The Child Tax Credit’s Potential to Reduce Child Poverty

Boston University, University of California, Davis, Sanford School of Public Policy, Duke University, Harris School of Public Policy, University of Chicago

The Issue:

The rate of child poverty in the United States precipitously dropped in 2021 only to rise in more recent years. The drop occurred during a period of large temporary expansions of social support policies implemented during the COVID19 pandemic. Federal tax credit policies — and especially the expansion of the federal Child Tax Credit — were thought to have played a role in the reduction of child poverty at the time. Congress tasked the National Academies of Sciences, Engineering and Medicine to study the role of federal tax credit policies on child poverty during this period. What lessons did we learn from the 2021 expansion of the Child Tax Credit? Which provisions were the most effective in reducing child poverty, how much do they cost, and what are the tradeoffs?

Federal tax credits were responsible for lifting more than 2 million children out of poverty in 2021

The Facts:

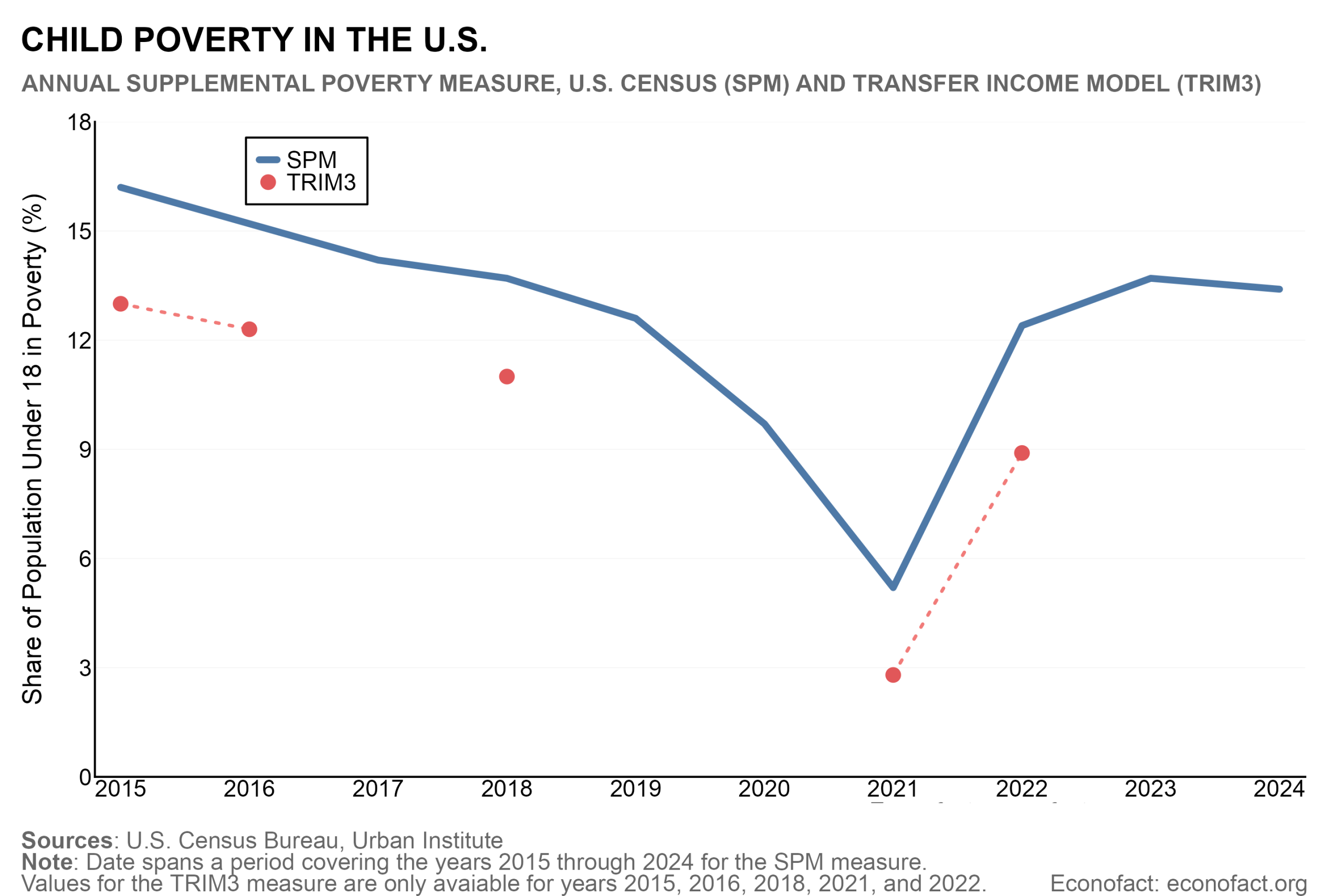

- The pandemic offered a striking example of a time in U.S. history in which changes in policy led to a dramatic drop in child poverty. During the pandemic, the federal government expanded existing social programs and implemented new measures to help support families. The wide range of measures included expanded federal tax credits, expanded unemployment insurance, stimulus checks, and expanded nutrition assistance. Compared to 2018, when the proportion of children living in poverty in the U.S. was 13.7 percent based on the U.S. Census Bureau’s supplemental poverty measure (SPM), the rate was only 5.2 percent in 2021. (Unlike the Official Poverty Measure, the SPM takes into account noncash benefits, such as food stamps and tax credits, as well as necessary expenses, such as out-of-pocket medical expenses and work-related expenses — in measuring household income. It also adjusts for differences in cost of living across states.) The consensus report from the National Academies of Sciences, Engineering and Medicine used supplemental poverty measurement estimates produced by the Urban Institute’s TRIM3 microsimulation model for its analysis. The TRIM3 estimates make adjustments for misreporting of safety net benefits (much of which is under-reporting), which produces lower poverty rates compared to Census estimates. Using TRIM3 estimates, the SPM measure of child poverty was 11 percent in 2018 but only 2.8 percent in 2021 (see chart). This reduction in child poverty did not last. By 2022, child poverty was 8.9 percent based on TRIM3 estimates, more than 3 times higher than the rate in 2021.

- Can federal tax credits be a policy strategy for addressing poverty? Whether and how federal tax credits address poverty depends on their design, who receives the tax credit and under what circumstances. They may help reduce poverty by both increasing the income received by some working households and by encouraging employment. The Earned Income Tax Credit (EITC) supplements earnings for low- to moderate-income working individuals and families and is fully refundable, which means that families can receive a cash refund even if they owe no income taxes. The credit grows with earnings, plateaus, and then gradually phases out as income continues to rise. The Child Tax Credit (CTC) was created by Congress in 1997 to ease the financial burden of having children. Initially, it was a nonrefundable per-child credit, which means that it could only reduce tax liabilities to zero and did not benefit the lowest-income families, since most have no tax liability. The CTC has changed over time to include a refundable component that low-income families can claim, phasing in for families with incomes above a certain amount and rising with families’ earnings until reaching a maximum amount per child. Prior to 2021, the most recent legislative changes to the CTC were made under the Tax Cuts and Jobs Act in 2017 (see chart below).

- In 2021, the Child Tax Credit was expanded to reach families at the lowest levels of the income distribution — including those with no earnings —and the size of benefits increased for some families. The 2021 American Rescue Plan Act (ARPA) made temporary changes to both the EITC and the CTC. The changes that affected families with children the most were changes to the CTC. (ARPA temporarily expanded the EITC’s benefits for workers without children but left family benefits unchanged). The legislation temporarily extended CTC benefits to children in families with no earnings. The maximum amount of the credit increased to $3600 for each child less than age 6, and to $3000 for each child aged 7-16. The credit was made fully refundable and the credit phase-in was eliminated. As a result, tax filing units could claim the full credit even if they had no earnings (see chart). In addition, while ordinarily tax credits are only received the year following the year when the income is earned (e.g., at tax filing time in Spring 2022 for income earned in 2021), monthly payments were allowed immediately after the ARPA legislation passed in 2021, meaning families were eligible to receive up to half of their credit on a monthly basis.

- Federal tax credits played a key role in lifting families out of poverty during the pandemic. The National Academies of Sciences, Engineering and Medicine report concluded that the tax credits in 2021 (the existing provisions combined with the ARPA expansions) relative to no credits lifted more than 2 million children out of poverty or a 51 percent reduction in child poverty that year. Estimates in the report showed that the decline in child poverty in response to the tax credits would have been 3 to 4 times higher if the other pandemic relief programs that also lifted many children out of poverty had not been in place.

- The extent to which tax credits change employment and earnings of parents and other adults in the household affects the impact these tax credits have on child poverty. Changes to tax credits can alter incentives to work. Employment (and thus earnings) may decline in response to the tax credit, partially offsetting its anti-poverty effects, if the credit reduces the pressure to earn income from work. This was the case with the extension of the CTC under ARPA to families with no formal earnings. Alternatively, the tax credit may increase employment, augmenting its anti-poverty effects, as it enhances earnings from employment making work more attractive. This was the case with the EITC and CTC prior to ARPA, since a minimum amount of earnings was required in order to receive credit. The report estimated that if effects on employment are taken into account, the impact of the tax credits in 2021 (both the existing policies and the ARPA expansions) on child poverty was even larger. However, the ARPA changes to the child tax credit were temporary, which makes it difficult to draw lessons from this experience for how permanent changes to the CTC would impact child poverty, especially over a longer time period. Also, the ARPA CTC expansion, by itself, when not combined with other policies such as the EITC, was found to increase the number of children in poverty due to reductions in employment and thus earnings as a source of income.

- Not everybody who was eligible to receive the tax credits in 2021 claimed them, but participation rates were relatively high. The use of tax policy to distribute resources to broad swaths of the U.S. population rapidly was put to the test during the pandemic. Administrative records estimate participation rates of above 80% among those eligible for both the EITC and the CTC, although take-up rates (participation among those eligible) were lower among Hispanic families and lower-income families. The expansions came as a surprise for many people with very low income who were not “attached” to the tax system and struggled to understand the expanded credits and how to claim them through tax returns or directly. Still, the majority of families with low income and children who were eligible for tax credits received them. This was in part because the Department of the Treasury did extensive outreach to encourage people to apply through an online portal and because it also sent checks directly to families who had filed in previous years for whom the Treasury had both bank information and could infer eligibility. Community-based organizations and other trust-based information and education sources helped families unfamiliar with filing taxes and claiming tax credits as well.

- The fiscal cost of achieving poverty reduction through a federal tax credit depends in part on the way in which benefits are structured across the income distribution. The 2021 expansions of the EITC and CTC increased federal outlays (the cost of the benefits received from these two credits by US households) by an estimated $228 billion. However, only 6% of these additional outlays were estimated to go to families living in poverty because these credits, especially the CTC, are structured to benefit children in families with higher income. All in all, only about 6 percent of government outlays on both the EITC and CTC in place in 2021 went to children living with incomes at or under 100% of the poverty line, while about 53 percent went to children above 200% of the poverty line (see figure 8-15).

- There are different policy options to modify the existing federal tax credits to achieve greater reductions in child poverty. Estimates from simulations of modifications to the earned income and child tax credits show that the largest potential poverty reductions occur when the credit is fully refundable, including for those with no earnings, and when eligibility for the tax credit starts at lower income levels. Other policy options, such as exempting caretakers who are elderly, disabled, or with children under 6 from any earnings requirement, also resulted in poverty reductions. The most generous expansions of the CTC achieve the largest reductions in child poverty, though at substantially higher fiscal cost. However, the fiscal costs can be mitigated somewhat with faster phase-outs of credits for high-income groups. Taking into account possible changes in employment in response to expansions to the CTC tended to lower the anti-poverty impact somewhat, but still resulted in a lower child poverty rate than under current policy. Detailed examples of alternative policy options and their impact on child poverty are included in the National Academies Report (see this chapter).

What this Means:

Child poverty imposes high costs on the children that experience material needs as well as on society. A growing body of evidence shows a causal link between the lack of resources and adverse outcomes for children, who tend to have lower rates of completed education, lower earnings in adulthood, and higher rates of mortality. Federal tax credits can play an important role in lifting people above poverty. Still, under current policy, Census estimates suggest that more than 10 percent of US children — over 8 million children — live in poverty. The experience of 2021 shows that the Child Tax Credit could be expanded to achieve greater reductions in child poverty, at some cost. Key decisions that affect the benefits of such a response include how far down the income distribution benefits are targeted, how quickly the benefits are phased in, and how far up the income distribution the benefits go, and how these design considerations affect changes in people’s employment behavior and earnings. Each of these aspects also affect costs to the government. Improving data and supporting research done by the Census Bureau to improve poverty measurement, as well as increased access to administrative data, and information about how families use the credit are important for improving understanding of responsiveness to poverty reduction policies.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.