The 10-Year Treasury Rate: Why Is It Important and What Can Policy Do About It?

Williams College

The Issue:

Few financial indicators are as closely watched as the interest rate on 10-year Treasury securities. So much so, in fact, that Treasury Secretary Bessent stated in a February 2025 interview that “The president wants lower rates. He and I are focused on the 10-year Treasury and what is the yield of that.” What is the 10-year Treasury yield? What role does it play in the economy? What determines it? And what (if anything) can the Treasury do to affect it?

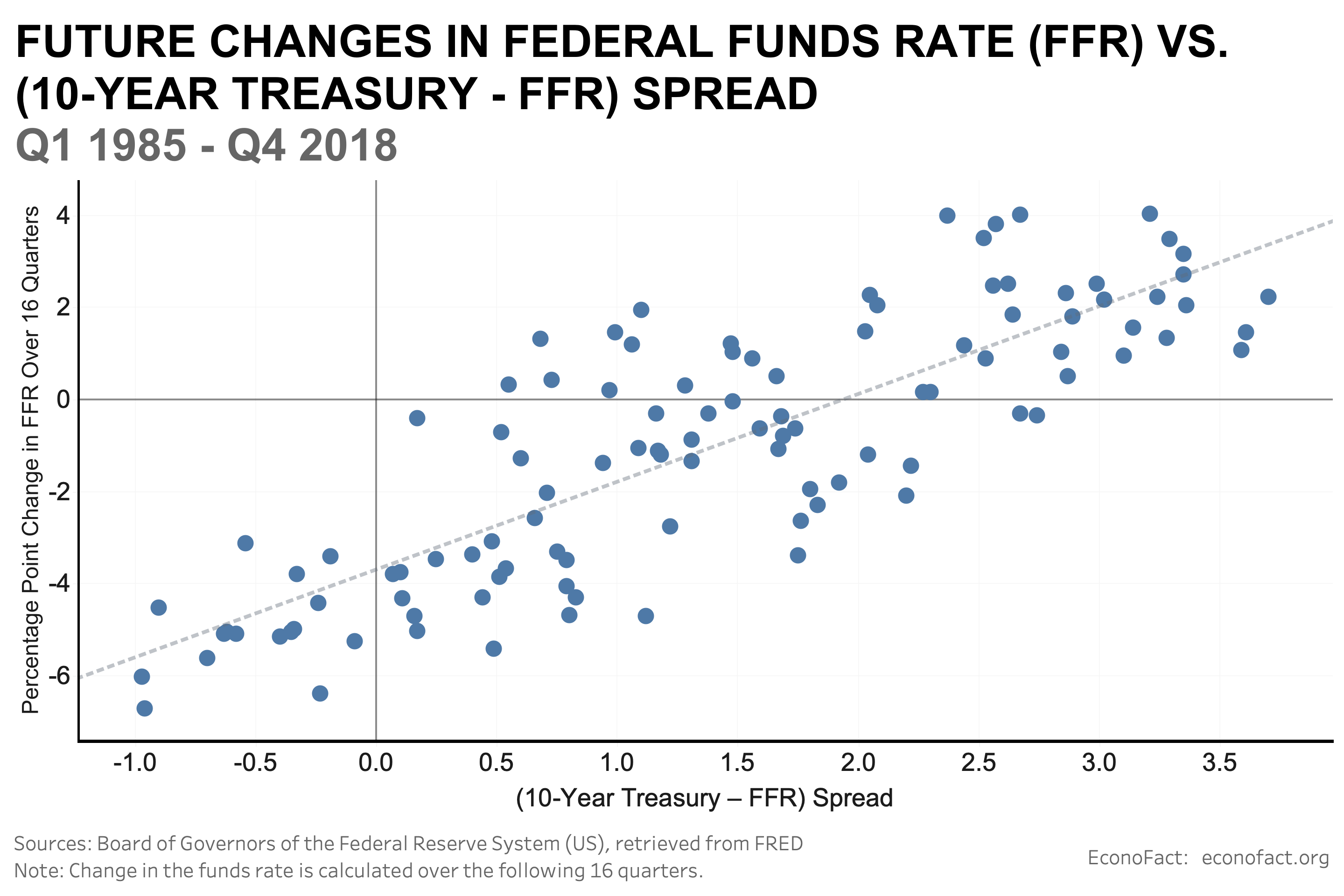

Expectations of future short-term rates are the single biggest factor affecting long-term rates, including the 10-year Treasury yield.

The Facts:

- Treasury securities are debt instruments issued by the U.S. government to finance its budget deficit. Treasury securities come in a range of maturities (the time until the principal is repaid) from four weeks to 30 years. The 10-year Treasury yield (the “yield to maturity”) is what an investor would earn if they purchased a 10-year bond and held it to maturity. But treasuries are tradeable, and this allows investors to sell them in a secondary market before the maturity date. The prices of bonds, both at the time of their initial issuance and in the secondary market, vary inversely with yields since a bond represents a promise to pay a fixed amount in the future and the lower the price paid for that bond the higher the yield. If prevailing interest rates rise unexpectedly, for instance, an existing bond with interest rate below the current market rates will sell for a lower price and the investor who sells the bond before its maturity, will earn a lower-than-expected return.

- The market for Treasury debt is vast and active. As of the end of 2024, there were $28 trillion in Treasury securities outstanding, dwarfing the $9 trillion in bonds issued by corporations and banks. Ownership of Treasuries is widespread: mutual funds own $3 trillion; households, $2.8; banks, $1.5; state and local governments, $1.7. Private investors, central banks and governments outside the U.S. own $8.7 trillion in Treasuries. The Fed holds $4 trillion. Every day, over a trillion dollars’ worth or Treasury securities are traded, more than triple the daily trading volume of equities in the U.S.

- The 10-year Treasury rate affects the cost of financing the government’s debt. The high level of accumulated government debt, together with increases in interest rates, meant that interest payments on the debt made up about 13 percent of federal spending in 2024 which was more than spending on defense. Although the government deficit – the extent to which government expenditures surpass government revenues — has come down from its pandemic high, it remains high relative to the historical average and it is projected to keep increasing under current policy over the next three decades as an aging population will require significant federal support for both income and healthcare. This will increase the outstanding government debt held by the public both in absolute terms and in proportion to national income (GDP).

- The 10-year Treasury rate also affects the private sector’s borrowing costs. The 10-year Treasury yield serves as a benchmark for a wide range of interest rates that have a direct effect on household spending as well as business investment. When the yield on the 10-year Treasury rises, borrowing costs across the economy tend to increase as well. The opposite happens when the 10-year Treasury yield drops. The interest rates with the most direct effects on expenditures are those on home mortgages and corporate bonds, both of which closely track the 10-year Treasury yield. The first graph shows that there is a close correlation between the yield on the 10-year Treasury bill and both the average 30-year fixed mortgage rate and the Aaa corporate bond yield.

- Expectations of future short-term rates are the single biggest factor affecting long-term rates, including the 10-year Treasury yield. The Fed sets the federal funds rate, the interest rate banks lend reserves to each other overnight, and through this it indirectly controls, for all intents and purposes, other short-term interest rates. The Fed tightens monetary policy by raising the federal funds rate to slow the economy when it is overheating and cuts the rate to stimulate spending when the economy falters. The 10-year yield is in turn strongly influenced by expectations of the future path of short-term interest rates. Consequently, the 10-year rate tends to be high, relative to the funds rate, when investors expect tighter monetary policy in the future. Conversely, declines in the 10-year rate, relative to the federal funds rate, often foreshadow looser policy. This relationship is evident in the graph below, which plots the difference between 10-year Treasury yield and the federal funds rate on the horizontal axis and the change in the federal funds rate over the following four years on the vertical axis. (Periods in which the federal funds rate was zero are excluded.) The plot shows that bond traders are reasonably good at anticipating Fed policy: increases in the federal funds rate generally follow periods in which the 10-year Treasury yield is high relative to the funds rate, and cuts in the funds rate typically follow periods in which the difference between the 10-year and funds rates is close to zero or negative.

- Another important factor for the yield on a 10-year Treasury bond is the expected path of inflation until the bond reaches maturity. All else equal, yields will be higher when the expectations of future inflation are higher because the value of a fixed payment in the future will be eroded by higher prices – thus these higher yields do not result in higher real, inflation-adjusted returns if the expected inflation comes to pass. Inflation expectations depend, in part, on the public’s views of the Fed’s commitment to maintaining low inflation, what is often called its “credibility.” In the 1980s, occasional spikes in long-term bond yields have been attributed to “inflation scares,” episodes in which doubts arose about the Fed’s commitment to low inflation. Similarly, the Fed’s reluctance to commit to an inflation target may explain the excess sensitivity of long-term interest rates that had been observed before the adoption of an explicit inflation target of 2% in 2012.

- The real, inflation-adjusted return on 10-year Treasury bonds also depends on the amount of bonds the government sells to finance its budget deficit. Just as with anything sold in a market, an increase in the supply of something relative to its demand lowers its price. A growing gap between government spending and government revenues means that the government needs to continually increase the supply of Treasuries to cover the shortfall. Demand from investors for Treasuries might not rise as fast as the increase in the supply of Treasuries, causing the price of Treasuries to fall. Since bond yields are inversely related to their price, this in turn will lead to higher yields. For this reason, all else equal government budget deficits tend to increase the 10-year Treasury yield. Consequently, the Treasury’s role in reducing the 10-year yield would work through reducing the budget deficit – but, of course, this would require the President and the Congress to bring about changes in tax and spending policies.

- Increases in perceived default risk or political instability could also raise the Treasury yield. Brinksmanship surrounding increases in the debt ceiling prompted the Fitch rating agency to downgrade federal government debt from AAA (its highest rating) to AA+ (its second highest) in 2023, reflecting concerns of “expected fiscal deterioration” and “an erosion of governance.” (Standard and Poor’s had downgraded federal debt 12 years previously, for similar reasons.) The two agencies’ downgrades were largely symbolic, and did not materially affect perceived default risk or yields; but growing doubts about the government’s commitment to timely repayment could lead to further downgrades, higher interest rates, and disruptions to the many financial markets that rely on Treasury interest rates as risk-free benchmarks.

- Although the market for 10-year Treasuries serves as a key barometer of the economy’s health, it is not always easy to decipher. Because multiple factors influence bond yields on any given day, it can often be difficult to interpret changes in the bond yield in isolation. For example, the 10-year Treasury yield fell by 0.63 percentage points from mid-January to early March 2025. The decline could reflect an ebbing of inflationary concerns or more optimistic views about the new administration’s potential for reducing the government deficit. However, over the same period participants in the market for federal funds futures came to expect an additional quarter-point reduction in the target federal funds rate in the following months, so an anticipated economic slowdown is the more likely explanation.

What this Means:

The bond market provides a real-time referendum on macroeconomic policy. Bond yields, notably the 10-year Treasury rate, contain information on the credibility of the Fed’s inflation target, the demands placed on financial markets by government budget deficits, and the likelihood of an economic downturn. The ability of monetary and fiscal policy to keep Treasury yields low in the long term is limited. The Fed can keep the rate low by maintaining its commitment to price stability. And to push the rate down, or at least to prevent it from rising, the federal government needs to stabilize the budget deficit. Moreover, the government must eschew political gamesmanship in budget and debt ceiling negotiations, lest it precipitate a fiscal crisis. Were this to happen, bond yields could rise sharply—as they did in the U.K. in late September 2022, when the Conservative government’s unveiled its plan for dramatic tax cuts (the “Growth Plan”), which caused the bond yield to soar 0.65 percentage points within the span of just two days. Given the central role played by the 10-year Treasury rate in the financial system, an abrupt spike of this magnitude would seriously disrupt the entire economy.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.