generate further financial distress. Fiscal crises are extremely difficult to predict, and shifts in investor sentiment can occur very quickly, which increases the value of changing federal tax and spending policies sooner rather than later.

I. The Evolution of Federal Debt

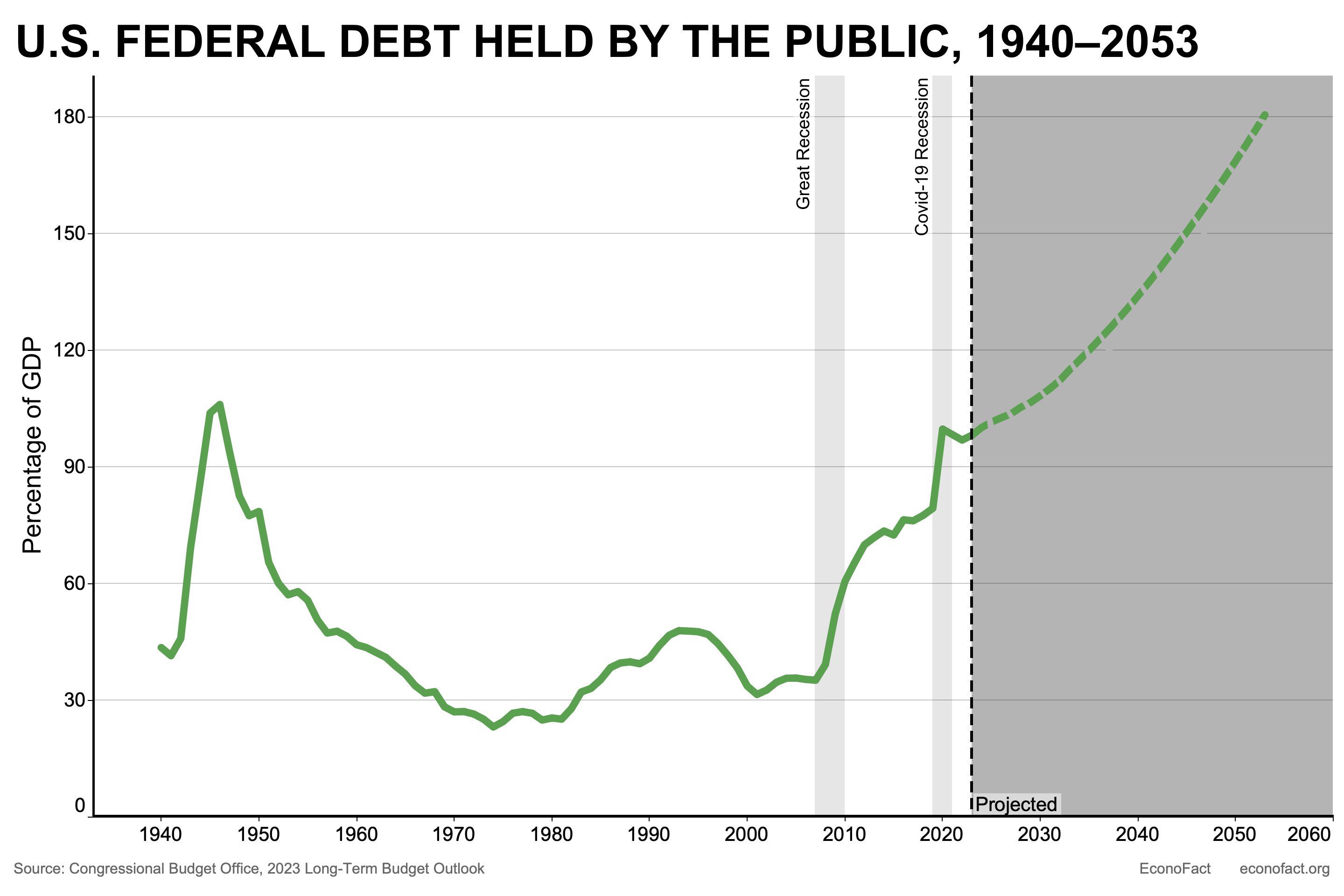

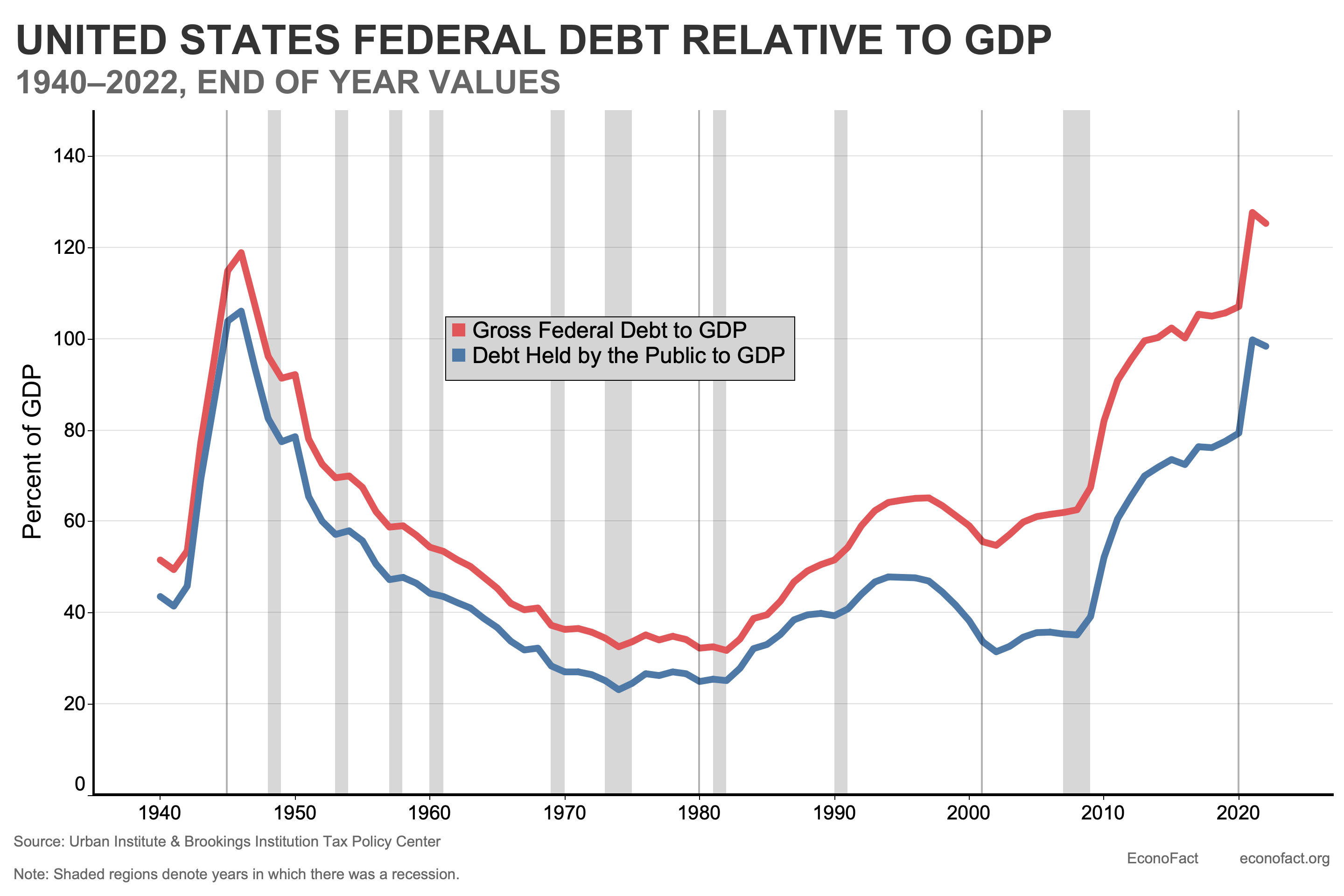

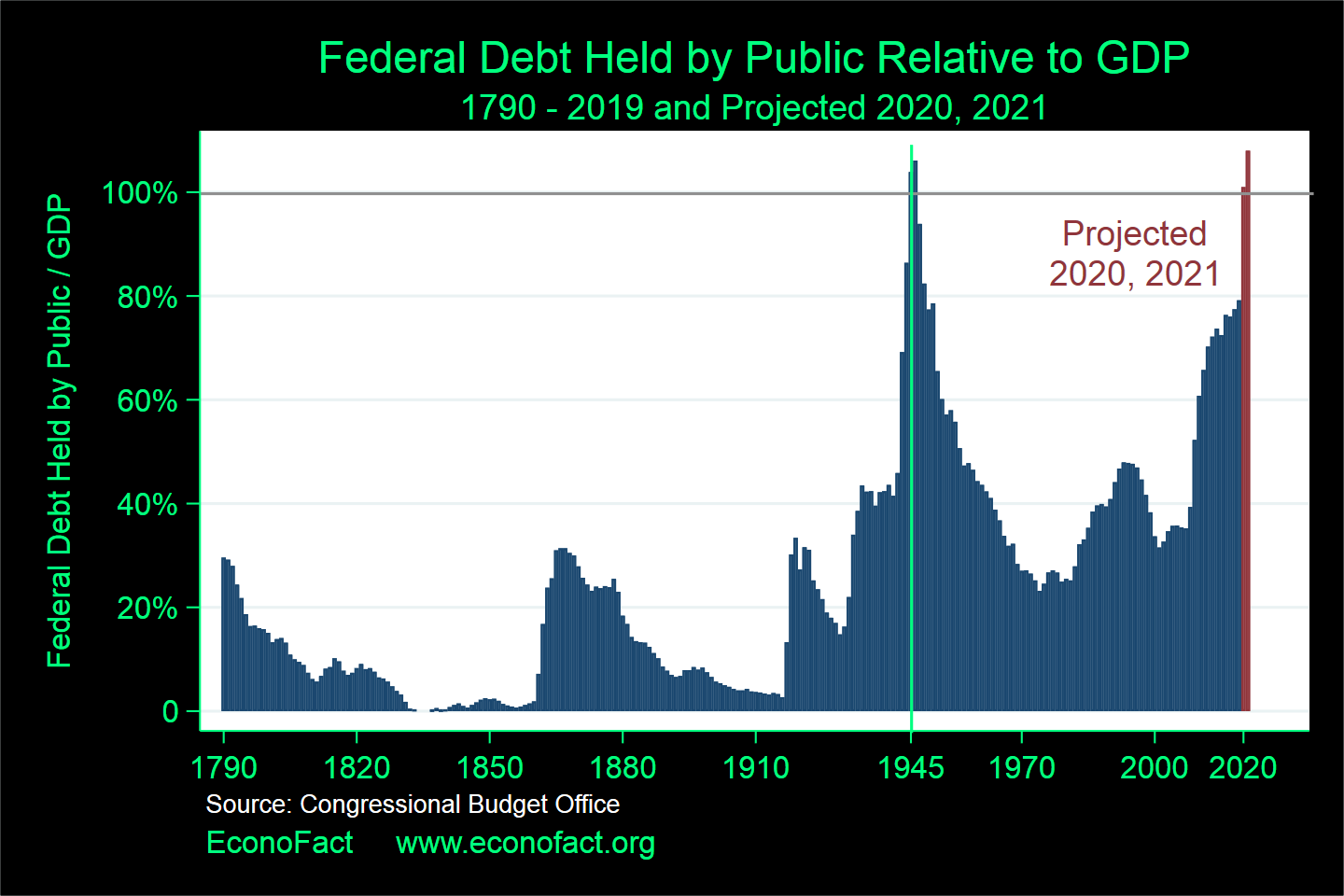

Federal debt in the United States is historically high relative to national income. The most useful measure of federal debt is debt held by the public — that is, debt not owed by one part of the government to another part of the government. National income represents the potential tax base for supporting debt and is often proxied by gross domestic product (GDP). Federal debt held by the public, which equals the accumulation of past federal budget deficits, is now close to its highest level relative to GDP in the country’s history.

The Congressional Budget Office (CBO) projects that, under current law, federal debt will rise much further relative to GDP in coming years.1 That projection is based on the presumption that policies scheduled to expire under current law (such as certain tax provisions) expire as scheduled. Debt is expected to keep climbing relative to GDP because annual deficits are expected to be about 6 percent of GDP — large enough for debt to grow faster than the economy. The country has not previously experienced deficits this high apart from wars and economic downturns. Deficits will be large both because the gap between noninterest spending and revenue is expected to remain sizable and because interest payments will be pushed up by increasing debt.

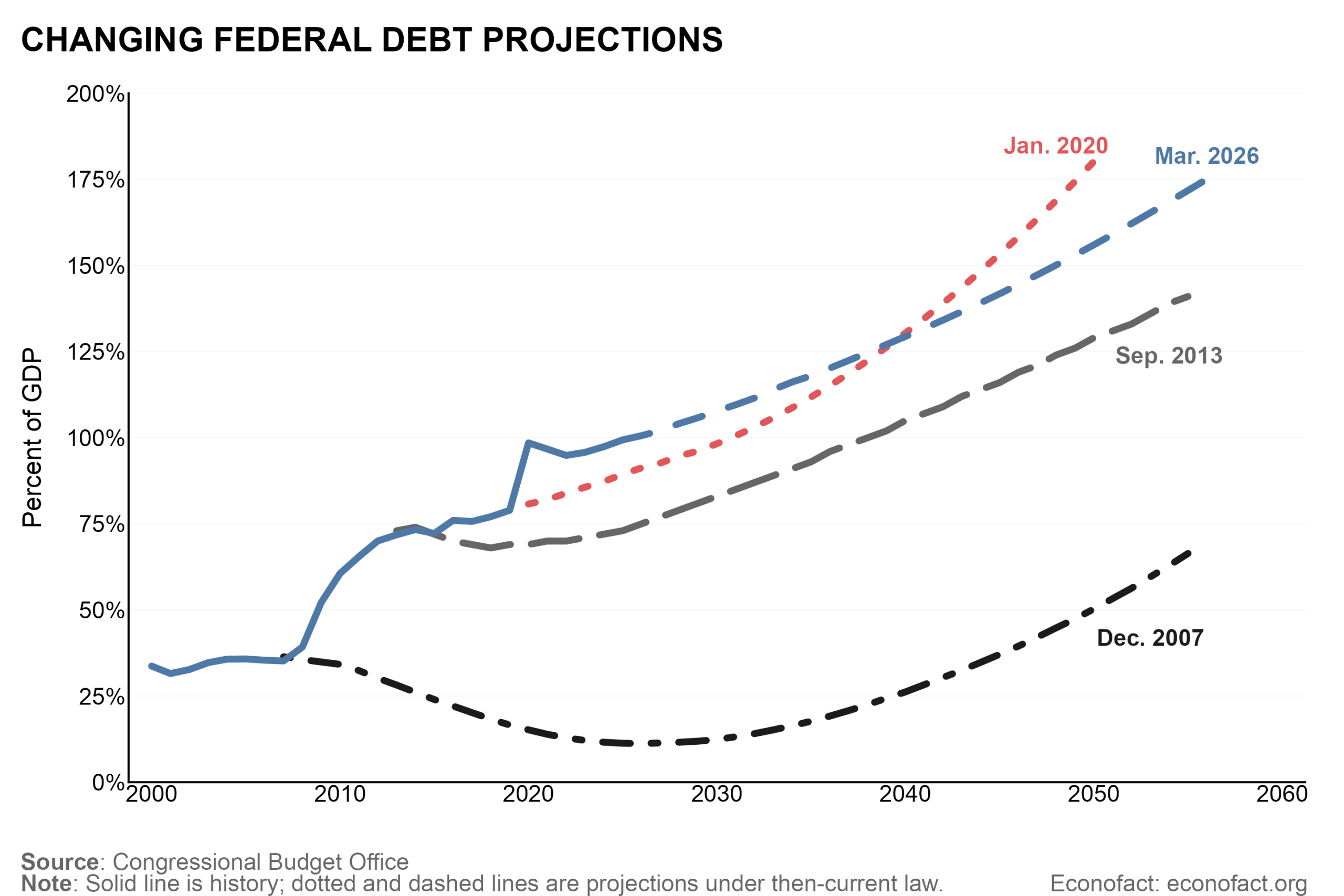

Source: Congressional Budget Office “The Long-Term Budget Outlook Data: 2026 to 2056” Feb. 2026.

Projections of budget outcomes are highly uncertain. Economic shocks and policy changes have shifted federal revenue and spending significantly in the past and will undoubtedly continue to do so. The actual and projected path of debt is much higher today than it was in 2007 — as shown in the chart below. The figure presents CBO’s projections of debt in 2007 (before the global financial crisis), in 2013 (after that crisis and the Great Recession), in 2020 (before the COVID recession), and in 2026. The differences between the projections primarily reflect substantial cuts in taxes as well as the two severe recessions and policy responses to them. Federal budget deficits increase automatically in recessions as income and therefore tax revenue decline and as spending for safety-net programs increases; in addition, policymakers enacted further reductions in taxes and increases in spending to spur economic growth and protect households from the economic downturns. Population aging and rising health care costs continue to be key drivers of the fiscal outlook but do not have larger effects than what was projected in 2007.

Notwithstanding the uncertainty of budget projections, federal debt will almost surely continue rising relative to GDP unless tax and spending laws are changed. Stabilizing the debt-GDP ratio under current policies would require large and favorable shifts in a combination of productivity, interest rates, and gaps between noninterest spending and revenue given existing laws. Such auspicious changes are conceivable but very unlikely. Therefore, preventing continual increases in federal debt relative to GDP will require actions by policymakers.

Continual increases in federal debt relative to GDP are not sustainable. As debt keeps rising relative to GDP, interest payments on the debt will rise relative to GDP as well, holding all else equal. That growing burden compared with the potential tax base for supporting debt cannot continue indefinitely.

II. The Risk of a Federal Fiscal Crisis

High and rising federal debt, combined with concerns about policymakers’ willingness and ability to manage the government’s finances, increase the risk of a fiscal crisis. Such a crisis would occur if investors demanded sharply higher interest rates to hold US Treasury securities.

Higher federal debt increases the risk of a fiscal crisis through several channels. Higher debt means a larger supply of outstanding Treasury securities. All else equal, that larger supply will be willingly held by investors only if they are rewarded with higher interest rates. In addition, anticipation of continued debt accumulation can heighten investors’ concerns that policymakers may attempt to default on the debt or reduce the value of the debt through inflation or other means. That anticipation would cause investors to demand higher interest rates to compensate them for the greater risk. Moreover, when debt is higher, any given increase in interest rates boosts interest payments by more, which pushes debt still higher relative to the potential tax base for supporting debt — and expectations of that dynamic can trigger a crisis.

The risk of a federal fiscal crisis is compounded by policymakers’ abandonment of efforts to stabilize the debt. Policymakers enacted significant deficit-reducing measures in the 1980s and 1990s but have not done so during the past quarter-century. Moreover, political polarization makes fiscal adjustment even more challenging now: Bipartisan agreements on policy changes are harder to reach, and partisan policy changes to reduce debt would have the immediate disadvantage of being politically unpopular and the long-term disadvantage of giving the other party budgetary space for advancing its own priorities when political control shifts. In addition, some policymakers and observers have offered ideas for reducing the budgetary burden of outstanding debt at the expense of debt holders, albeit not generally framed in those terms. One example is calls for the Federal Reserve to lower interest rates in order to reduce the government’s borrowing costs rather than to fulfill the Fed’s mandates regarding the economy. Another example is the suggestion that some foreign holders of Treasury securities could be pressured to purchase certain securities as a condition of maintaining US security guarantees for their countries.

The risk is further increased by policymakers’ increasing difficulty in recent years executing the basics of fiscal management. Increases in the debt ceiling often have involved brinkmanship that has raised the chance of payment disruptions. Appropriations legislation has often not been enacted before previous appropriations have lapsed, leading to stopgap funding in some instances and causing extended government shutdowns in others. Such messy execution of day-to-day financial activities combined with inaction on debt-reducing policy changes and discussions of potential actions hurting debt holders can reduce investor confidence in the future return on Treasury securities. The result, all else equal, is higher interest rates on those securities and a greater chance of a sharp runup in rates if worries about fiscal policy mount.

Unfortunately, fiscal crises are extremely difficult to predict. Investor sentiment toward government debt can depend not only on the level and growth of debt but also on political dynamics, economic conditions, and financial markets and institutions. Countries differ widely in these characteristics, and fiscal crises are rare, so historical experience offers little basis for strong inferences.

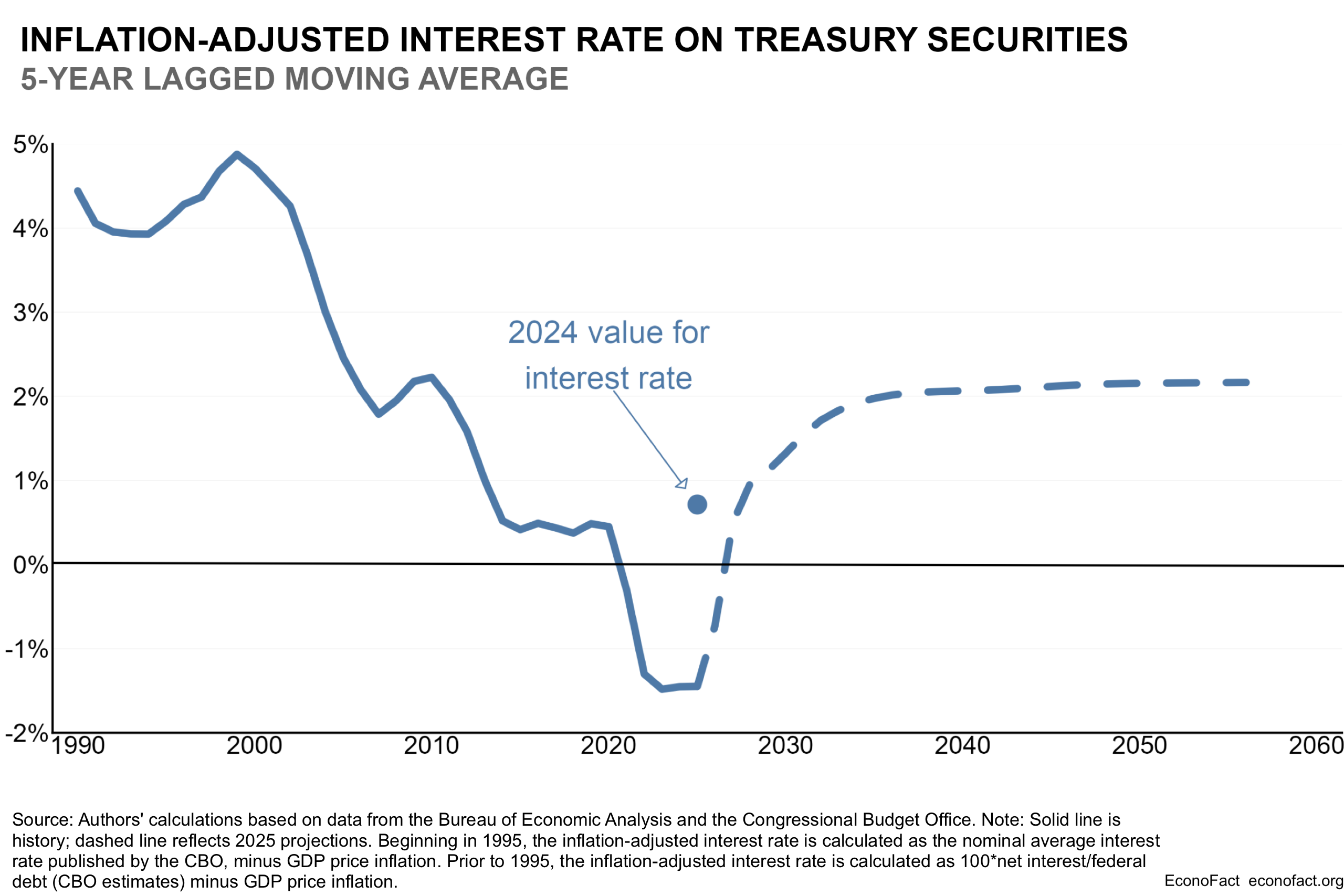

Despite the rising risk of a federal fiscal crisis, interest rates on Treasury securities are roughly the same today as they were two decades ago when debt was only one-third as large relative to output. Federal debt equaled 35 percent of GDP in 2007 and is about 100 percent of GDP today. Despite that tripling in the amount of debt relative to output, interest rates on Treasury securities are about the same today as in 2007 — as shown in the chart below, which presents a five-year moving average of Treasury rates adjusted for inflation in GDP prices.2

Click here for a larger version of the graph.

The fact that Treasury interest rates have changed little on balance over the past two decades shows that investors’ demand for Treasury securities has kept pace with growing supply. Domestic demand for Treasury securities has been boosted by demographic and economic forces. Population aging has increased demand, because older people tend to hold more wealth relative to income and to prefer safer assets. In addition, slower growth of productivity and the labor force has moderated private demand for investment funds, leaving more saving available to support demand for Treasury debt. Foreign demand for Treasury securities has also been strong. The market for Treasuries remains the deepest and most liquid financial market in the world, and no asset comparable to Treasuries is offered in Europe, China, or elsewhere. Demand for Treasuries is bolstered further by the dollar’s serving as the world’s primary reserve currency and underpinning a large share of global trade in goods and services and an even larger share of global financial transactions.

Yet, the factors that have boosted demand for Treasury securities are not immutable, and economic shifts and political developments could weaken confidence in Treasury securities. Interest rates continue to be held down by factors such as population aging. However, the surge in investment in computing power is bolstering private demand for loanable funds, and the runup in US inflation in 2021 and 2022 increased the risk premium on long-term debt. Moreover, the stark shifts in international relations in 2025 and 2026 may weaken the dollar’s global position and undermine the role of Treasuries as a safe haven. However, the evidence on the latter point is unclear: The dollar dropped sharply in April 2025 when the United States levied tariffs on imports from around the world, but the dollar’s value today is still about the same as its value two years ago and above its value earlier in the decade.

Shifts in investor sentiment can occur very quickly. The late economist Rudi Dornbusch once said regarding overvaluations of currencies that a “crisis takes a much longer time coming than you think, and then it happens much faster than you would have thought.” Indeed, some countries have sustained high government debt for a while without evident trouble and then endured sudden and severe fiscal crises. Therefore, even though investors do not seem especially concerned about the US fiscal situation now, that situation could change abruptly — and the risk of such a change is increasing because of high and rising debt and political dysfunction.

III. How a Federal Fiscal Crisis Might Unfold

Fiscal crises are not events that economists can predict with any precision. Crises do not occur when a single indicator crosses a particular threshold, nor are they typically caused by individual policy errors. Instead, crises tend to emerge from interactions among high debt, political worries, and stresses in financial markets and institutions, with expectations playing a central role. To understand how these vulnerabilities could interact — and what is at stake when investor confidence falls — it is useful to examine how a US fiscal crisis might unfold.

A fiscal crisis unfolds first in financial markets. Decisions in financial markets are inherently forward-looking, so market prices and yields reflect expectations of future events and not necessarily current conditions. A fiscal crisis could begin because investors become unwilling to hold US Treasury securities at typical interest rates for a number of different reasons. For example, investors might demand higher rates in response to information implying that budget deficits would be markedly larger over time, such as a political shift or an increase in international tensions. Alternatively, they might demand higher rates because of a pronounced deterioration in the country’s economic outlook that raised doubts about the government’s ability to fully honor its outstanding obligations. Or, investors might demand higher rates not because of a change in fundamental budget or economic factors but because of a problem in the “plumbing” of the financial system that led to a poorly received auction of Treasury securities.

Interest rates could rise further through self-reinforcing dynamics as that initial “spark” of higher rates falls on the “dry tinder” of the risks described earlier. Higher rates increase government interest payments — and more quickly than observers may realize, because a large share of Treasury debt matures and must be refinanced each year. Higher interest payments worsen the fiscal balance and reinforce concerns about the trajectory of debt, pushing interest rates up more.

Stresses in the market for government debt can propagate through the financial system via multiple channels. Losses or margin pressures at leveraged institutions may force sales of Treasury securities, driving down their prices and directly amplifying increases in Treasury yields. Such losses or pressures can also lead to sales of other types of securities, spreading stresses across financial markets. Uncertainty about which markets might be affected next undermines confidence broadly. Because many financial markets and institutions are essentially global, the propagation of stresses and uncertainty does not stop at national borders. Leveraged institutions may need to sell assets in foreign countries, raising interest rates and creating pressures on financial institutions in those countries.

The “Truss moment” in Britain in 2022 illustrates how some of these dynamics can play out. Prime Minister Truss announced tax and spending policies that investors worried would substantially increase British government debt, and she had omitted the typical review of new policies by the independent UK Office for Budget Responsibility. Investors dumped long-term British bonds (called “gilts”), which led to additional bond sales by leveraged financial intermediaries. Yields on gilts jumped up, and the value of the British pound dropped sharply. That turmoil ended fairly quickly when Prime Minister Liz Truss changed fiscal policies and then resigned from office. But a key lesson from this episode is that feedback in financial markets can generate a large rise in interest rates even when an initial shock appears modest.

Central banks can sometimes interrupt damaging financial dynamics by purchasing securities or making funds available to financial intermediaries in other ways. During the Truss moment, the Bank of England purchased gilts briefly to restore market functioning. Similarly, at the onset of the COVID-19 pandemic in March 2020, the Federal Reserve conducted large-scale purchases of Treasury securities to stem the “dash for cash.” However, central bank interventions can at best provide temporary relief from financial turmoil and cannot fully substitute for fiscal policy actions to restore investor confidence in government debt.

Financial stresses have damaging economic effects, which in turn can exacerbate the financial stresses. Turmoil in the financial system tightens financial conditions faced by households and firms. A runup in Treasury interest rates raises the rates charged to households and firms. In addition, losses at financial institutions and heightened uncertainty cause lenders to pull back on credit supply, further restraining borrowing even by households and firms willing to pay higher rates. Higher interest rates and weaker economic prospects lower asset values, including equity prices and real estate prices, which weighs on household wealth and firms’ assessments of the value of their activities. Higher interest rates, diminished access to credit, and lower asset values reduce consumption and investment. As output and employment weaken, the losses of income and revenue lead to further cuts in consumption and investment, and the economy can easily fall into recession. Investors respond to the financial stresses and economic slowdown by pulling capital out of the country or reducing the inflow of capital that might otherwise occur.

A quick and constructive response to a fiscal crisis is vital. The reactions by fiscal policymakers to an unfolding crisis can make a crucial difference in shaping the financial and economic dynamics. If public leaders respond constructively, by clarifying policy intentions or adjusting policies, they may reassure financial-market participants, and the recovery in investors’ confidence may ease borrowing costs. For example, the swift response to the “Truss moment” in the United Kingdom kept that event to a moment rather than letting it fester into a prolonged crisis. But if leaders instead cast blame and defer action, worries about future policy can deepen, further reducing investors’ willingness to hold federal debt at typical interest rates.

If interest rates on government debt continue to rise, and financial turmoil spreads, policymakers eventually need to restore confidence by making policy changes that put debt on a more sustainable path. For the United States, the needed changes probably would be large: Suppose that restoring confidence required changes in policies that would cause CBO to project that debt, rather than rising further, would equal its current value of roughly 100 percent of GDP in 30 years’ time. Then, policymakers would need to enact some combination of spending cuts and tax increases that totaled more than 1½ percent of GDP over those years, which would be roughly $500 billion per year now.3

Such policy changes may not mark the end of a fiscal crisis, but rather the beginning of a prolonged period of economic and political strain. The abrupt fiscal tightening weighs further on consumption and investment and generates more weakness in output and employment. Even if confidence is partially restored, the combination of weaker growth, tighter fiscal policy, and damaged institutions can leave lasting scars. In some cases, governments have defaulted on their debt or sought external assistance from institutions such as the International Monetary Fund.

The Greek experience of the past decade and a half illustrates how severe and persistent the consequences of a fiscal crisis can be. In 2009, Greece had a large amount of public debt, a very large budget deficit, a large current account deficit, public debt denominated in a currency (Euros) that Greece did not control, extensive tax evasion, and revisions to budget statistics that reinforced concerns about the quality of data. A fiscal crisis arose, and the government was forced to adopt sudden fiscal austerity. Greek GDP fell sharply and recovered only gradually, so Greek debt actually rose relative to GDP over the following decade despite the austerity measures. Economic and financial conditions in the United States differ in many crucial ways from conditions in Greece, so the Greek experience does not foretell what would happen in the United States if a fiscal crisis occurred here. But a useful lesson from that experience is that once a fiscal crisis takes hold, reversing its economic damage can be difficult and slow.

IV. Recognizing the Unpredictability of a Federal Fiscal Crisis, What Can Policymakers Do?

The inability to predict the timing of a federal fiscal crisis should not be mistaken for evidence that the risk of a crisis is low or that inaction by policymakers is costless. Even though current US fiscal policies are almost certainly unsustainable, the most likely outcome in any given year is that investors absorb the available federal debt without causing a spike in Treasury interest rates. Yet, if policies are not changed, the risk of a fiscal crisis will continue to increase over time as federal debt increases, so a crisis will probably occur at some point.

Putting federal debt on a more sustainable path is crucial. Cutting spending and raising taxes to lower the trajectory of debt would reduce the likelihood of a crisis and, if a crisis occurred, mitigate its consequences. With less debt, interest payments would be smaller, and those payments would be less sensitive to changes in interest rates. In addition, the act of changing policy to put debt on a more sustainable path would demonstrate the political willingness and ability to adjust fiscal policy when necessary. All of those differences would strengthen investor confidence and make a fiscal crisis less likely. If a fiscal crisis occurred nonetheless, less debt would mean that the initial increase in interest rates would raise the government’s borrowing costs by less, leading to less deterioration in the fiscal outlook and less reinforcement of concerns about the debt path. Moreover, with less debt, the policy changes needed to restore investors’ confidence by keeping debt to any given size relative to GDP would be smaller. Smaller cuts in spending and increases in taxes would reduce the severity of the economic downturn resulting from a crisis, which would in turn diminish the ensuing political and social turbulence.

Institutional reforms that increased the likelihood of future federal debt restraint could help as well. For example, the Senate and House of Representatives could adopt rules that require supermajority approval for any legislation that would increase long-term deficits, or they could establish a bipartisan fiscal commission whose recommendations would receive expedited Congressional consideration and up-or-down votes. More fundamentally, the country could adopt a Constitutional amendment that limited deficits or debt. Such mechanisms would be intended to hinder policy changes that enlarge deficits and facilitate changes that shrink deficits.

However, institutional constraints on federal budget deficits and debt may have limited impact. For example, the so-called “One Big Beautiful Bill” Act extended tax cuts that had been scheduled to expire under previous law and thereby increased long-run deficits. Senate rules for reconciliation bills prohibit legislation with that effect, but the Senate Budget Committee chairman circumvented the prohibition by declaring that the appropriate benchmark for assessing the bill’s deficit effect included an extension of the expiring tax cuts. As another example, some bipartisan efforts to agree on deficit-reducing policy changes — the 2010 Bowles-Simpson commission and the so-called Supercommittee that followed it — did not receive sufficient political support to generate policy changes. A Constitutional amendment might be written strictly enough that deficits would be reduced significantly, but such strictness would create an opposing danger of paralyzing fiscal policy when domestic or international crises emerge; that concern leads many analysts to oppose a strict fiscal amendment. One set of institutional reforms that restrained debt growth was the Budget Enforcement Act of 1990, which established caps on annual appropriations and a pay-as-you-go constraint on taxes and entitlement programs. But those constraints were intended not so much to compel new deficit-reducing policy changes as to preserve the deficit reduction achieved by policy changes enacted in 1990, and when fiscal conditions improved dramatically in the late 1990s, policymakers largely abandoned the constraints.

Planning for a federal fiscal crisis could be valuable also. President Eisenhower once observed that “plans are worthless, but planning is everything” — presumably because specific plans never correspond exactly to the circumstances that arise, but the process of planning prepares one to respond to a wide array of circumstances. In preparing for a potential fiscal crisis, valuable planning could include creating different scenarios for the evolution of a crisis and building frameworks for responding to those scenarios — for example, by decision-making authorities, developing coordination mechanisms, and assessing policy tradeoffs. Such planning could reduce confusion and delays if investors’ confidence deteriorated rapidly, making a crisis substantially less damaging.

V. Conclusion

Without significant changes to tax and spending policies, the United States faces a growing risk of a fiscal crisis, although the timing of such a crisis is inherently uncertain and could be far in the future. Strong demand for Treasury securities and the dollar’s central role in global finance have so far allowed the federal government to sustain high and rising debt without a sharp increase in borrowing costs. But those conditions are not guaranteed to persist, and history suggests that shifts in investor confidence can occur abruptly.

Against that backdrop, the absence of an immediate crisis should not be a reason for complacency. Putting federal debt on a more sustainable path, strengthening fiscal governance, and improving preparedness for a potential crisis would reduce vulnerability and limit the economic and social damage if confidence were to falter. Acting before financial markets force changes in policies would give policymakers more flexibility and help avoid the most disruptive outcomes — benefits that become increasingly important as debt continues to rise.

Footnotes

- This projection comes from CBO’s The Long-Term Budget Outlook Data: 2026 to 2056, which was published in February 2026. ↩︎

- The same point holds for the nominal yield on 10-year Treasury securities, which is a key benchmark in financial markets. ↩︎

- This calculation is based on CBO’s The Long-Term Budget Outlook under Alternative Scenarios for the Economy and the Budget, which in turn draws on CBO’s The Long-Term Budget Outlook: 2025 to 2055. CBO has not released alternative scenarios based on this year’s updated budget outlook. ↩︎